Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

The Block annual Report (below) : Web3, NFT trend interpretation

The Block Annual Report (PART 2) : Interpretation of Web3 and NFT Trends & NBSP;

原文来源: The Block

Glacier Web3 Lab

Chapter 5: Decentralized Finance: Overview of 2021, Prospects for 2022 & NBSP;

Decentralized finance: Overview in 2021, Outlook in 2022

Look at decentralized finance, including: lending, decentralized exchanges, derivatives, decentralized stablecoins, leverage, and more.

The profile

- Total value locked in DeFi is over $100 billion. Most of the money has been allocated to lending platforms and decentralized exchanges. However, most DeFi tokens perform worse than Ethereum.

- An eight-fold increase in the amount of stolen funds compared to the previous year was the result of 50 misappropriation incidents totalling us $610 million.

- Regulatory pressure will divide and reshape DeFi. More and more applications will enforce KYC requirements and require trust in product facilitators.

Status of DeFi in 2021

Decentralized Finance (DeFi) is an open, multifaceted financial system driven by smart contracts and blockchain predictions, an alternative to the traditional opaque system run by decades-old infrastructure and processes. It provides users with unpermised and borderless access to a variety of financial instruments without relinquishing control of assets to intermediaries such as brokerage firms or banks.

The liquidity mining boom (LM) triggered by the "DeFi Summer" in 2020 kick-started DeFi's unlimited opportunities and continues to attract liquidity in 2021. The net value of DeFi agreements soared from $16.1 billion to $101.4 billion this year, with the majority of crypto assets allocated to loan agreements and DEXs.

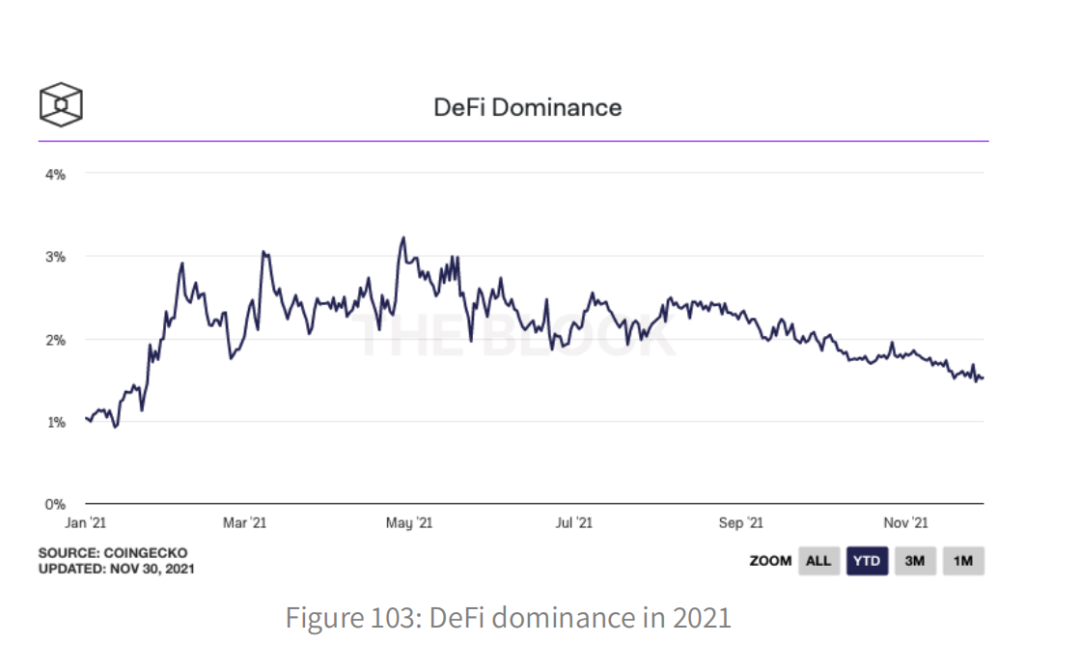

However, DeFi token dominance as an asset class has declined after a strong first quarter. The DeFi dominance index stood at 1.0 percent in January, 3.2 percent in April, and 1.5 percent now.

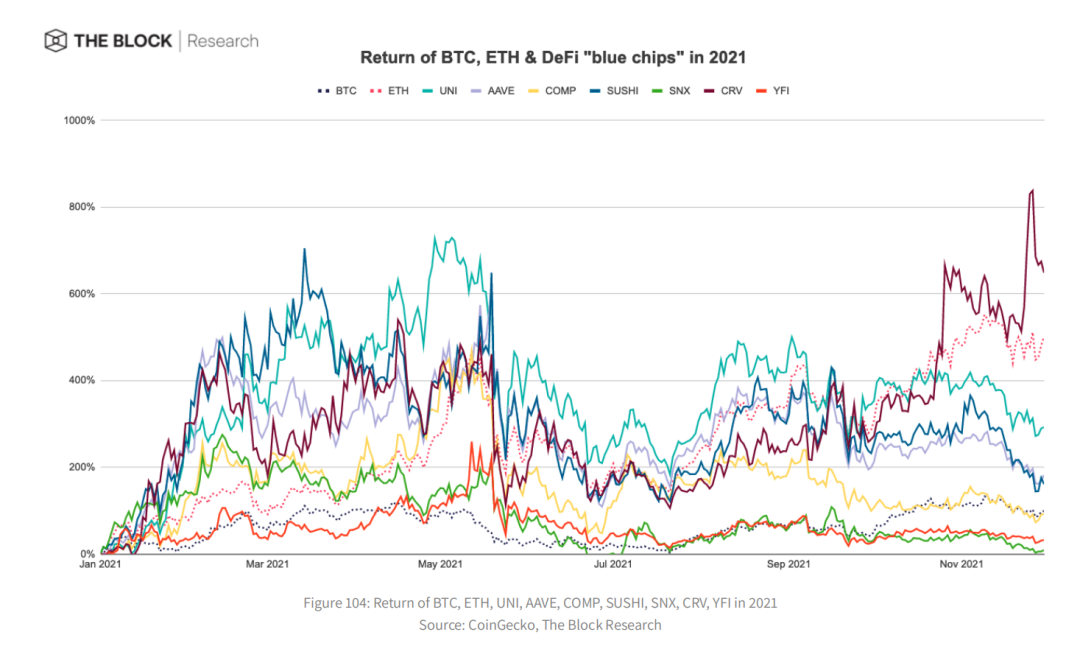

Using DeFi "blue chips" (UNI, AAVE, COMP, SUSHI, SNX, CRV and YFI) as proxies for DeFi token performance so far this year, most blue chips have outperformed BTC but underperformed ETH despite a solid start to the first quarter. CRV is the only company to outperform ETH so far this year after explosive growth in q4, while SNX, YFI and recent COMP are the worst performers. The strength of ETH may be partly due to the growth of DeFi, as DeFi activity is more active on Ethereum. Uniswap was the most used DeFi protocol in May, with over a million active users. On average, 45.7% of Uniswap's monthly active users are new.

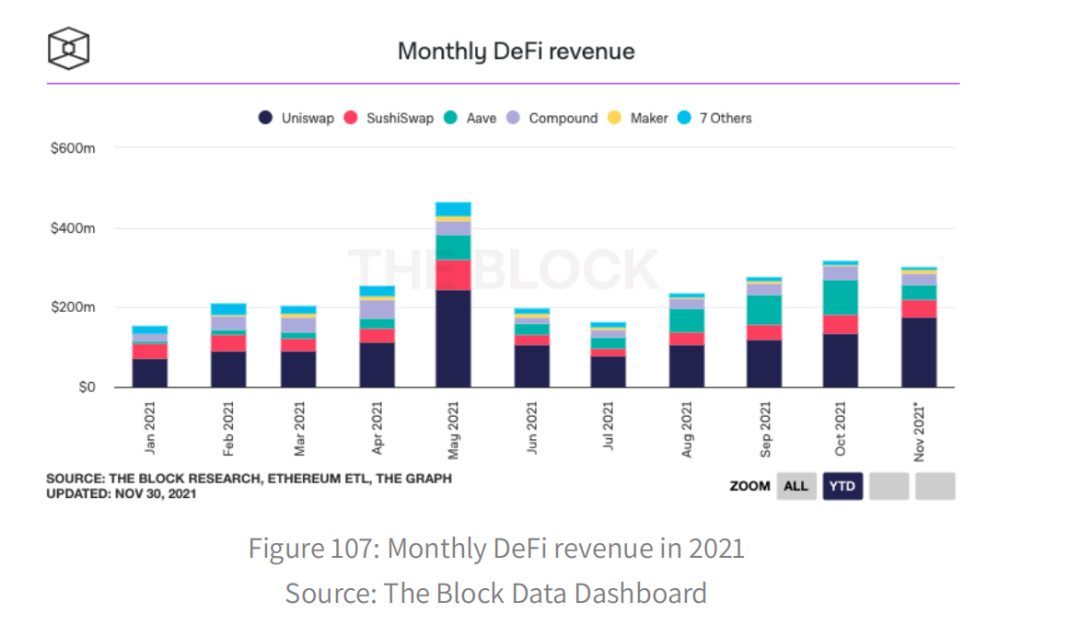

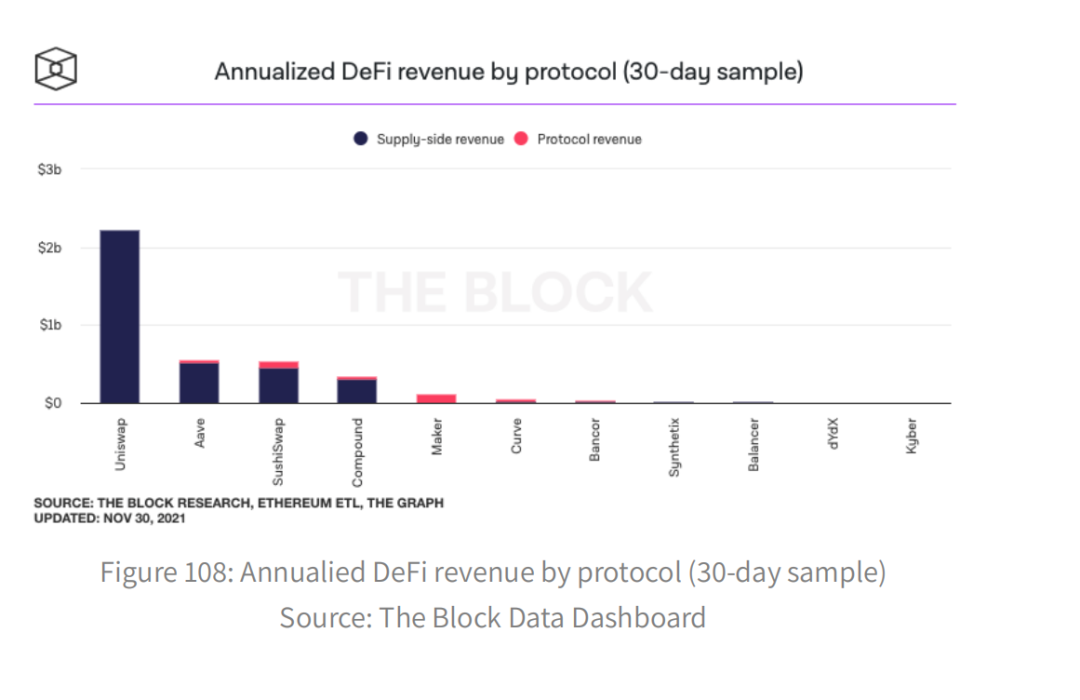

Uniswap also received the bulk of DeFi revenue from major loans, exchanges and derivatives agreements, earning $2.2 billion in 30 days. However, most recorded DeFi revenues are supply-side, that is, fees belonging to users of the agreement, such as liquidity providers and lenders. Of the major DeFi protocols, only 8.1% of revenue goes to the protocols and their governance token holders.

Lending

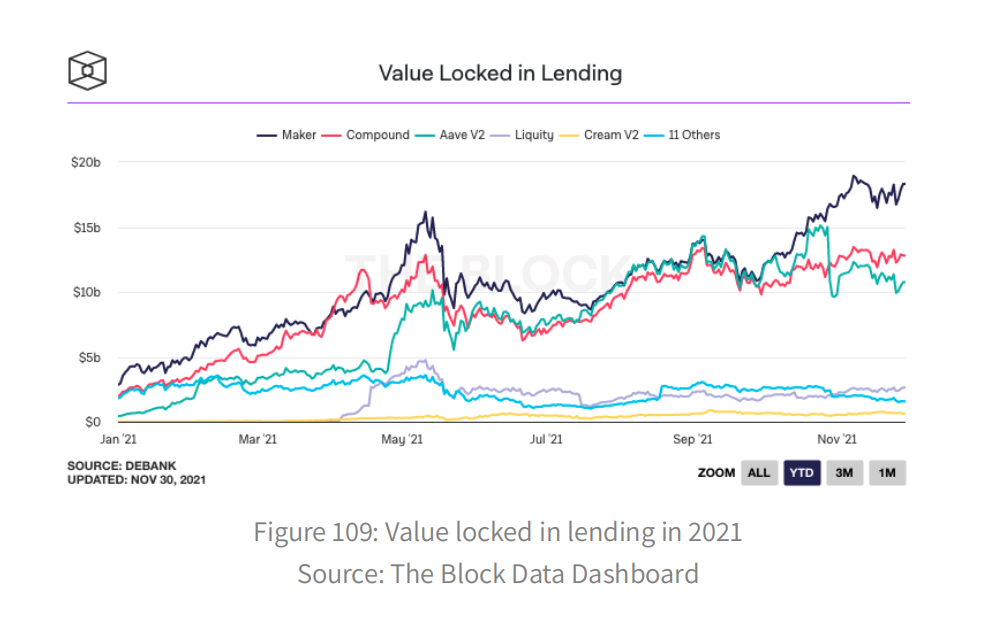

Lending is one of DeFi's main pillars, as the market has witnessed the unstoppable growth of TVL loan agreements from $7.1 billion to $46.8 billion in 2021, which represents an increase of 559.2%. The top three loan agreements by lock-in value were Maker, Compound and Aave, with TVL at $18.3 billion, $12.8 billion and $10.8 billion, respectively, and total outstanding debt at $9.1 billion, $7.7 billion and $6.5 billion, respectively.

