Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

API/RSS

API/RSS

Social

Social

DeFi lending is reshuffled, what new trends can be found through protocol changes?

Summarized by AI

Summarized by AI

Original author: 1kx researcher Mikey 0x

Original compilation: 0x214, BlockBeats

In the past few months, the DeFi lending track has undergone major changes. 1kx researcher Mikey 0x has reorganized this field, and BlockBeats organizes and translates it as follows:

The content of this article will include the introduction of the new lending agreement, core data statistics and development trends, which may allow us to roughly grasp the next Cycle track appearance.

< /p>

New lending agreement

dAMM and Ribbon

dAMM ;and Ribbon is an under-collateralized, variable rate loan The protocol, similar in nature to Aave 's pool-based model, provides users with efficient, frictionless deposit and lending experience.

dAMM currently supports 23 assets, Ribbon will be launched soon.

Lulo

< a href="https://www.lulo.finance/" target="_blank">Lulo is a P2P order book model lending agreement on the chain, providing fixed interest rate and periodic lending. After running on the backend, users can easily profit from the complex lending mechanism.

Similar to Morpho , Lulo closes the lender/debit spread common in lending pool models, while is a direct match on credit/debit.

Arcadia

< /p>

Arcadia Assets (ERC-20 and NFT) are mortgaged into treasury. These treasuries are NFTs and thus can be combined as second layer products. Lenders can choose risk appetite based on vault quality.

ARCx

< /p>

ARCx The lending agreement will trade on the borrower's chain The better the historical transaction credit of the borrower (for example, no history of being liquidated), the higher the loan-to-value ratio (Loan To Value; LTV). As of now, the LTV of the borrower in the largest loan is as high as 100%.

Lenders provide liquidity based on the credit risk of the borrower.

dAMM and Ribbon in ( Undercollateralized) Institutional lending competes directly with Maple and Atlendis.

Arcadia, ARCx, and Frax are variants of existing models in this area.

< /p>

Core data analysis

Many protocols are still pursuing "product verticalization" in order to maintain their competitive advantages and value capture capabilities.

Frax: Stablecoin, AMO, AMM, Liquid Staking AAVE:

Stablecoin, under-collateralized loans, risk-weighted assets RWA

ARCx : credit score

Ribbon: treasury + loan

Some lending protocols are more focused on catering to long-tail assets From an institutional perspective, dAMM is currently the only protocol that already supports multiple long-tail assets.

Euler finance< /a> Allows lending of any asset, some of which can be used as collateral.

