Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

API/RSS

API/RSS

Social

Social

SBF's latest statement: Alameda tens of billions of burst losses and FTX collapse process recovery

Summarized by AI

Summarized by AI

Original title:FTX Pre-Mortem Overview"

Original article by Sam Bankman-Fried

原文编译: 麟奇,ChainCatcher

Abstract

In mid-November 2022, FTX International effectively went bankrupt. The story of FTX is, in the end, a cross between Voyager and Celsius.

The combination of these three things led to implosion.

a) Alameda's balance sheet grew to approximately $100 billion of net asset value during 2021, with $8 billion of net borrowings (leverage), and $7 billion of working capital on hand.

b) Alameda failed to adequately hedge its market risk. Over the course of 2022, a series of large market crashes, including in both stocks and cryptocurrencies, caused the value of its assets to fall by about 80%.

c) In November 2022, an extreme, rapid and targeted crash facilitated by the CEO of Binance left Alameda insolvent.

Then Alameda spread to FTX and beyond, similar to 3AC and others that eventually affected Voyager, Genesis, Celsius, BlockFi, Gemini and others.

Even so, a more objective recovery of funds is potentially possible. FTX US remains fully solvent and should be able to refund all of its customers' money. FTX International has billions of dollars in assets, and I dedicate almost all of my personal assets to clients.

Some key points

This article is a discussion about whether FTX International is solvent.

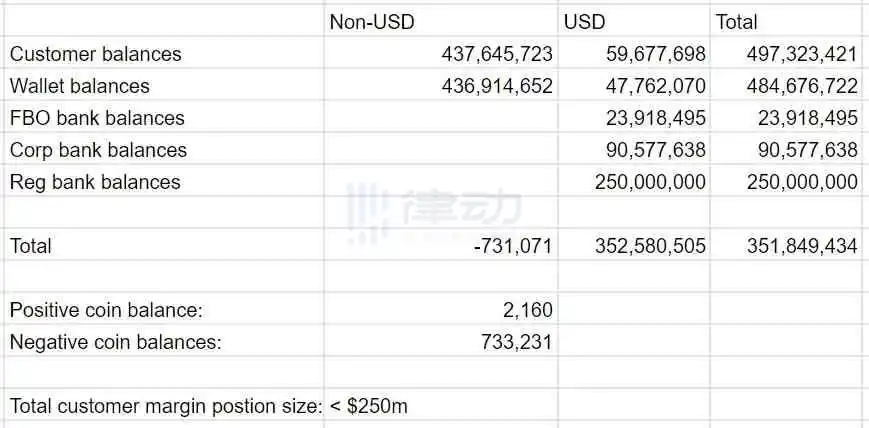

This has nothing to do with FTX US because FTX US is perfectly solvent and always has been. When I turned FTX US over to Ray and the bankruptcy panel, it had about $350 million in net cash on hand on top of customer balances. Its funds and clients are segregated from FTX International.

But it is absurd that FTX US users have yet to be compensated and have yet to get their money back.

This is the balance sheet record when I handed over FTX US:

FTX International is a non-US exchange that operates outside the US, is regulated outside the US, is incorporated outside the US and accepts non-US customers.

(In fact, its headquarters are in the Bahamas, where it is incorporated and operates as FTX Digital Markets LTD).

US clients are on the (still solvent) FTX US trading platform.

Senators to Sullivan & Crowell (S& C) about potential conflicts of interest. And S& C's statement to the contrary that their "relationship with FTX is limited and primarily transactional", S& C was one of the two principal law firms of FTX International before its bankruptcy and the principal law firm of FTX US. The CEO of FTX America is from S& C) They are associated with FTX . US in their most important regulatory applications, they work with FTX International works on some of the most important regulatory issues, and they also work with FTX. US in its most important deal. When I visit New York, I sometimes stop at S& C's office job.