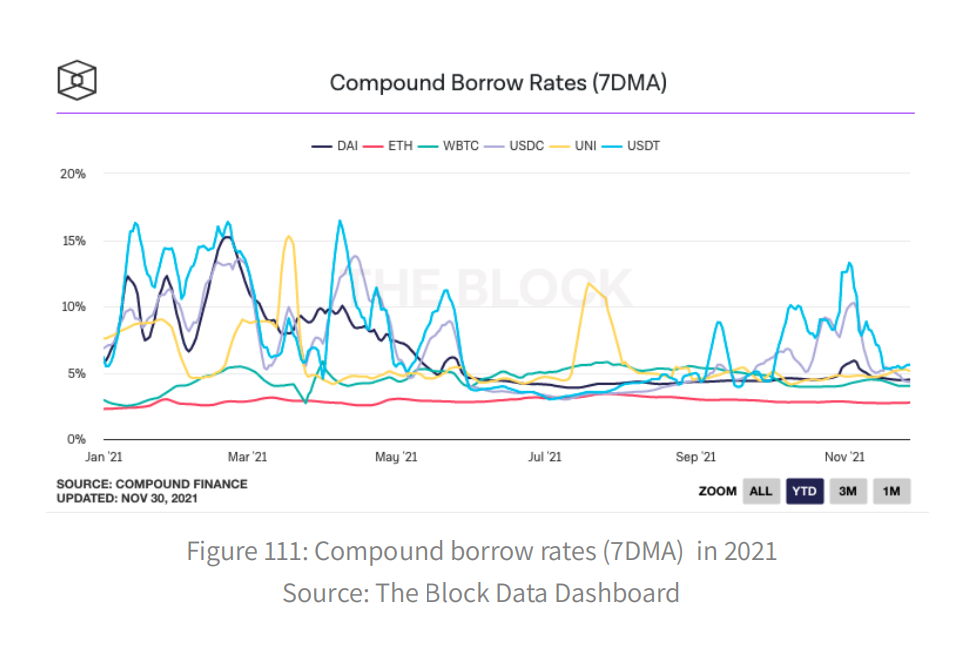

Maker drives DAI, the largest diversified stabocoin, while Compound and Aave are money markets where interest rates are adjusted by algorithms determined by loan pool utilization. Compound's borrowing rates were more volatile and relatively high during the bull market earlier this year, but they stabilized after May. Stabocoins have consistently had higher interest rates than major cryptocurrencies, reinforcing the belief that the market has a long-standing bias.

A common feature of these widely adopted loan agreements is that all loans issued must be over-secured. If the position is deemed risky, the collateral can be forced by the shareholder to cover the outstanding debt, usually when the position falls below a certain minimum collateral ratio. In this way, loans can be made anonymously and untrusted, while reducing the risk that the agreement will collapse if the defaulting borrower defaults. Despite the dominance of long-standing lending agreements, the market is becoming more diversified as new lending platforms are fine-tuned and targeted at different niche audiences. Cream attempted to include long tail assets in its money market, but presented significant risks to the integrity of the agreement, as described in the DeFi Exploits appendix. Kashi of SushiSwap and Fuse of Rari introduced separate loan portfolios to insulate these risks at the expense of capital inefficiency.

On the other hand, Alchemix and Abracadabra use the earnings generated as collateral, which mitigate some of the inefficiency of capital while also introducing composability risks. In addition, TrueFi is the first on-chain unsecured lending platform that maximizes the capital efficiency of credit borrowers. Interestingly, despite many attempts, regular fixed rate loans remain unattractive to high performance DeFi users due to liquidity fragmentation. While LM helped boost liquidity temporarily, it distorted bond prices when organic demand was absent.

Decentralized transactions

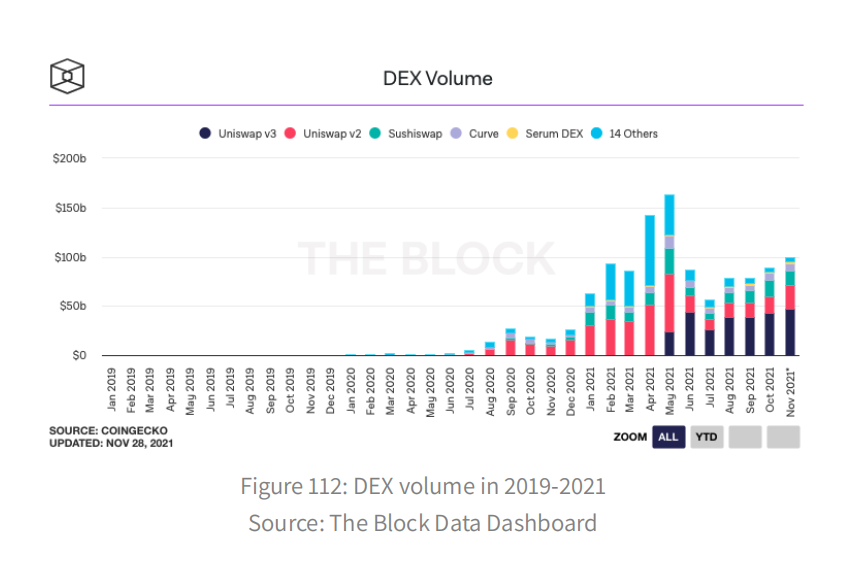

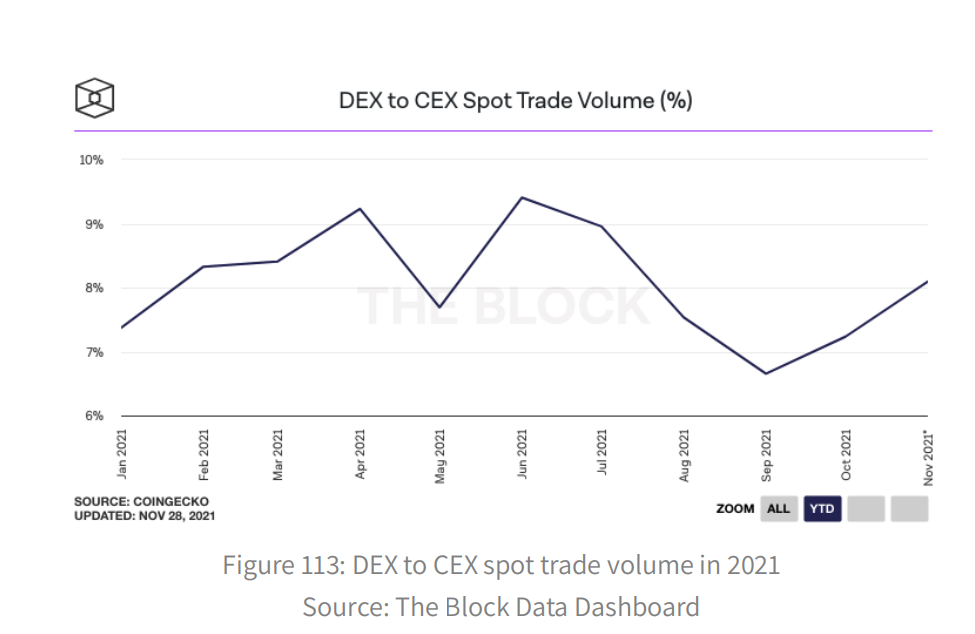

In addition to loan agreements, automated market makers (AMMs) can channel passive liquidity from market participants eager to deploy idle assets into yield. Overall, monthly DEX transactions peaked at $162.8bn in May 2021, with the biggest month-on-month increase of 137.3% in January. Volumes, however, have not fully recovered from the slump in May, with dex's spot volume ratio to centralised exchanges remaining below 10 per cent for the year.

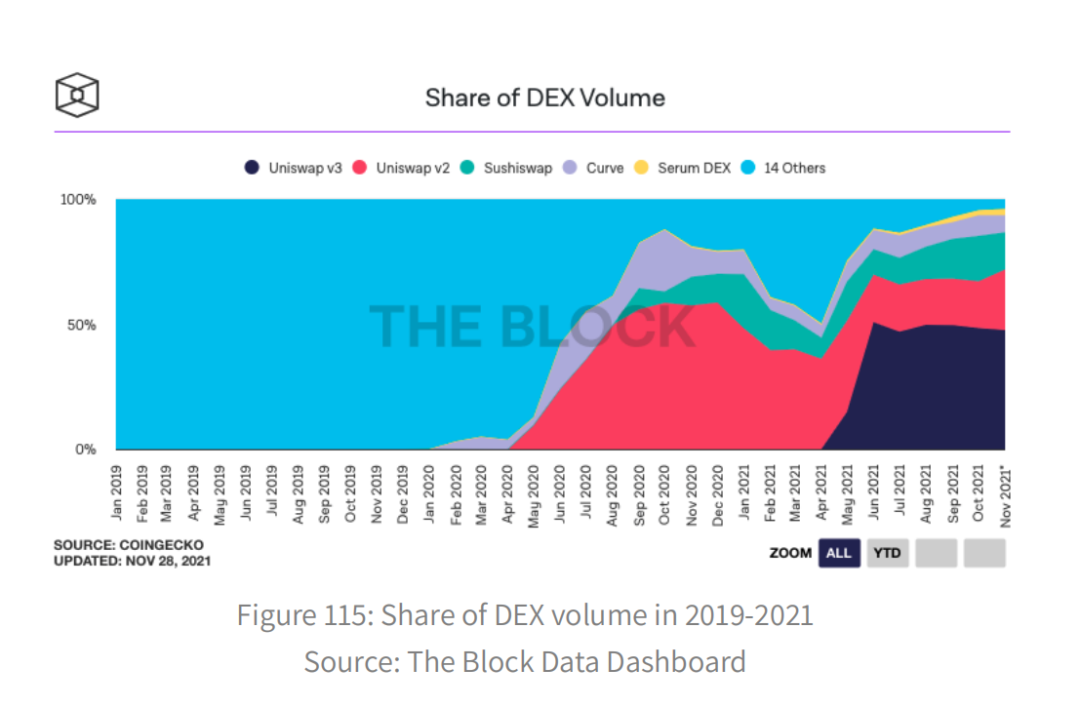

Curve is the largest DEX with a market capitalization of $16.8 billion, accounting for 6.8% of DEX's trading volume. Curve is an AMM optimized for transactions between similar assets, because liquidity is algorithmically concentrated around the peg system. Due to its continued competitive LM and lack of non-permanent losses, it generates low risk and sustainable returns.

Uniswap, on the other hand, continued to lead in terms of numbers, with Uniswap V2 being the largest DEX until it was replaced by Uniswap V3 in June. At its peak, Uniswap V2 saw $59.2 billion in monthly transactions in May, but it was dwarfed by the later versions due to V3's centralized liquidity design, which greatly reduced liquidity slippage. Uniswap V3 was released in May and is under the GNU license to prevent potential imitators, as mentioned in the Market Conditions section. SushiSwap has failed to keep up with the growth of its competitors, with TLV sales of $5 billion and a market share of 15.0%. While most of the orders were placed through AMMs, the largest DEX order by volume was Solana's serum, which accounted for 2.6%.

As liquidity becomes fragmented, users may prefer to trade through DEX aggregators, which provide better execution by optimizing switching paths. Surprisingly, on average, only 13.9% of DEX volume comes from aggregator sites. A lot of data comes from DEX local routers or trading bots. 1Inch was the annual leader in DEX aggregation with 64.9% market share, followed by 0X API(matcha) with 16.8%.

Derivatives & have spent

The largest cryptocurrency market by volume comes from permanent futures contracts, which do not mature or settle but trade close to benchmark reference index prices through a financing mechanism. Although exchanges have become more competitive over the past few years, it makes sense that the natural next step would be to extend that success to the derivatives market.

Perpetual Protocol led derivatives trading in the first half of 2021, trading a record $551.1m a week in the week of the May crash. Perpetual operates on xDai side chains and is built on a virtual AMM (vAMM) that parameterizes market depth and slip. With this model, agreements can provide liquidity immediately without the need for counterparties. Another intuitive way is the development of its insurance fund, which charges 50% of the transaction fee. The fund stands ready to back the deal by covering undersecured positions in volatile markets and financing payments when VAMM acts as a counterparty to every deal. Perpetual's insurance Fund currently has $8.2 million in funds.

DYdX has made a comeback since starting its LM program in August with dYdX(the local token for the protocol). DYdX relies on StarkEx, a ZK-rollup layer 2 scaling solution, as described in the Layer 2 section. It utilizes a hybrid infrastructure model, leveraging unmanaged, on-chain settlement, and off-chain low-latency matching engines with order books.