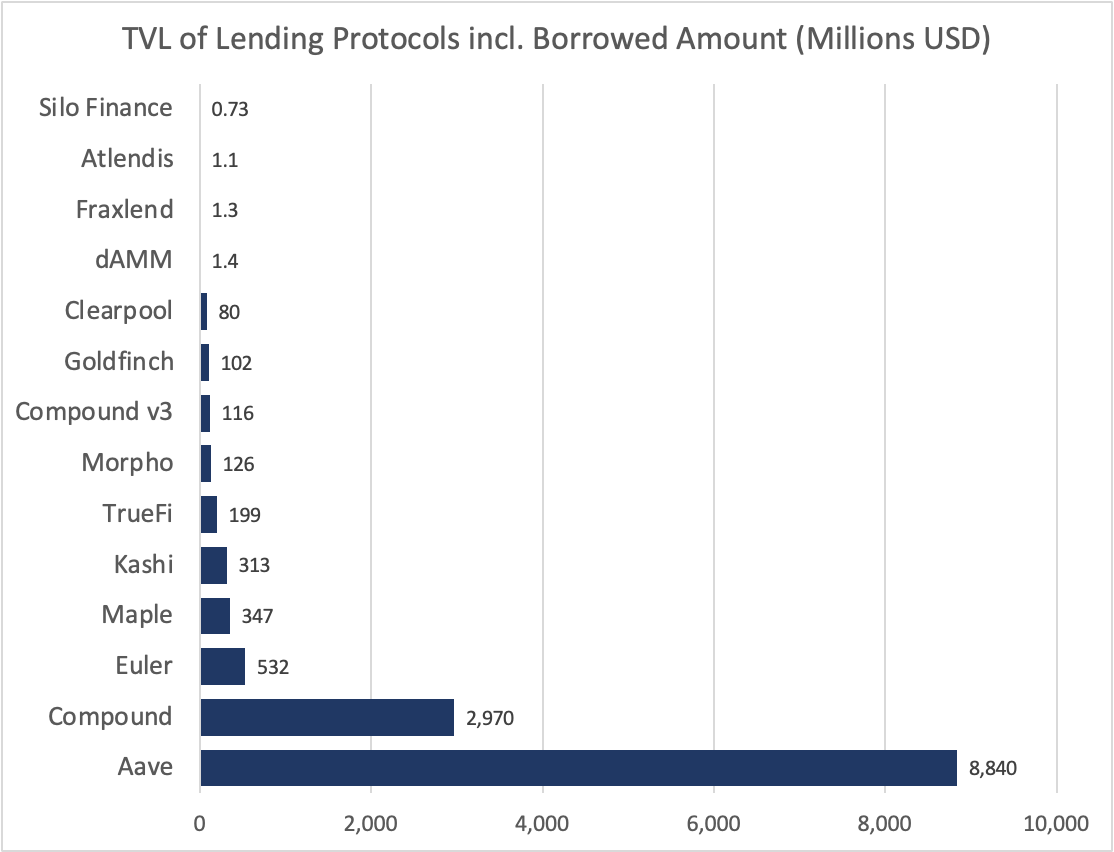

So far, AAVE still wins significantly, partly due to its active promotion of multi-chain deployment, its total TVL 37% comes from Layer 2 and EVM compatible chains.

Compound V3's slow rate of getting funds from V2 is not good, so Compound is firmly in second place.

Maple is the most popular under-collateralized lending protocol.

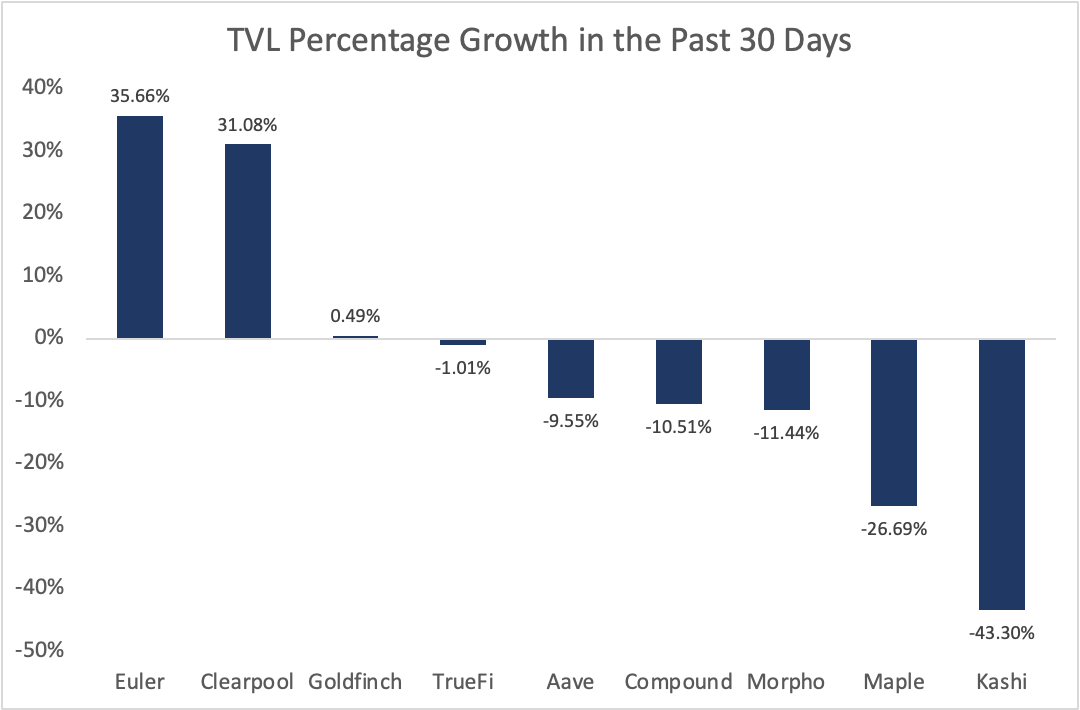

In the past month, Euler and ClearPool are the only two semi-mature platforms showing significant growth. AAVE and Compound saw mid-range growth, while Kashi saw the biggest decline.