S& C and GC were the principal parties that threatened me with appointing candidates of their choice as CEO of FTX, including solvent FTX US, who then filed for Chapter 11 bankruptcy proceedings and selected S& C acts as a consultant to the debtor entity.

Despite the bankruptcy, and despite handling about $5 billion in withdrawals in its final days of operation, FTX International still retained a lot of assets, about $8 billion in different liquid assets at the time of Ray's takeover.

That is in addition to a number of potential financing proposals, including letters of intent signed after the Chapter 11 filing, totaling more than $4 billion. I believe that if you give FTX International for a few weeks, it is likely to use its illiquid assets and equity to raise enough capital to make its customers largely reimbursed.

However, since S& Since C pressed FTX to file for bankruptcy protection, I fear these avenues may have been abandoned. Even now, I believe that if FTX International restarted, and customers are indeed likely to receive substantial compensation.

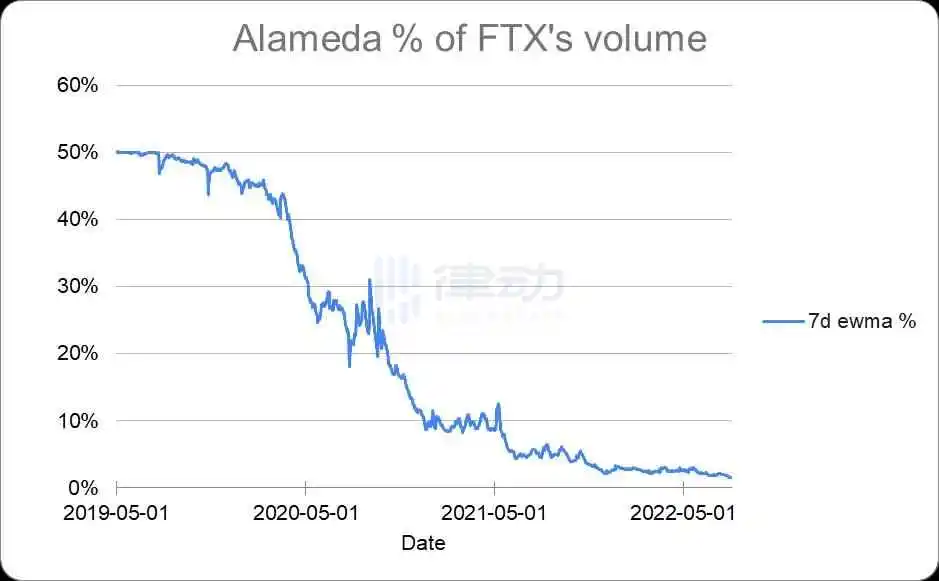

While FTX liquidity began to rely primarily on Alameda in 2019, by 2022 FTX liquidity had diversified, with Alameda declining to around 2% of FTX trading volume.

I didn't steal money, and I certainly didn't hide billions of dollars. Almost all of my assets were and are available to support FTX clients. For example, if the bankruptcy panel is willing to fulfill my D& O Legal fee protection, I offer to contribute almost all or 100% of my personal shares of Robinhood to the client.

FTX International and Alameda are both legal and independently profitable businesses in 2021, each making billions of dollars.

Alameda then lost about 80% of its asset value during 2022 due to a series of market crashes, as did 3AC and other cryptocurrency firms last year. After that, its assets fell even more in a targeted attack. FTX has been affected by Alameda's decline, just as Voyager and others were earlier affected by 3AC and others.

Note that in many places in the text, I am still forced to make approximate judgments. Many of my personal passwords are still held by the Chapter 11 bankruptcy team, not to mention the data. If they want to add data to the conversation, I would welcome it.

Also, I haven't run Alameda for the past few years.

So a lot of this stuff is an afterthought, from models and approximations, generally based on data I had before I stepped down as CEO, and models and estimates based on that data.

An overview of what Happened

2021

During 2021, Alameda's net worth soared, with a market value of about $100 billion by the end of the year, according to my model. Even if you ignore assets like SRMS, whose fully diluted assets are much larger than the amount in circulation, I think it's still about $50 billion.