DYdX's liquidity comes primarily from algorithmic market makers operating in the DeFi space (e.g., GSR and Wintermute). Its weekly turnover peaked in September at $9.5 billion, dwarfing Perpetual's achievements. Permanent futures typically operate in isolation from other DeFi protocols, sacrificing composability to improve capital efficiency through leverage.

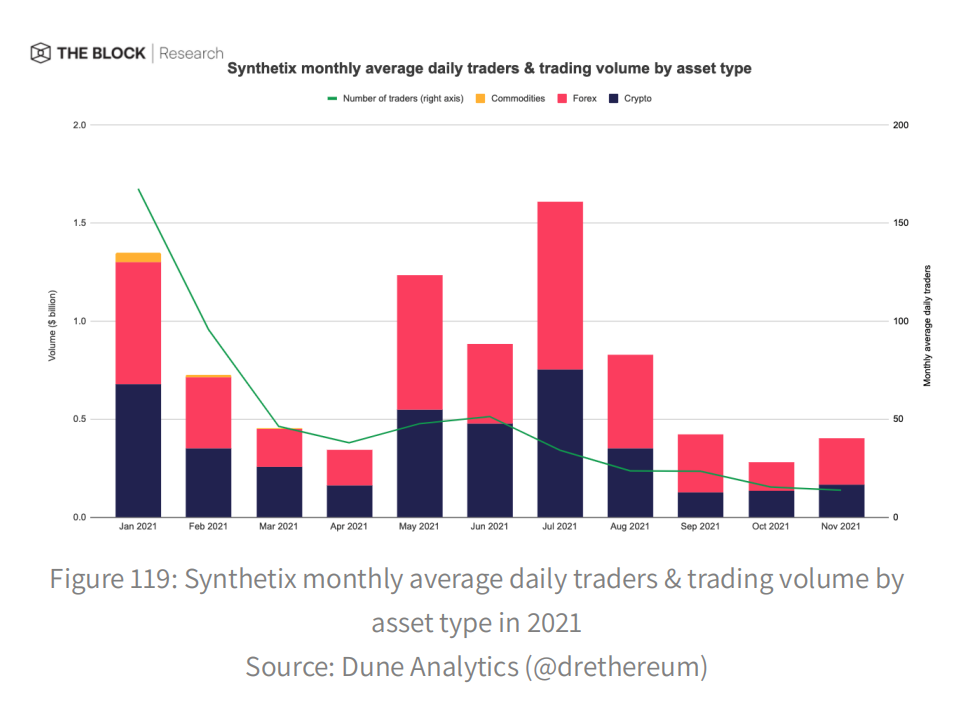

Synthetic assets, also known as synthetic, are tokenized derivatives that provide countertrading through tokenization and excessive collateral. Synthetix is the oldest and largest Synth publishing agreement to date. SNX shareholders can issue by overmortgaging and trade with other tokens on the Synthetix platform, which offers slide-free execution at Oracle prices. However, as described in the loan section, skew the open interest rate (typically favoring the long) may increase the agreed debt as SNX shareholders collectively and passively underwrite all positions.

Trading volume on Synthetix, which mainly comes from a combination of foreign exchange (52.2%) and cryptocurrencies (47.1%), peaked in July at $1.6 billion. Since then, its trading volumes have shrunk, making it a pitfall compared with the fragmented spot and permanent futures exchanges. Syntix's average daily number of traders fell to 13.8 in November from 167.5 in January, suggesting the company has failed to attract retail interest. Whether the index can regain momentum after its recent turn to optimism remains to be seen.

On the other hand, a Terra-based mirror protocol that focuses on synthetic shares mimics Synthetix's over-collateralized approach, but removes the no-slide trading offer so that synthetic shares can only trade on the secondary market. This shifts the burden of skewing open interest to the open market, resulting in mirror issue synths trading at a premium. TVL has held steady on both platforms over the past few months, with Synthetix valued at $1.7 billion and Mirror catching up. Their growth may be hampered by increasing regulatory pressure as Uniswap LABS removed their synthetic token from Uniswap's official front desk and the SEC recently filed an enforcement action against Mirror.

Not all types of derivatives will flourish in 2021. Because of the lack of liquidity and the complexity of the mechanism, the diversified options market has not yet matured into an effective speculation or hedging tool.

Structured product

In recent times, DeFi's growth has been accompanied by an increase in the complexity of portfolio management. It has spawned countless prepackaged structured products that abstract away the complexity of different financial instruments to save investors time and cost. The first iteration of structured products is the return optimizer, which captures and optimizes returns for fund savers. Convex is the biggest yield optimizer in TVL. Launched in May 2021, it specifically rewards shareholders and liquidity providers on TVL's largest DEX Curve, as described in the Decentralized Exchange section. With $16 billion for TVL, which is the first revenue aggregator with an uncertain deal, Convex has surpassed desire, with TVL's $5.9 billion in revenue.

Other types of structured products have also started to develop this year. For example, return grading agreements such as BarnBridge rank returns for investors with different risk appetite, while indices such as DeFi Pulse Index give holders passive exposure to a basket of managed tokens. On the other hand, automated liquidity offering (LP) managers like Charm and Gelato automatically rebalance LP positions on Uniswap V3, while automated trading strategy managers like Ribbon combine various derivatives with higher risk-adjusted returns. These products are still in their infancy, and it remains to be seen whether they will achieve widespread adoption.

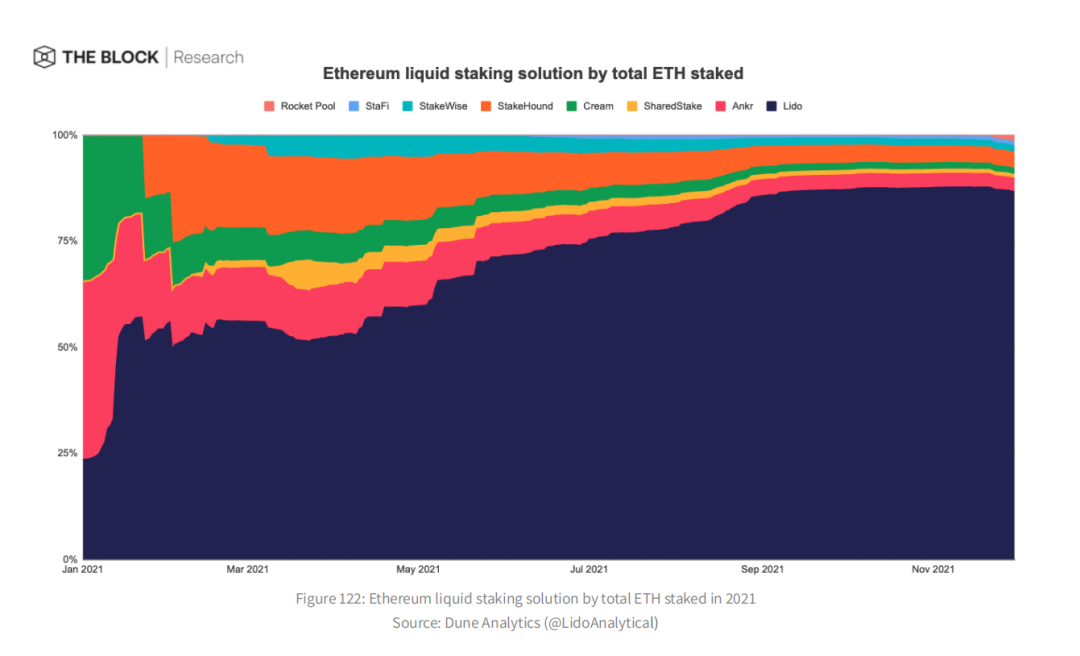

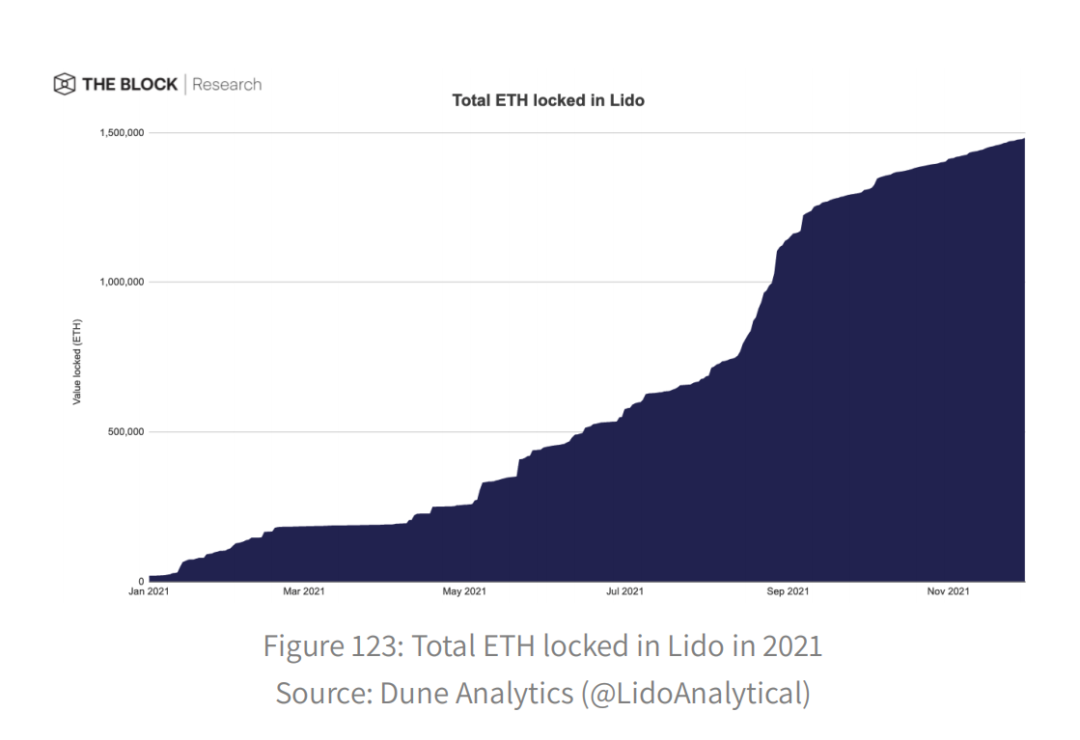

The launch of the Beacon Chain in December 2020 initiated ethereum's gradual transition to a proof-of-stake (PoS) consensus mechanism under Ethereum 2.0, as described in the layer by layer section. Users can use Ether as a validator of the network and receive more Ether as a reward. However, being a verifier requires sufficient technical knowledge and upfront funding. Liquid Bet Solutions democratize, totoken and "liquid" bet on Ethereum so that retail participants can get PoS bet exposure and leverage their equity in other DeFi applications such as collateral on lending platforms. Lido became the largest ethereum 2.0 mobile platform in one year, with a market share of 86.6% and TVL of 1.5 million ETH($6.6 billion), equivalent to 1.3% of the current Ethereum supply. TVL in ETH will continue to rise as it cannot be withdrawn ahead of the planned merger of the Ethereum main network with the beacon chain sometime in the first half of 2022.

Similar services can also be used on other PoS blockchains. Lido, for example, is streaming live on Terra and Solana with TVL of 68.1 million LUNA($3.5 billion) and 1 million SOL($208.1 million), respectively.

Decentralized stablecoin

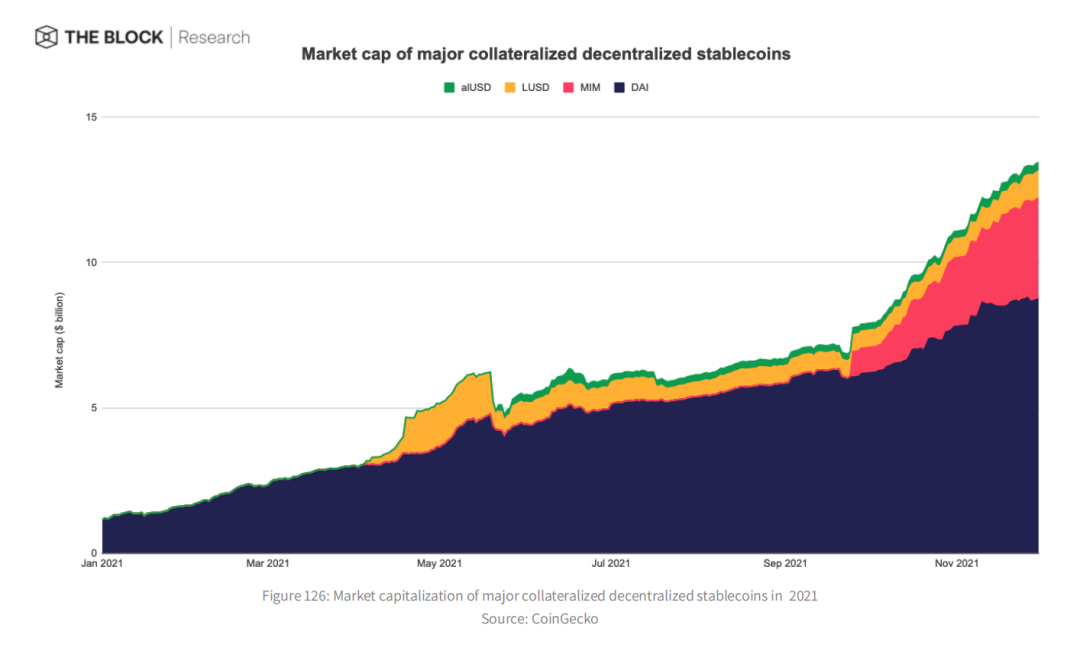

Decentralized staboins promote unlicensed payments and leverage. Maker's DAI is the largest decentralized staboin, with its share of the total staboin supply rising from 4.1% to 6.3% in 2021. The balance of DAI increased from 1.2 billion won last year to 9 billion won this year. Thanks to the introduction of the DOLLAR-pegging stabilization module (PSM), DAI's price has stabilized near the dollar peg as it traded at a premium on and off in 2020. PSM allows users to exchange a given collateral directly for DAI at a fixed rate, rather than borrowing money. 14.9% of DAI in circulation are supported by USdcs or USDP derived from PSM.