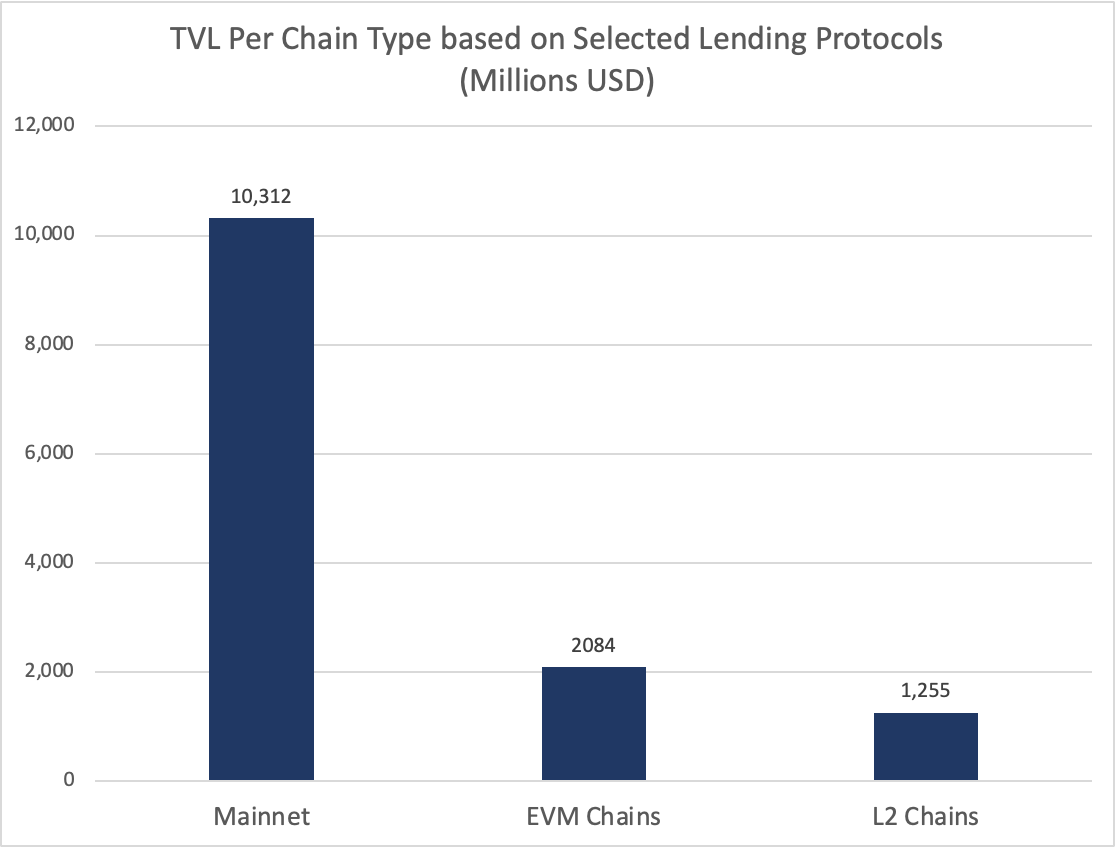

Most of the loan TVL comes from the main network, But EVM and Layer 2 are slowly encroaching on market share.

In the next cycle, the growth of Layer 2 usage and the number of projects will lead to leverage Demand increases, creating more liquidity.

TVL with different types of lending agreements Sort of, the overcollateralization model has been dominant.

However, with the advancement of KYC and ZK certificate technology, and the entry of more institutional capital, this gap is expected to further narrow.

Compared with blue-chip assets and long-tail asset lending, blue-chip assets currently occupy almost all of the liquidity. Euler is a relatively well-known protocol that focuses on long-tail assets, but less than 5% of its TVL belongs to long-tail assets, which is mainly due to the opportunity cost brought by staking Token.

When (illiquid) staking can get up to 10 to 30 times the APR, users Why did you choose to deposit GRT Token into Euler? This situation will be reversed as more liquid collateralized DeFi agreements appear in the market. In these derivatives, Token can be used for lending while earning income.

Verticalization (Verticalization) is an interesting trend in all DeFi that cannot be ignored, because lending and Not the only track with an increasingly concentrated market share...Lido, Uniswap, and MakerDAO have huge market shares in their respective categories.