Alameda's position also grew during 2021.

In particular, I think it has about $8 billion in net borrowings, which I think it spends on the following:

a) About $1 billion in interest payments to lenders

b) About $3 billion to buy out Binance's shares in FTX from FTX's existing portfolio

c) About $4 billion in venture capital

(When I say 'net borrowings,' I basically mean borrowings minus the current assets on hand that can be used to repay loans. This net borrowing in 2021 was primarily from third party lending platforms such as Genesis, Celsius, Voyager, etc., rather than margin trading from FTX).

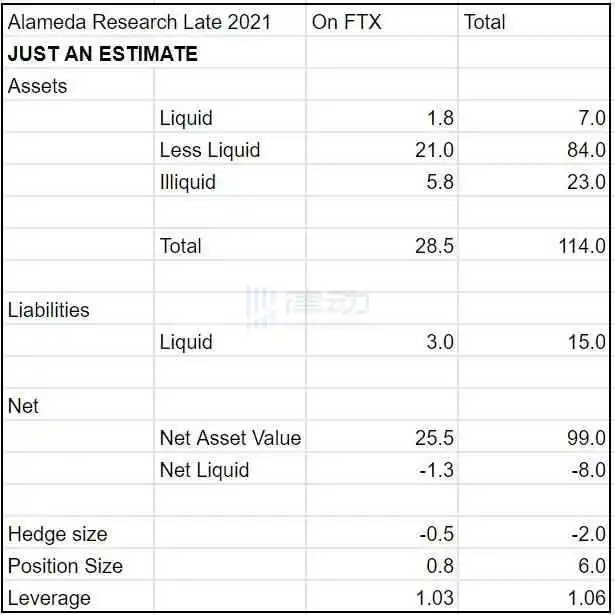

So by the beginning of 2022, I believe Alameda's balance sheet looks roughly as follows.

a) About $100 billion in net asset value

b) About $12 billion of liquidity comes from third party service desks (Genesis, etc.).

c) ~ $10 billion of liquidity

d) ~1.06 times leverage

In this context, an $8 billion illiquid position (with tens of billions of dollars of available credit/margin from third-party lenders) seems reasonable and not risky. I think Alameda's SOL alone will cover the net borrowings. Also, it came from the third-party lending desk, which, I was told, had all received an accurate balance sheet from Alameda.

I think it's good for FTX International's position was reasonable at the time, according to my model, about $1.3 billion, with tens of billions of dollars in collateral, and FTX was successfully audited by GAAP at the time.

Then, 94 percent of the market would have to crash by the end of 2021 to drag Alameda underwater! And it's not just SRMS and similar assets, if you take that out of the way, Alameda is still heavily over-mortgaged. I think its SOL position alone is bigger than its leverage.

But Alameda was not adequately hedged against the risk of an extreme market crash: only a few billion dollars of assets were hedged. Its net leverage ([net position-hedged]/ net asset value) is about 1.06 times; It was long the market.

So, in theory, Alameda faces an extreme market collapse, but it would take a similar 94% collapse to put it out of business.

The market crashes in 2022

So here's where Alameda enters 2022:

1. Net assets of $100 billion

2. Net borrowings of $8 million

3. 1.06 times leverage

4. Tens of billions of liquidity

Then, over the course of the year, the market crashed again and again. Alameda repeatedly failed to adequately hedge its position until mid-summer.

-BTC fell 30%.

-BTC down another 30%.

-BTC down another 30%.

- Rising interest rates have curbed global financial liquidity

-Luna returns to 0

-3AC is out

-Alameda's co-CEO resigns

-Voyager out

-BlockFi is almost bankrupt

-Celsius went out of business

-Genesis goes out of business

-Alameda's borrowing/loan liquidity fell from about $20 billion at end-2021 to about $2 billion at end-2022

As a result, Alameda's assets have been hit again and again. But this is not specific to Alameda's assets. Bitcoin, Ethereum, Tesla and Facebook are all down more than 60% this year; Coinbase and Robinhood are down about 85 percent from their peaks last year.