Like other DeFi industries, the prospects for decentralized stablecoins are becoming more diverse. There are currently four decentralized stablecoins with market capitalizations of more than $300 million. Abracadabra's MIM, a stabocoin backed largely by income-generating positions, is by far the second largest diversified collateral stabocoin, with a market cap of $3.5 billion. MIM borrowers earn income on their mortgage assets, which improves capital efficiency.

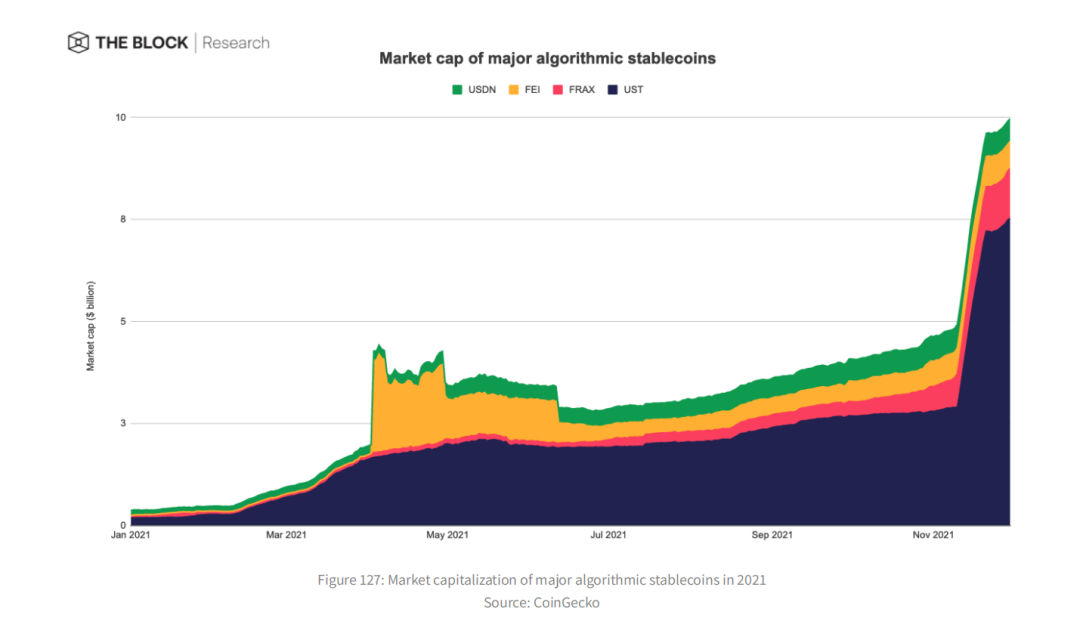

It has been known for years that the stablecoin trilemma is notoriously difficult to solve. Trilemma refers to the dilemma of stable currency when it has three attributes: decentralization, capital efficiency and price stability. In order to solve the above trilemma, we conducted a large number of experiments on algorithmic stablecoins with mixed success.

In early 2021, we saw the collapse of unsecured algorithm-based stabocoins such as the Empty Set Dollar, due to their lack of risk-free arbitrage opportunities at lower-than-expected pegged exchange rates. However, other algorithmic stablecoins that rely on fractional reserves or endogenous collateral have begun to flourish, with four of them valued at more than $300m.

Terra-based UST is the largest algorithmic staboin with a market cap of $7.6 billion and is backed as an issue-tax share by organic collateral LUNA, of which LUNA is a native asset on Terra's blockchain. $1 worth of issue-tax stock can be burned to produce 1 UST and vice versa. UST has benefited greatly from the explosive growth of the Terra DeFi ecosystem, as UST is heavily used for anchor protocols (a lending platform) and mirror protocols (a synthetic asset issuance platform).

According to the algorithm design, the algorithm stabilization coin may temporarily lose its pin. When the price of LUNA, the issuance tax token, collapsed in May, hkUST's shares traded 3.8 per cent below the dollar peg. A few days later, the dollar peg was restored.

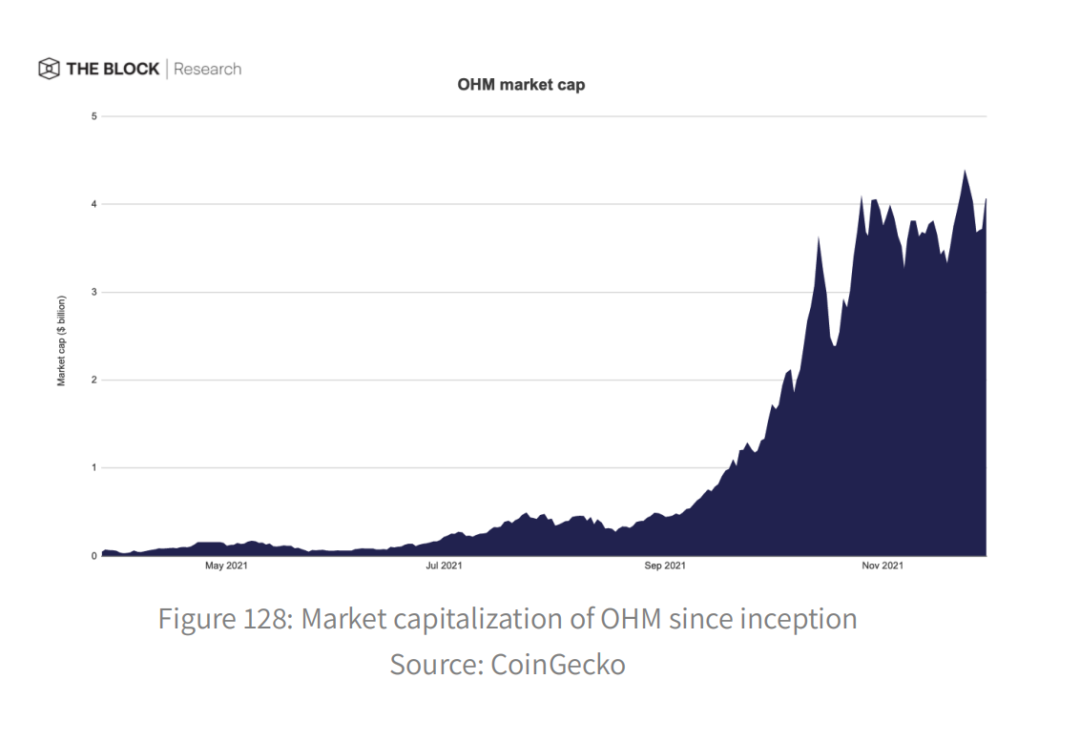

Volatility token

Often referred to as "volatile staboins," algorithmic low-volatility tokens are an emerging asset class that has gained market attention this year. They aim to become decentralized reserve currencies that are less volatile than most crypto assets and less vulnerable to long-term changes in the purchasing power of the dollar caused by unforeseen monetary policy or economic conditions.

These tokens have feedback mechanisms that dampen demand fluctuations by regulating the supply of tokens. Olympus DAO's OHM, launched in March 2021, is the largest low-volatility token with a market cap of $4.1 billion.

OHM tokens are backed by collateral but trade at a premium. This is because artificial demand is created to encourage speculators to buy into Ohm in order to earn more ohm tokens. The DAO gets more collateral by selling ohm at a below-market price, allowing the agreement to issue more Ohm tokens backed by additional collateral. This creates a circular economy driven by speculative demand. Whether these tokens can generate demand beyond pure speculation remains to be seen.

Bitcoin is challenging

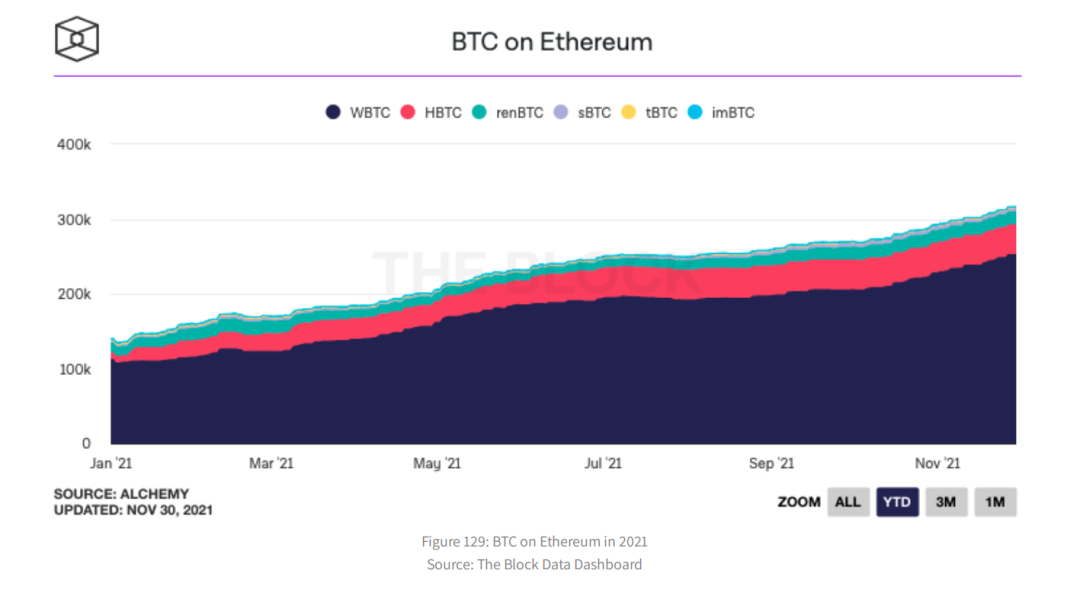

In a way, Bitcoin is the first DeFi app that allows holders to store and transfer financial value. Despite the lack of a quasi-Turing-complete virtual machine on the Bitcoin network, BTC is heavily utilized in DeFi applications on other blockchains. That's not surprising given bitcoin's 39.1% dominance of the cryptocurrency market.

The number of bitcoins wrapped in Ethereum has risen steadily, from 140,000 to 3.166 million this year, or 1.7 percent of the entire bitcoin supply. Centralized custodians play a key role in porting bitcoin's value to DeFi, probably due to capital efficiency and user friendliness. Wrapped Bitcoin (WBTC) is the most popular version of Wrapped Bitcoin with 80.0% market share on Ethereum, followed by Huobi BTC (HBTC) with 12.6%, Surpass renBTC in January 2021. The top three WBTC holders are all loan agreements: Maker(20.8%), Compound(13.1%) and Aave(10.1%).

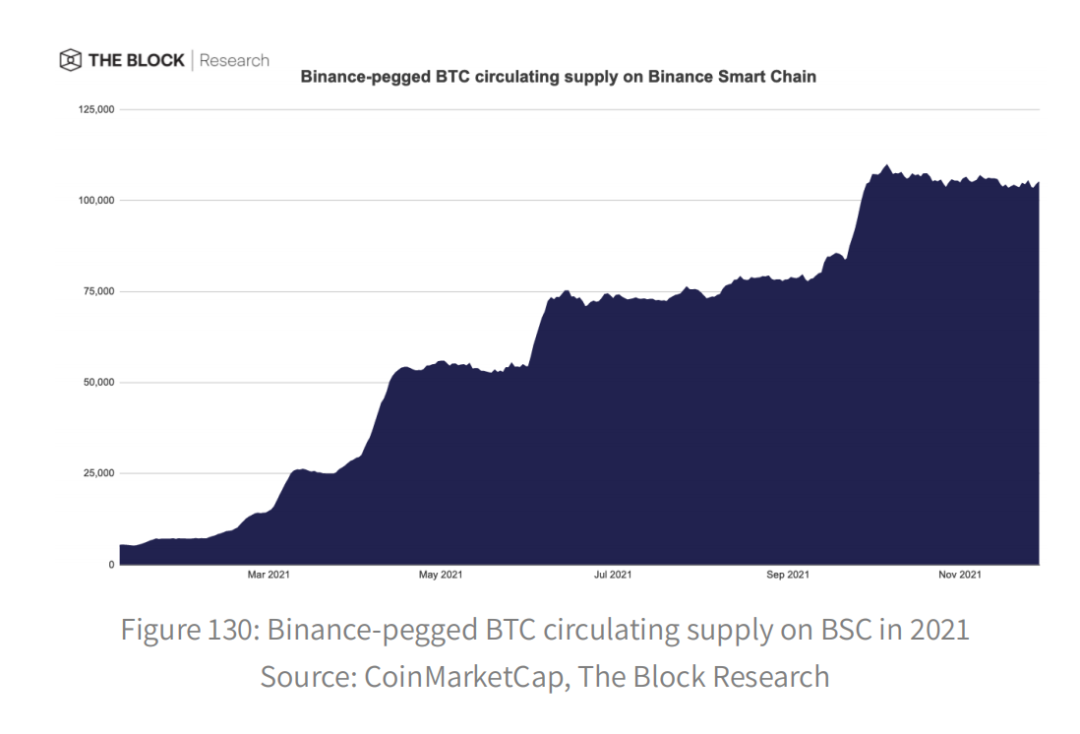

On THE BSC, the circulation supply of currency-linked BTC (BTCB) soared from 53,000 to 105,000 over the same period, suggesting healthy growth in the BSC DeFi ecosystem. The top two holders are Tranchess with 19.8%, a structured product focused on BTC; Venus, at 11.0%, is TVL's largest loan agreement on the balanced scorecard.