< /p>

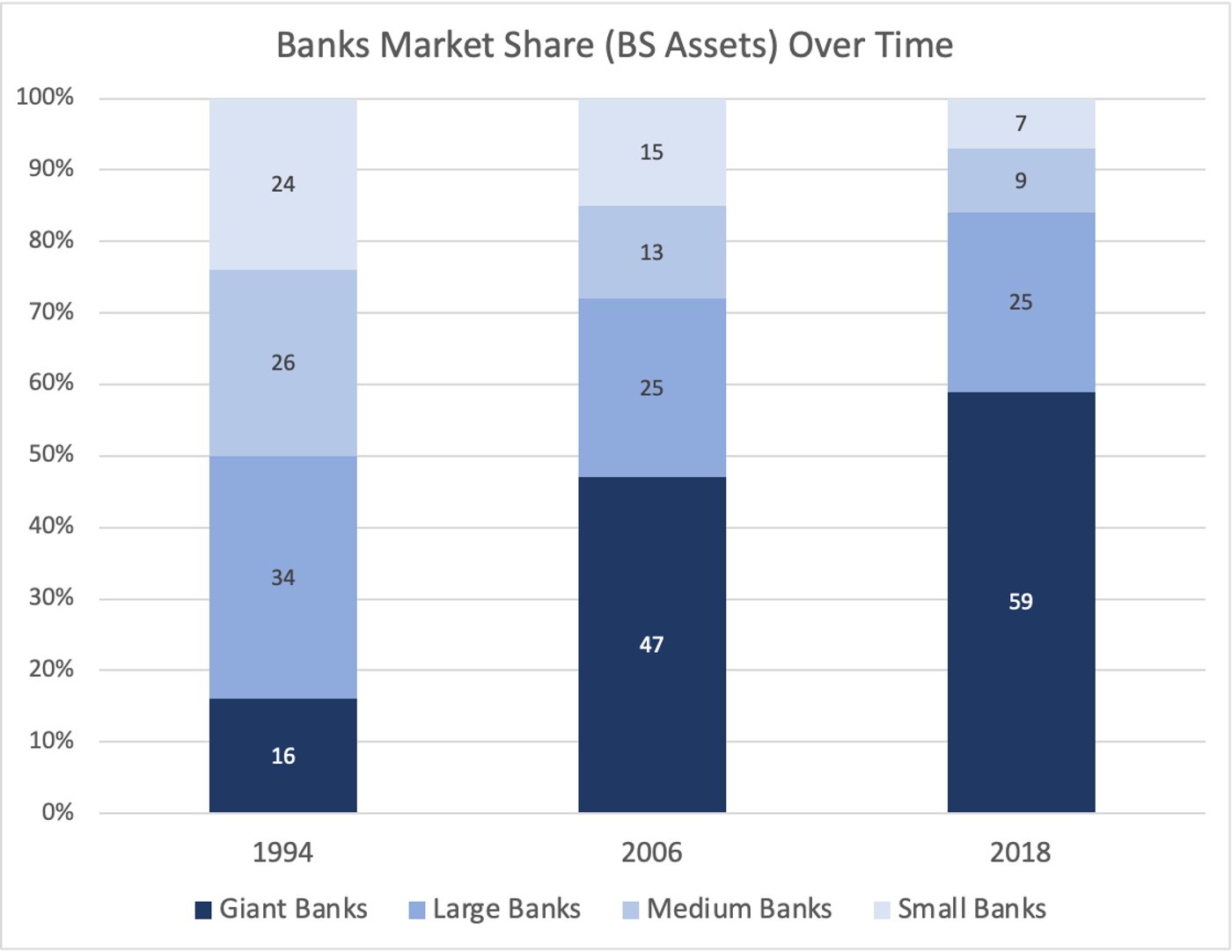

Over time, we may see the leading DeFi (and lending protocols) continue to grow stronger...similar to how large banks have continued to grow in size over the past few decades. Reasons include: strong network effects, verticalization (improving product into features), brand competitive advantage (Brand Moat).

Potential DeFi lending trend:

1) Non-full mortgage lending agreement based on off-chain assets with zk proofs (also associated with KYC access)

2) Loans with NFTs with social attributes as collateral < /p>

3) Focus on DAO loans

Original link

欢迎加入律动 BlockBeats 官方社群:

Telegram 订阅群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方账号:https://twitter.com/BlockBeatsAsia