Keep in mind that Alameda has about $8 billion in net borrowings by the end of 2021:

a) About $1 billion in interest payments to lenders

b) About $3 billion to buy out Binance's shares in FTX from FTX's original investment list

c) About $4 billion in venture capital

This $8 billion of net borrowing, minus a few billion of hedges, resulted in an excess leverage/net position of about $6 billion, backed by about $100 billion of assets.

As the market collapsed, so did these assets. Alameda's assets, which include a portfolio of altcoins, crypto companies, stocks and venture capital, fell about 80 percent during the year, bit by bit increasing its leverage.

Meanwhile, liquidity has dried up in lending markets, public markets, credit, private equity, venture capital and just about everything else. Over the past year, almost every source of liquidity in the crypto space -- including almost every lending platform -- has collapsed.

That means Alameda's liquidity is down to a few hundred million dollars in the single digits by the fall of 2022, from tens of billions at the end of 2021. Most other platforms in the space have fallen or are in the process of falling, leaving FTX as the last survivor.

In the summer of 2022, Alameda finally hedged heavily on some combinations of BTC, ETH, and QQQ(Nasdaq ETF).

But even after all the market crashes of 2022, Alameda had about $10 billion in net assets shortly before November; Even if you exclude SRMS and similar tokens, the net asset value is positive and it ends up being hedged.

Margin trading

During 2022, a number of crypto platforms went bankrupt due to an explosion in margin positions, including Voyager, Celsius, BlockFi, Genesis, Gemini, and eventually FTX.

This is quite common on margin trading platforms; Among other things, it happens when:

Traditional finance:LME(London Metal Exchange),MF Global(MF Global),LTCM(Long-Term Capital Management),Lehman(Lehman Crisis)

Crypto industry:OKExAnd againOKEx(almost every week of the previous year),CoinFlex,EMX, Voyager, Celsius, BlockFi, Genesis, Gemini, etc.

The collapse that took place on Nov

After a months-long and extremely effective PR campaign against FTX and the crash, CZ's fateful tweet.

Until the FTX crash in November, QQQ moved about half as much as Alameda's portfolio and BTC/ETH moved about 80 percent, meaning that Alameda's hedging (QQQ/BTC/ETH) worked to some extent. Hedges weren't big enough before the 3AC crash, but by October 2022, unfortunately, they were finally big enough.

But the November rout was a targeted attack on Alameda's holdings, not a broad market move. In a few days in November, Alameda's assets fell by around 50%; Bitcoin is down about 15% to just 30% of Alameda's assets, while the QQQ is completely unchanged. As a result, the bigger hedges Alameda eventually made over the summer didn't work. It helped with every slump that year, but not this one.

Over the course of November 7th and 8th, things went from tense but largely under control to clearly insolvent.