Value of service provider

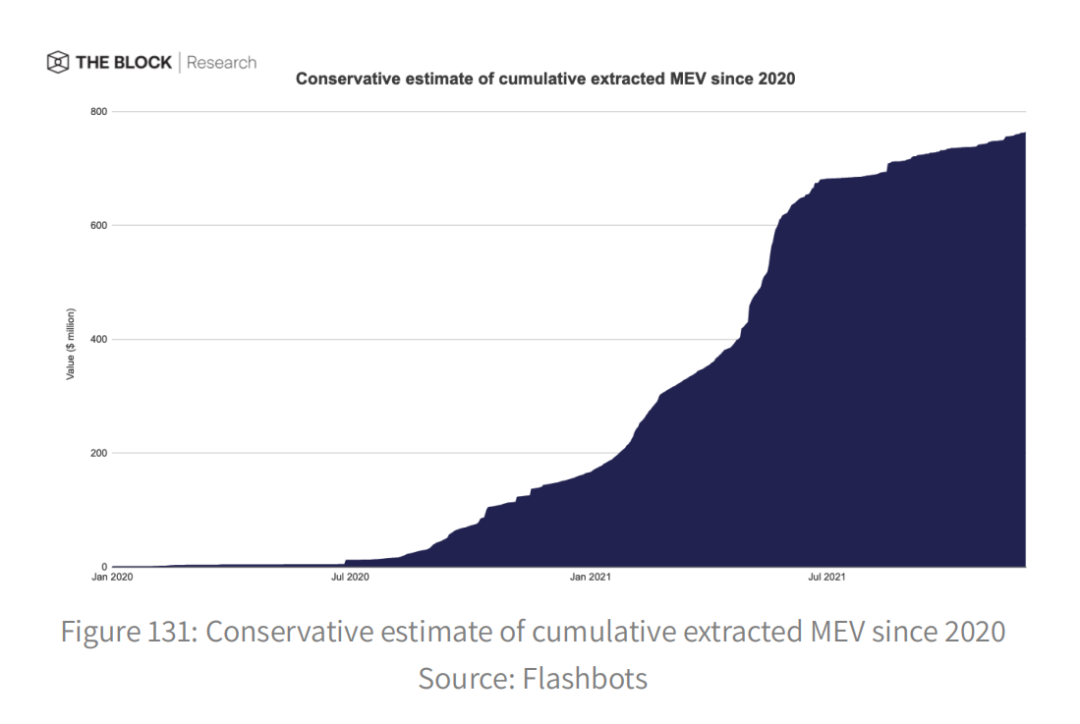

Servicers' extractable Value (MEV) refers to profits made by exploiting or sometimes abusing the ability of servicers or verifiers to (re) order or review transactions on the blockchain. It is conservatively estimated that cumulative MEV withdrawals over the two-year period exceeded $762.8 million, of which 78.4 per cent was extracted in 2021.

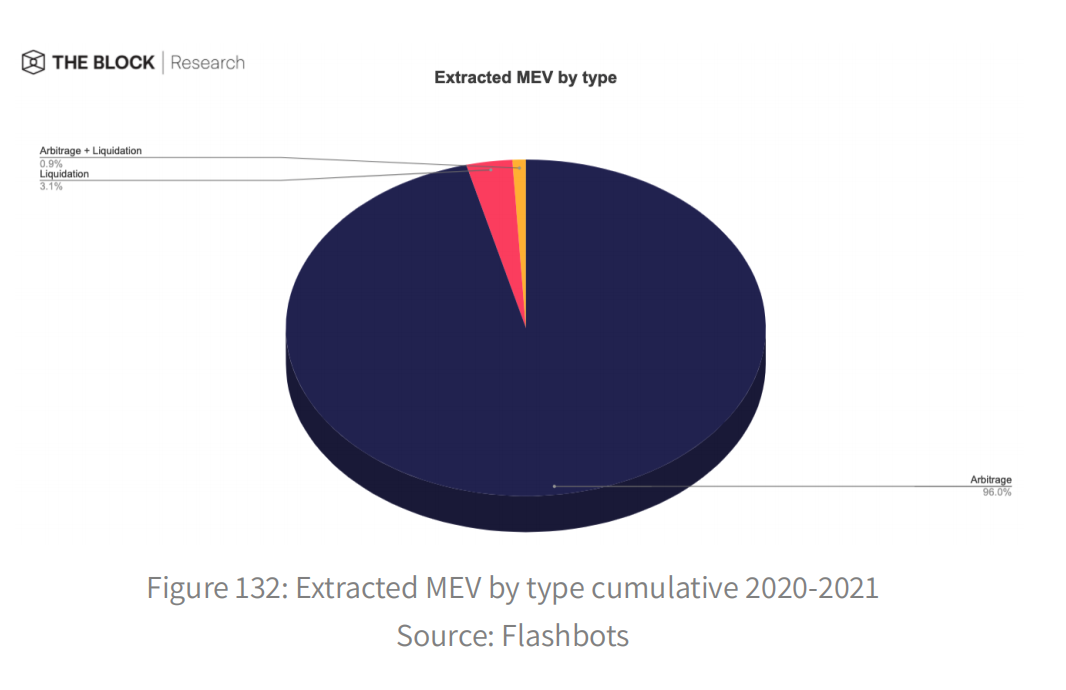

96% of the MEV extracted is related to arbitrage, as arbitrage opportunities abound in the liquidity pools of exchanges. The rest are liquidation related, or both, as such opportunities mainly occur during periods of sharp price falls or short selling squeezes. On average, 88 per cent of profits go to arbitrageurs who initiate trades, while servicers pocket the rest through gas fees and "tips" from the senders.

Tools such as Eden Network, Flashbots, and KeperDAO protect transaction senders from predatory MEV bots, which retrieve meVs by running ahead or behind. Transactions submitted through these tools are forwarded to collaborative and economically related servicers, but not broadcast to the public MEM pool.

Smart wallet

There are two completely different types of accounts on Ethereum: externally owned accounts controlled by private keys and contracts specified by code. The contract allows the creation of "smart wallets" that offer greater flexibility. One notable use case is the Multisig wallet, which has been used to secure the original DeFi protocol that has not been fully decentralized. It reduces single points of failure because multiple signatures are required to sign transactions. Gnosis Safe, launched in 2017, has become the de facto standard for Multisig wallets. Usage grew exponentially, with 378,000 Gnosis safes created and 323,900 transactions from those safes.

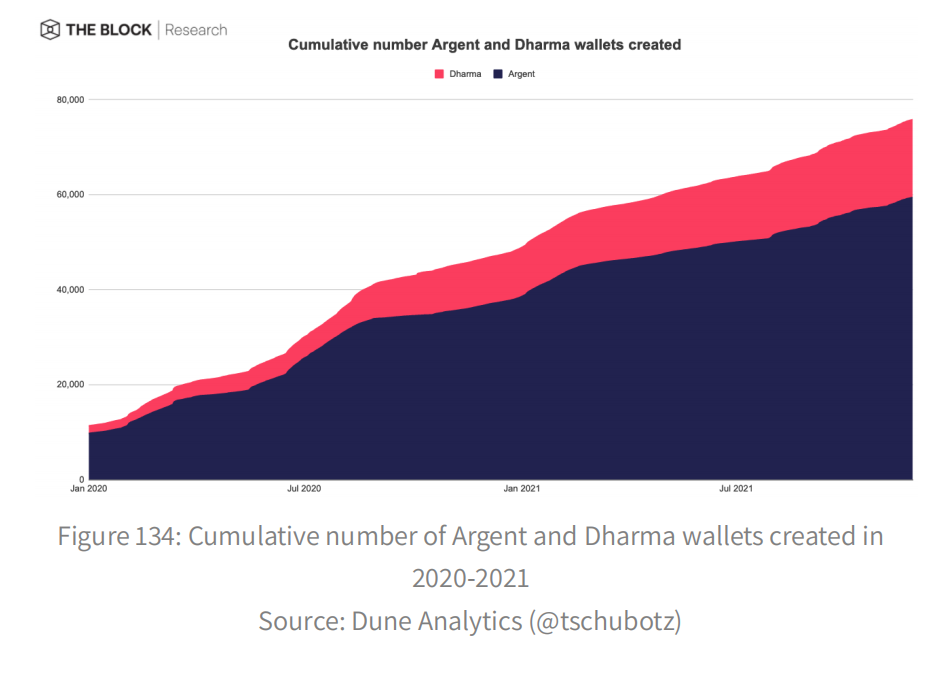

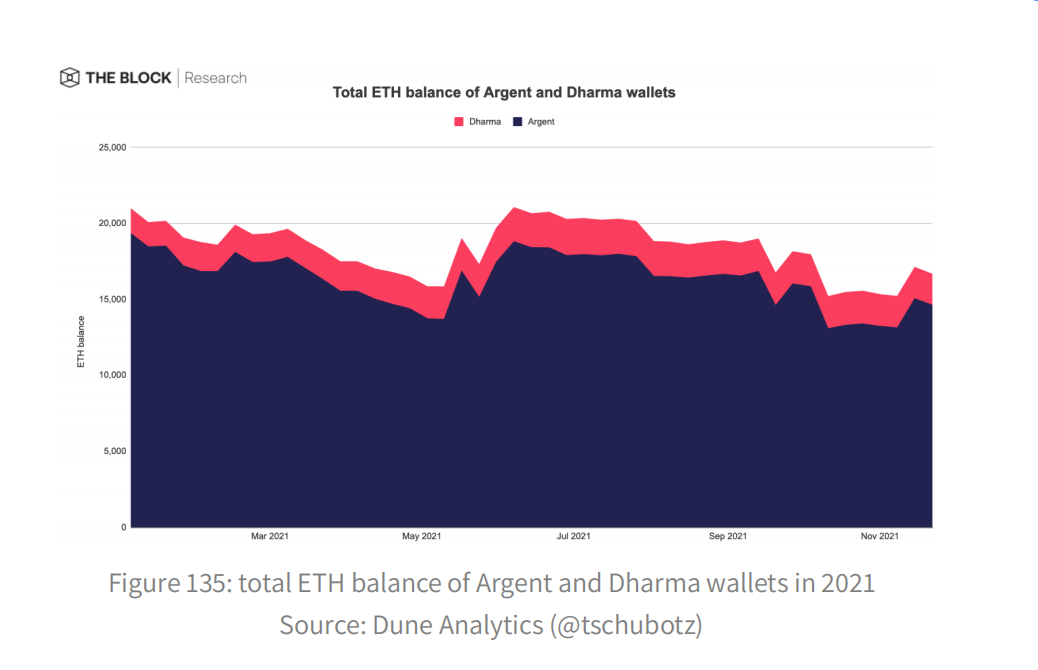

Smart wallets can also bring user-friendly features to wallet management. Argent and Dharma, for example, allow "guardians" of a user's choice to restore or limit access to their smart wallets. The cumulative number of silver and French wallets grew slowly, from 384,000 and 104,000 respectively, to 594,000 and 164,000 respectively in 2021. However, ETH balances in these wallets have declined by 20.6 percent since January.

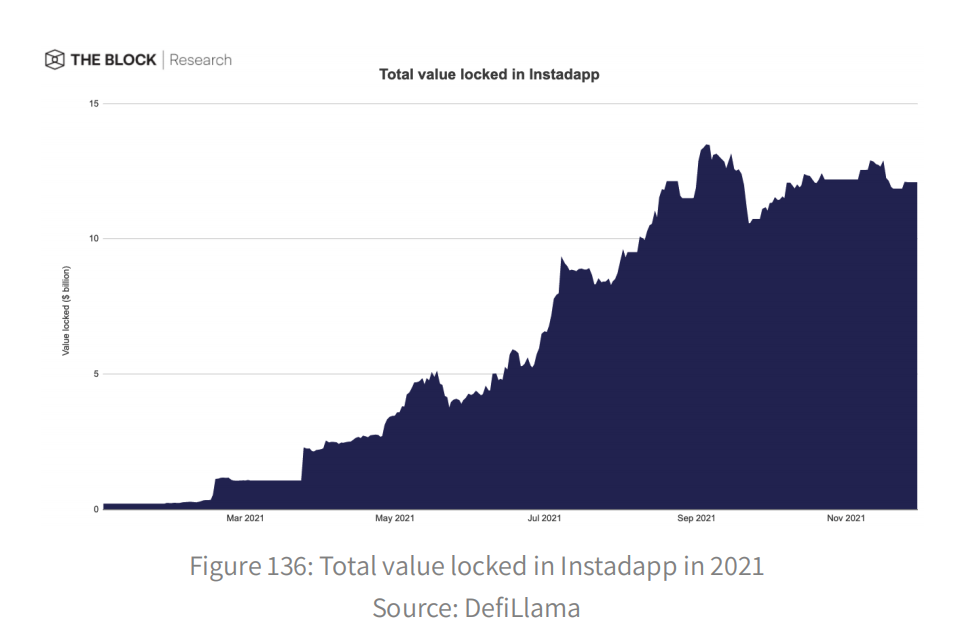

For advanced individuals, smart wallets like Instadapp and DeFi Saver provide a one-stop shop for managing DeFi positions on major protocols through custom automation, such as loan refinancing. Instadapp's TVL skyrocketed to $12.1 billion this year, driven in part by LM.

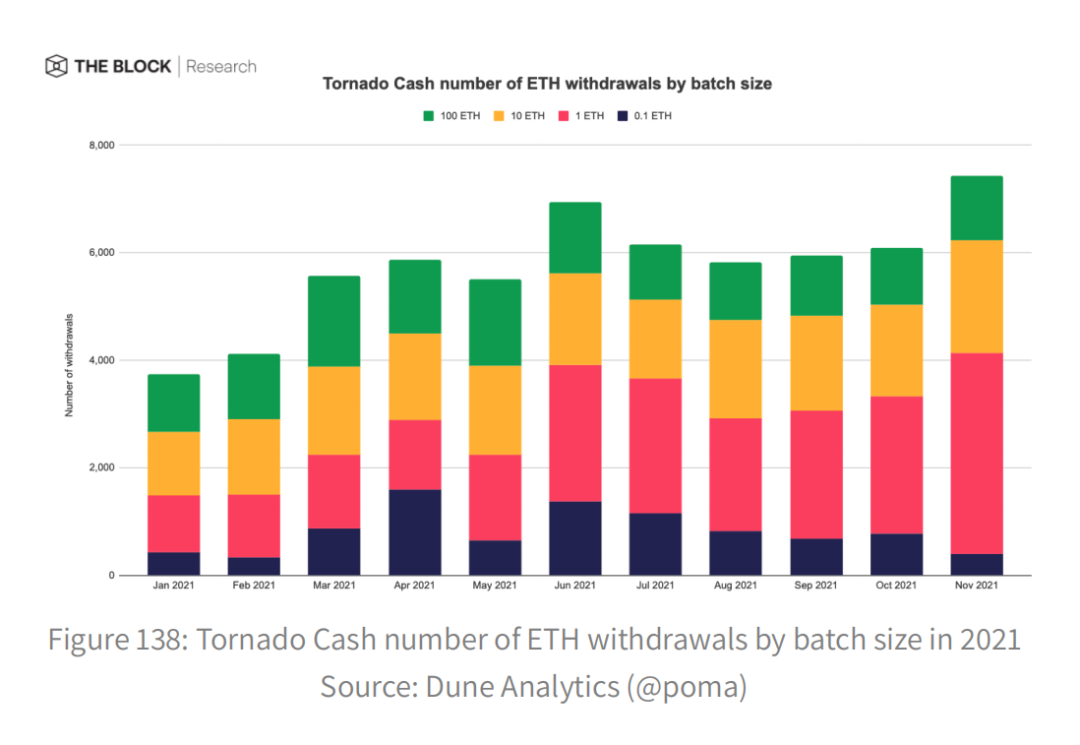

Privacy Tornado Cash remains the Privacy mixer on Ethereum. Its TVL grew from $55.1 million to $695.9 million in 2021, processing an average of $87.4 million in deposits and $86.4 million in withdrawals per week this year.

35.3 per cent of ETH transactions through Tornado Cash this year were 1ETH, while transactions of 0.1 ETH are becoming increasingly unpopular in high gas environments.

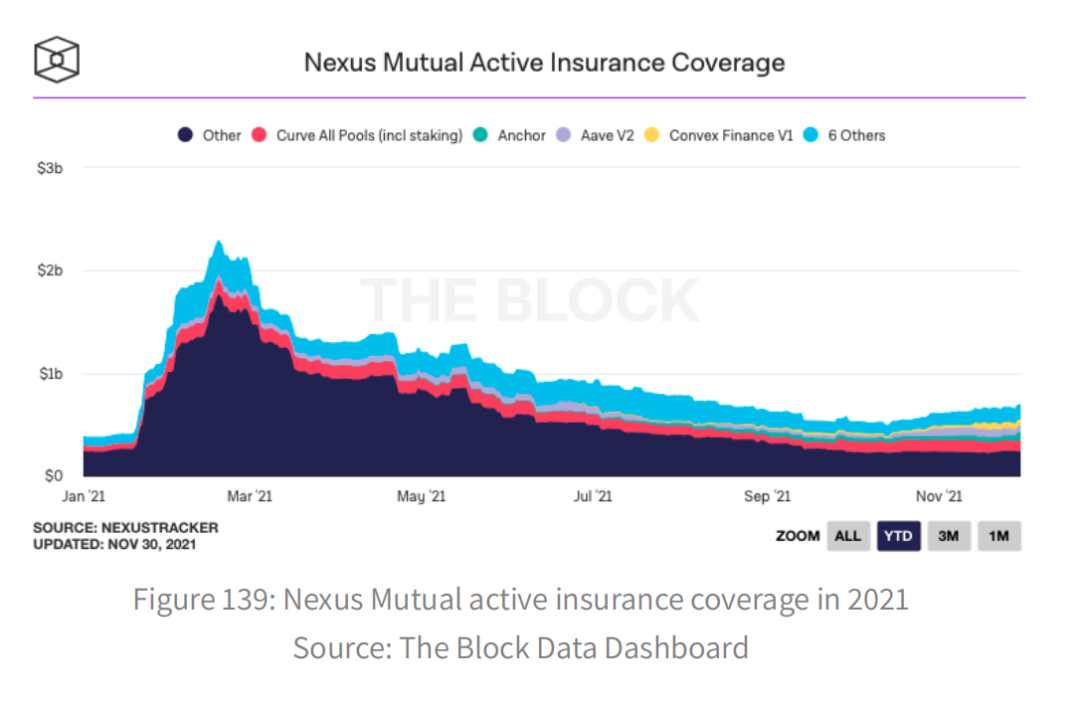

While most DeFi industries are booming in 2021, DeFi insurance is likely to be one of the few categories to decline. Active coverage by Nexus Mutual, a leading insurance solution, peaked at $2.3 billion in February and has since declined by 70.0% to $688.2 million.

Token service

Initial DEX issuance (IDO) refers to tokens issued through DEXs, which is one of the most popular token issuance methods. However, Naive IDOs, by seeding liquidity pools on DEXs, attracted the leading bots and grabbed a significant portion of the tokens, driving up market prices significantly. They then sell it for a profit. The liquidity channelling pool (LBP) pioneered by Balancer has emerged as a more favourable way to issue tokens this year.

The initial listing price will start with a high starting price to discourage leading competition. Prices will be adjusted algorithmically over time based on immediate purchase demand. It is similar to a Dutch auction, but more responsive to a surge in demand. On the other hand, initial Binding Curve Offering (IBCO), popularized by Hegic Protocol, has become the preferred token offering method for most Solana projects. Investors can deposit and withdraw funds during the sale, after which they can redeem the tokens on a pro rata basis. The more money raised, the higher the valuation of the implied token. Unlike LBP, IBCO offers the same settlement price for all participants of any size.

Some projects avoid IDOs and prefer to distribute tokens to protocol users, possibly due to regulatory concerns about token sales. Some speculators use this model to try to interact with protocols that have not yet issued tokens using multiple wallets, hoping for handsome returns in the future. This is known as "farming by air", and there is debate about the ethics of the practice.

Overview of the biggest DeFi vulnerabilities of 2021

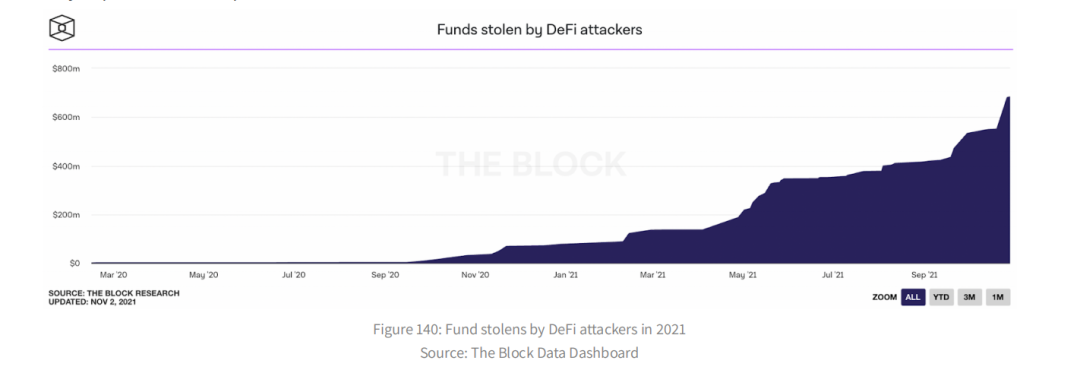

In 2020, the popularity of the DeFi protocol led to an increase in the user base and project TVL. In turn, big TVL attracted the attention of not only administrators, but also attackers, who stole more than $77 million through bugs in 2020. Most of the attacks happen in the fall because of summer DeFi. In this event, many forks are started with minimal changes, which is enough to cause a bug. It seems developers must learn their lesson and take responsibility for their users' money. However, history repeated itself due to a lack of sufficient number of security experts, less competition on other EVM compatible chains, and an inability to quickly upgrade fragile smart contracts.

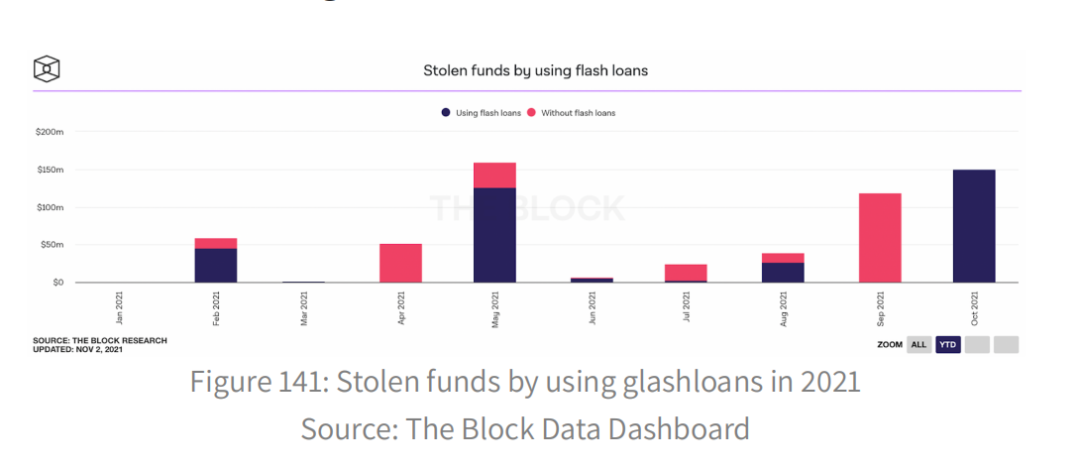

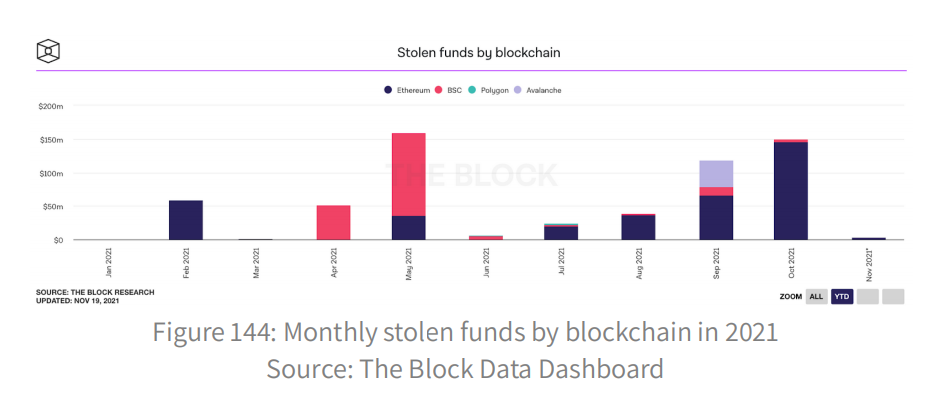

During the current year, the number of stolen funds increased eightfold, reaching $610 million as a result of 50 uses. The first known DeFi vulnerability involving bZx (02/15/2020) used a temporary loan. There is still debate about whether this primitive creature is harmful to the ecosystem. In any case, about 60%($355 million) of the money was stolen through flash loans.