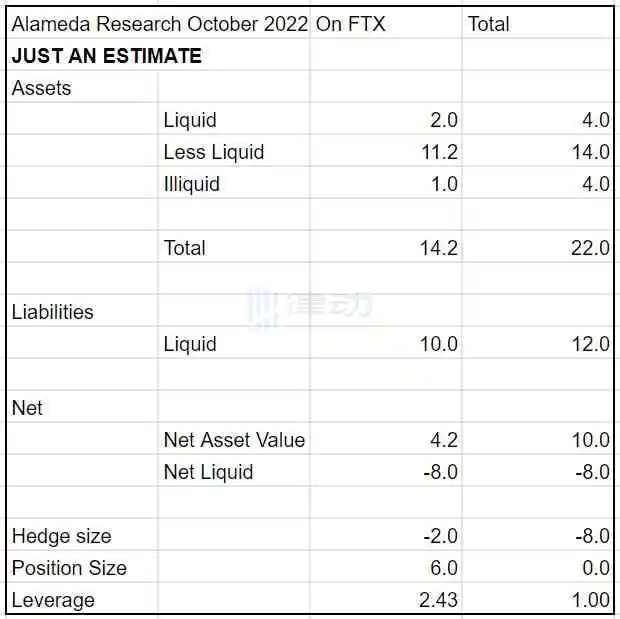

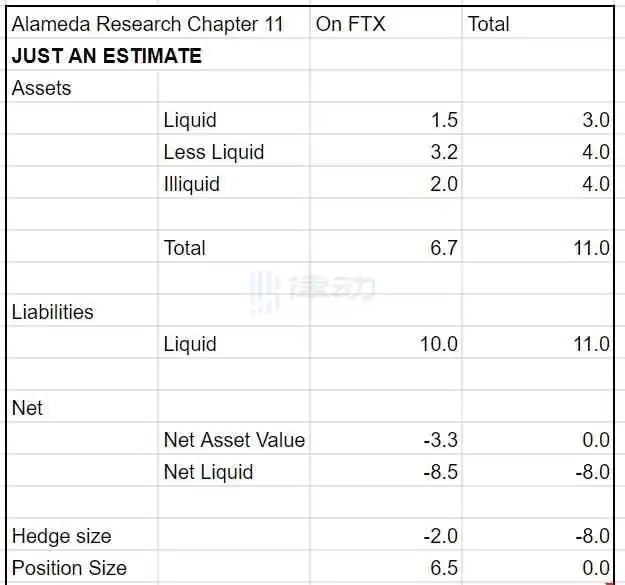

By November 10, 2022, Alameda has only about $8 billion (only semi-liquid) of assets left on its balance sheet, while current liabilities are roughly the same, about $8 billion:

A run on the banks requires immediate liquidity, and Alameda has none.

This autumn Credit Suisse fell by nearly 50% amid threats of a bank run. The threat of a run on the bank. At the end of the day, its run on the bank was unsuccessful. FTX does not.

So as Alameda became illiquid, So does International, because Alameda has a margin position on FTX; A run on the banks turned this lack of liquidity into insolvency.

This means FTX joins Voyager, Celsius, BlockFi, Genesis, Gemini and others who have suffered collateral damage due to the liquidity squeeze on borrowers.

All this is to say: No money was stolen. Alameda lost money because it did not adequately hedge the market, as 3AC and others did this year. FTX has been affected, just as Voyager and others were earlier.

epilogue

Even so, I think it is possible for FTX to make all its clients whole if it makes a concerted effort to raise working capital.

When Ray took over, the company received billions of dollars in financing offers, and has since received more than $4 billion in financing offers.

If FTX had been given a few weeks to raise the necessary liquidity, I believe it could have materially compensated its customers. I didn't realize it at the time, Sullivan & Cromwell risks undoing these efforts by putting pressure on Ray and filing for Chapter 11 bankruptcy protection, which includes solvent companies such as FTX US. I continue to believe that if FTX International were to restart today, it would be possible for customers to be materially compensated. Even if you don't, there are plenty of assets available to clients.

Many of them were data from companies I didn't run at the time (Alameda). Unfortunately, I was slow to respond to public misconceptions and material misstatements. I spent some time piecing together what I could, and I didn't have and couldn't access a lot of the relevant data, much of it from a company I didn't run at the time (Alameda).

I had been planning to give the first substantive account of what had happened when I testified before the House Financial Services Committee on December 13. Unfortunately, the Justice Department had moved to arrest me the night before, preempting my testimony with an entirely different news cycle. Either way, a draft of my deposition was leaked.

I have a lot more to say about why Alameda failed to hedge. What happened to US, what led to the Chapter 11 proceedings, S& C and so on. But at least it's a start.

Original link

欢迎加入律动 BlockBeats 官方社群:

Telegram 订阅群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方账号:https://twitter.com/BlockBeatsAsia