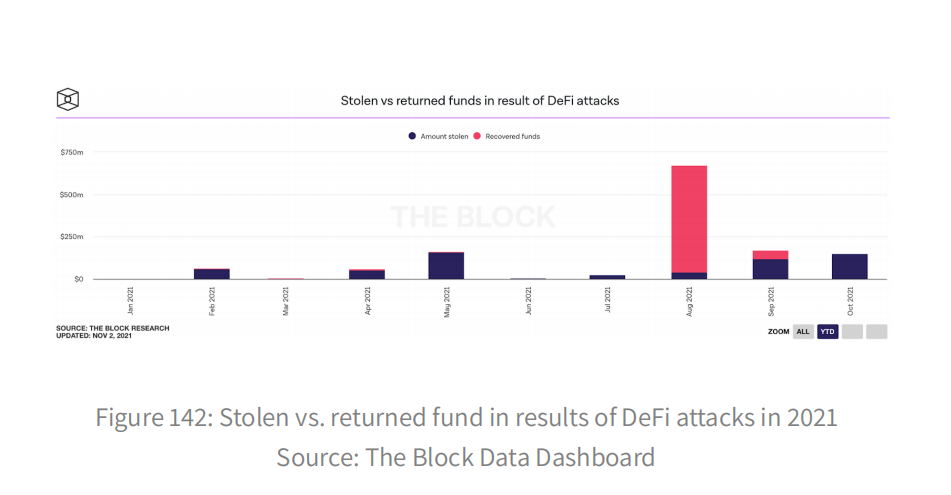

Another important point is that attackers can return some of the stolen money to the project. This usually happens if the attacker agrees to the bug bounty or if their identity is known. Overall, 53 percent ($704 million) of the stolen funds in 2021 were returned to projects, mostly due to poly network development.

The latest insights confirm that we live in a multi-linked world. While most of the bugs are still on Ethereum, there have also been bugs on BSC, Polygon, and Avalanche since April. About a third of the stolen money, or $200m, belonged to the balanced Scorecard programme, which suffered the biggest loss in May.

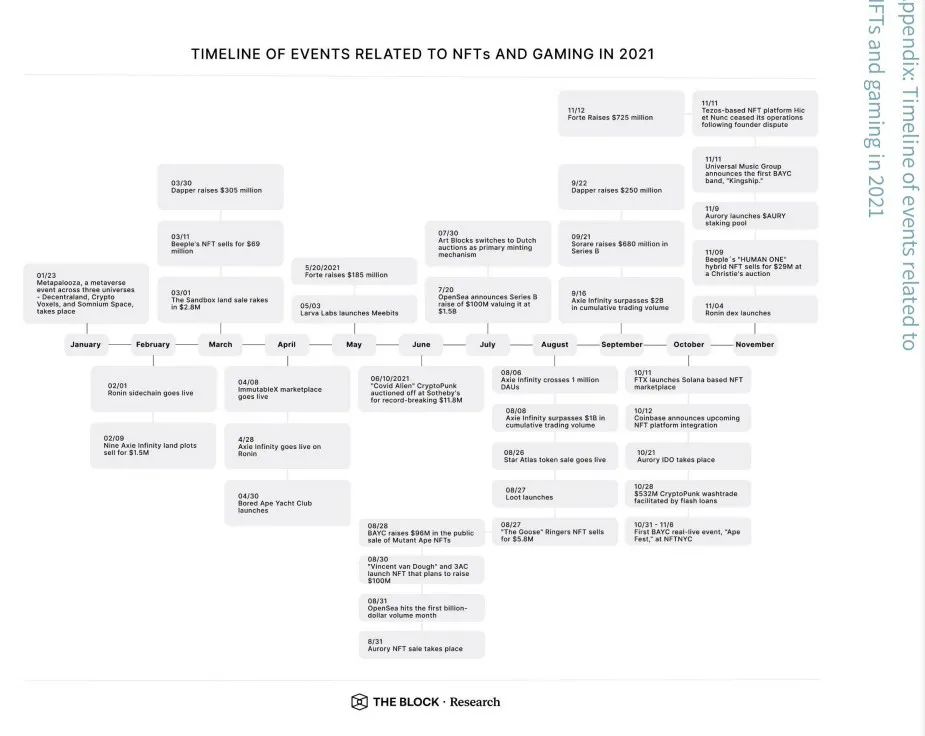

You can find a timeline of all major hacks that took place in 2021 in the appendix in the DeFi section.

DeFi's competitive prospects in 2022

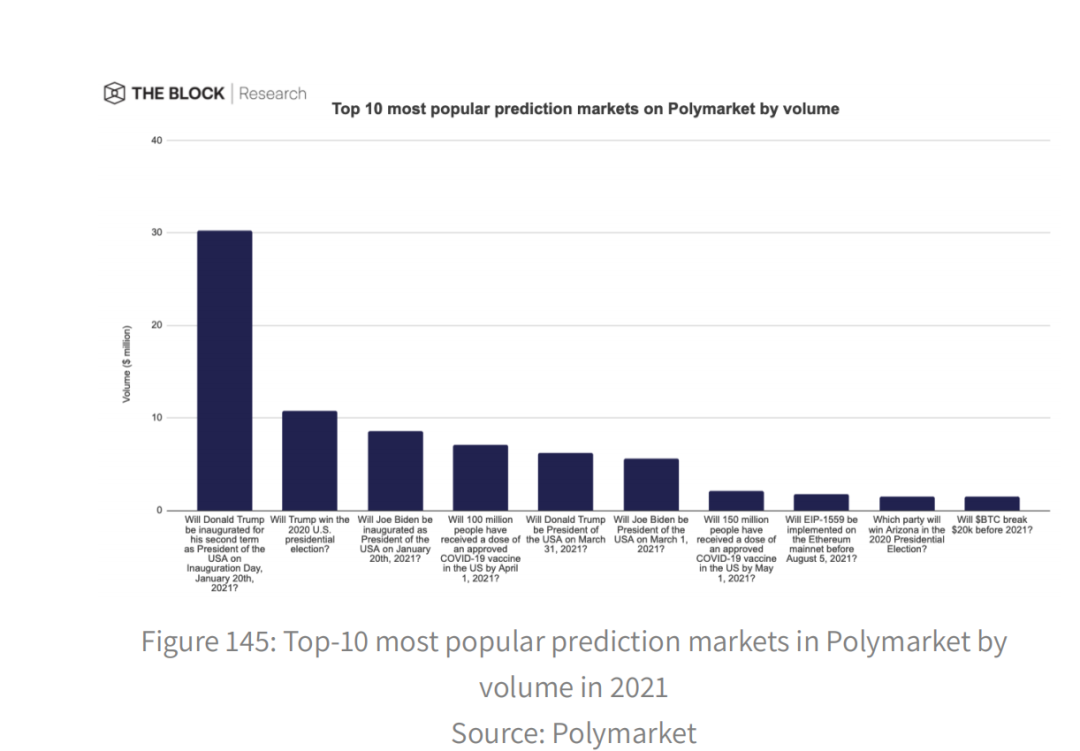

Prediction markets were one of the first concepts of decentralized applications implemented on blockchain, such as Augur. Despite its early start, it has failed to generate meaningful volumes compared to other categories of DeFi protocols. Polymarket on Polygon is the leading forecast market for 2021, with hot markets showcasing major global events (like the US presidential election and COVID-19) and cryptocurrency trends (like Bitcoin prices, Ethereum upgrades). Surprisingly, sporting events do not attract as gamblers prefer traditional regional bookmakers rather than for better liquidity.

As DeFi becomes friendlier, decentralized predictive markets have the advantage of reaching more users globally, thus providing more competitive rates and deeper liquidity. Retail investors are likely to prioritize user experience over decentralization, while companies that can provide frictionless on/off ramps are likely to get a head start in grabbing market share. Multiple markets currently rely on centralized event prediction for settlement purposes. Going forward, as prediction markets gain traction over time, the market resolution process should make use of decentralized event predictions that are economically sound and resistant to corruption. Whether this can be achieved quickly is questionable, but what is certain is that full decentralization is not currently a priority for predictive market platforms.

Non-dollar stablers;

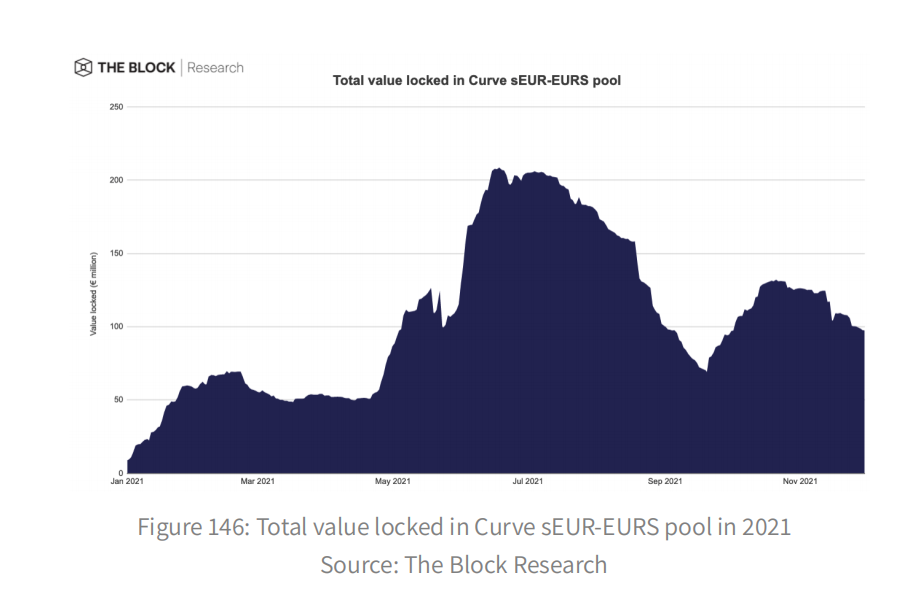

Most stablecoins are pegged to the U.S. dollar, as stablecoins are primarily used to trade cryptocurrencies in dollar pairs. While there are plenty of stablesoins linked to various fiat currencies, the demand and liquidity do not exist for most of them. Nonetheless, the euro stablecoin is likely to be adopted in the coming years. First, the euro is the second largest stablecoin bloc. There are already two staboins pegged to the euro in the DeFi space. SEUR is Synthetix's synthetic euro with a market cap of $118.7 million, while STATIS Euro (EURS) is the largest euro-linked stabocoin issued by STATIS with a market cap of $102.2 million. Their demand is largely driven by Curve's incentivised EURs pool, which has a TVL of $109.8 million.

Second, the EU's positive steps and relatively more welcoming attitude towards resolving legal issues surrounding staboins and other cryptocurrency assets could lead to greater adoption of DeFi in Europe. The crypto Asset Market is a proposed regulation that will create a federation-level licensing framework to provide regulatory transparency to a variety of crypto service providers, including stablecoin issuers. The Euro stabler will play an important role in facilitating such adoption.

Tokenization of real assets

While cryptocurrency as an asset class has matured into a $2 trillion market, it remains relatively isolated and isolated from other economies. As the token economy grows, everything of value, whether financial or cultural, will be tokenized in some way. Closing the gap between real World assets (RWAs) and DeFi can bring great "old wealth" to the new digital economy and enhance the emerging DeFi ecosystem. Tokenized RWAs benefits from the existing blockchain and DeFi infrastructure.

For example, Centrifuge is a blockchain that facilitates tokenization of RWA like NFT and provides financing for different types of tokenized assets through DeFi. Tinlake is the investment gateway for centrifuge's RWA capital pool, holding over $44.4 million in TVL funds across 10 RWA capital pools. Tinlake's real estate bridge loan pool financer, New Silver, funded its first loan with an initial $5 million line of credit, becoming the first company to use RWAs to back Maker's DAI stablesoin. Soon, todate RWA loans could be used as collateral for Aave.

Innovation in derivatives

DeFi has fostered countless experiments over the years, and that's unlikely to stop anytime soon. Just as centralized crypto exchanges revived permanent futures, enabling futures markets for then-illiquid crypto assets, DeFi is poised to revolutionize the derivatives market with creative and novel designs.

Permanent futures never expire and do not need to be delivered. In addition to significantly simplifying users, it also provides liquidity providers with greater capital efficiency by consolidating liquidity from multiple maturities into a single market. The same framework applies to the crypto options market, which suffers from fragmented liquidity and high rollover costs. The money paid for the "perpetual option" would be a function of the difference between the marked price and its intrinsic value (i.e., the volatility premium).

The novelty and complexity of these instruments may lead to mispricing at first, but it will become more effective as the market matures. In addition to perpetuating options, other potential derivatives include power perpetuations designed to maintain the convexity of options while consolidating futures liquidity, and floor perpetuations that track the lowest price of a particular set of non-fungible assets. Despite the promise, most of them will have only limited success without incentives.

Guided flow

Fluidity produces volume. Most DeFi projects fail to harness network effects and create self-sustaining momentum because they are unable to attract short-term and sustain long-term liquidity. LM's ubiquity may have demonstrated its short-term effectiveness, but questions remain about its efficiency and sustainability. In terms of efficiency, the existing LM incentivizes liquidity over the entire price range, from zero to infinity. This is a misalignment of resources, since most liquidity is never used.

Only a few projects, such as Instadapp, focus on incentivizing liquidity on a narrow scale on Uniswap V3, probably due to unfamiliarity with the implementation of a centralized LM. We will see the emergence of variations of LMS that reward loyal liquidity providers for providing meaningful liquidity. Rewards can be weighted by a basket of liquidity-related parameters, including concentration, proximity to market prices, loyalty, and so on. LM provides diminishing marginal utility in terms of sustainability.

Mercenary liquidity providers sell off their returns, creating huge selling pressure and devaluing return tokens so that yields fall over time, causing liquidity providers to reduce their liquidity. Ultimately, LM is the overhead of an agreement to one day reach escape velocity. This amounts to renting liquidity from mercenary capital, and the objectives of the agreements and liquidity providers are inconsistent.

Recently, Olympus DAO proposed the idea of protocol-owned liquidity (POL), which goes without saying. Since decentralized agreements cannot eliminate liquidity, at least not without thorough process of governance approval, the liquidity possessed by the agreements themselves is essentially permanent. Instead of renting liquidity from mercenary capital, the agreement buys them directly by issuing bonds, by which the agreement trades tokens in exchange for liquidity of said tokens. Whether POL and bond sales can revolutionise the art of bootstrap liquidity remains to be seen. Nor would it be shocking to see other innovative approaches to this multi-billion dollar problem that affects all DeFi protocols.

Governance Reform & NBSP;

The interests of governance token holders and protocol users are inconsistent. Only 7% of users belong to these two groups, and the time span of users from these two groups is very different. Token holders generally prefer to maximize the extraction of short-term value, even at the expense of the long-term sustainability of the agreement. In contrast, protocol users prefer the longevity and neutrality of the protocol.

Maker is a classic example of this governance dilemma. MKR holders benefit from higher DAI loan rates, while borrowers clearly prefer the opposite. If users can't rely on voters to make decisions that are in their best interest, users will turn away. The curve's voting lock solves this dilemma.

Curve's native token CRV does not directly provide voting rights. However, CRV holders can lock tokens to receive veCRV, which grants the holder voting rights. The longer tokens are locked, the more VECRVs (and votes) they will receive. That way, curve voters have a vested interest in DEX's durability. Moreover, liquidity providers on Curve can earn higher returns if they acquire and lock in CRV, thereby motivating users to actively participate in governance. Different implementations of vote locking are likely to be widely used in DeFi governance to realign interests among stakeholders.

Bifurcation challenges

Institutions are eager to put money into DeFi but face numerous obstacles due to regulatory uncertainty, ranging from KYC/AML practices to securities law related concerns. Some protocols foster the concept of "permissive DeFi," which, forgive the oxymoron, can satisfy existing compliance requirements. Some argue that such developments defeat the purpose of DeFi. Still, distrust is not the answer to everything. Some applications require trust from certain parties, such as borrowers and facilitators of unsecured loans, RWA toxified trustees, etc.

Open finance should not just decentralise all aspects of finance, but bring choice and transparency to users. These projects will be able to obtain war funding from institutional giants who have never had access to DeFi. Some existing decentralized agreements, such as Aave Arc and Compound Treasury, are also developing a separate division to cater to institutional clients. Still, most agreements are unpermissioned, and more and more developers of such agreements will remain anonymous. They will speed up the process of full decentralisation and avoid scrutiny at all costs.

The threat of restricted access will also accelerate the development and adoption of a privacy-enhanced DeFi ecosystem driven by zero-knowledge technologies. Today, many "decentralized applications" rely on centralized components, such as centrally managed user interfaces, proprietary routing optimization algorithms, and so on. As regulatory pressure mounts, they will be forced to pick sides. Some companies will comply with and enforce KYC processes, or restrict users' use in certain jurisdictions; Others will remain anonymous, giving up control of the front end and smart contracts. Regardless, a DeFi fork seems inevitable.

Chapter 6: Web3:2021 overview & NBSP;

Look at Web3, the technology that pushed the web to a turning point, and explore the latest data to see where we're headed.

The profile

- As Web3 matures, it is important to have frameworks to understand its technology organization and interactions, and how they generate new user experiences;

- To this end, we develop an integration model for Web3, which describes Web3 as a "horizontal" evolution of Web2 technology;

- Here, we explain the new framework and delve into its aspects, from the technical details of simplifying access to blockchain data to the numbers and numbers behind recent Web3 economic activity.

In November, Solana, Lightspeed Ventures, and FTX announced a $100 million fund for Web3 game development to support game studios and technologies that integrate Solana into desktop and mobile games.

Bumble revealed that they're exploring how to incorporate blockchain and encryption into the reboot of their dating platform BFF through the "Web3 lens."

Crypto venture capital firm Paradigm announced a massive $2.5 billion fund to develop Web3 applications, noting that the journey of Web3 and encryption is just beginning and that Web3 applications currently only reach a fraction of the audience that Web2 does.

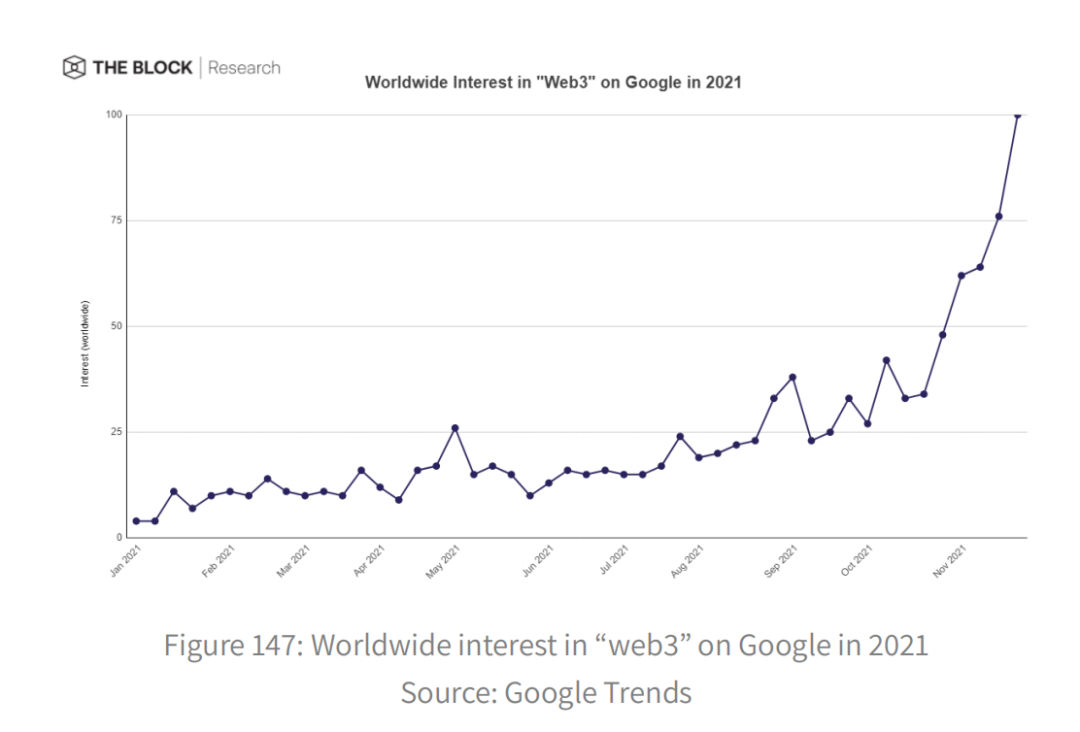

Global interest in the term "Web3" also hit a record high on Google in November, up about 150 per cent since the beginning of October. The Y-axis below is a measure of search interest relative to the highest point between January 1 and November 30.

Despite all the hype, there is still a lot of confusion about what Web3 is.

We have developed an integration model for Web3 that focuses on the technological evolution that is taking place at the Web architecture level. Next, we'll discuss this model, its context in the history of the Web, and how developments on the back and front ends of the Web have led to major changes in the way people use and experience the Web.

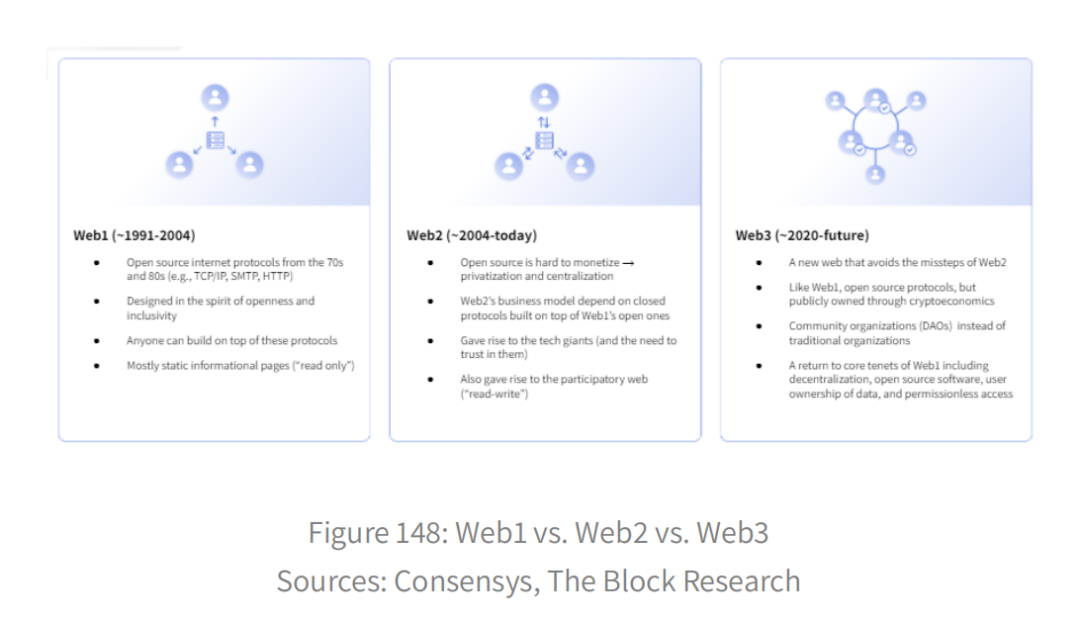

A simple framework for understanding Web3 technology

In a sense, "Web3" (e.g. "Web2") is just a buzzword used to encompass a new set of phenomena on the web. These terms can be misleading because the web is constantly evolving and does not "upgrade" from one version to another at a time. However, periods of rapid development do occur during certain evolutionary inflection points.

In the case of Web2, growth is primarily about commercialization and possible social experiences on the web -- some of the key differences include turning users into first-class entities with prominent profile pages that can connect with many users and publish multiple forms of content, And internal messaging systems and common application programming interfaces (apis). In Web3, significant developments are taking place on both the back end and the front end, from the way data is stored and served to the novel user experience of integrating wallet applications and Web3 gateways. At the social level, there is a move towards more publicly constructed and owned networks managed by community-owned and operated organizations supported by blockchain technology. That being said, Web3 is still in its early days, and any claims of "revolutionizing" or replacing Web2 technologies are premature.

This may be due to a lack of clarity about how clients and servers communicate in Web3. Next, we try to address this issue by focusing on specific developments occurring at the client-server level of the Web infrastructure.

On the left, we show a simplified description of the technical infrastructure for Web2, the dominant form of networking since circa 2004. Essentially, Web2, also known as "participatory" and "social networking," consists of client and server computers that communicate over a network. Internet Protocol stack. In contrast to "Web1," which refers to the first phase of the Web's evolution from roughly 1991 to 2004, Web2 involved more two-way communication between clients and servers.

The increase in client-to-server communication capacity enables users to compose and update data in a secure, reliable, trusted, and scalable way that has never been possible before -- and therefore, sometimes. Web1 is referred to as the "read-only Web," while Web2 is referred to as the "read-write Web." These capabilities pave the way for new developments, such as user profiles, internal messaging systems and social networking platforms.

Looking at the server side, we noticed. Web content (for example, HTML/CSS, JavaScript, images, video), application logic (for example, for serving dynamic content over HTTP), and data (for example, data stored in database management systems such as MySQL) are stored on privatized and centralized servers in Web2. Web1, by contrast, is relatively decentralized, with static pages of information hosted primarily by web servers operated by various Internet service providers (ISPs) and free web hosting services. One reason for server-side privatization and centralization is the economic opportunity presented by the social evolution of Web2. This is the first time we've been able to create a thriving digital marketplace. As with any market, knowing your customers is critical to effective marketing.

As a result, we've seen the birth and explosion of digital marketing, the commercialization and commoditization of personal data, and the competition among tech companies for data. To this day, the tech giants that survived the dotcom bust are in constant competition to find ways to capture and control that value. Power is concentrated by a few companies that control these precious resources -- for example, the cloud infrastructure market is dominated by a few tech giants (e.g., Amazon, Microsoft, Google). Essentially, the line between client and server becomes blurred in Web2, because the client also "provides" valuable data and resources to the server. In the process, customers lose ownership of these data and resources because they typically do not own or operate server computers.

Web3 technology, decentralization, and "propaganda"

Now it is clear that the Internet has lost its original one of the core principles: "don't need permission from the central agency can publish any content on the Internet, there is no central control node, so there is no single point of failure... and there is no" stop switch "! It also means not affected by indiscriminate censorship and surveillance." The decentralized vision of networks has been replaced by the reality of digital territories controlled by monopolistic technology companies. But after a long period of rigidity, the tech industry's top-down structure is showing signs of weakening.

Critics have voiced concerns about censorship, surveillance, misinformation and user exploitation, and antitrust regulators are cracking down on big tech companies to root out monopolistic practices. At the same time, we have had an influx of talented developers working to build a new version of the web that respects its original utopian vision of upholding the principles of freedom, inclusion, community and civility. As Tim Berners-Lee, the web's inventor, put it - "a web that works for everyone".

But as the past two decades have proven, building scalable and secure DApps is hard. It seems that combining decentralization with the user experience we are used to and need in Web2 is computationally infeasible on a Web2 infrastructure. Server-side centralization may also be the only viable computing solution to meet the needs of Web application users. Fortunately, decentralized solutions may exist in blockchain and related technologies. Bitcoin, for example, is a blockchain-based application that currently operates in a distributed fashion on a large scale, with approximately 14K full nodes and counts accessible. Technical security increases with the size of the network and the value of individual users, and the appeal of non-users increases with network effects. As a result, talented developers around the world are looking in this direction for a way to build a new network that avoids Web2 missteps.

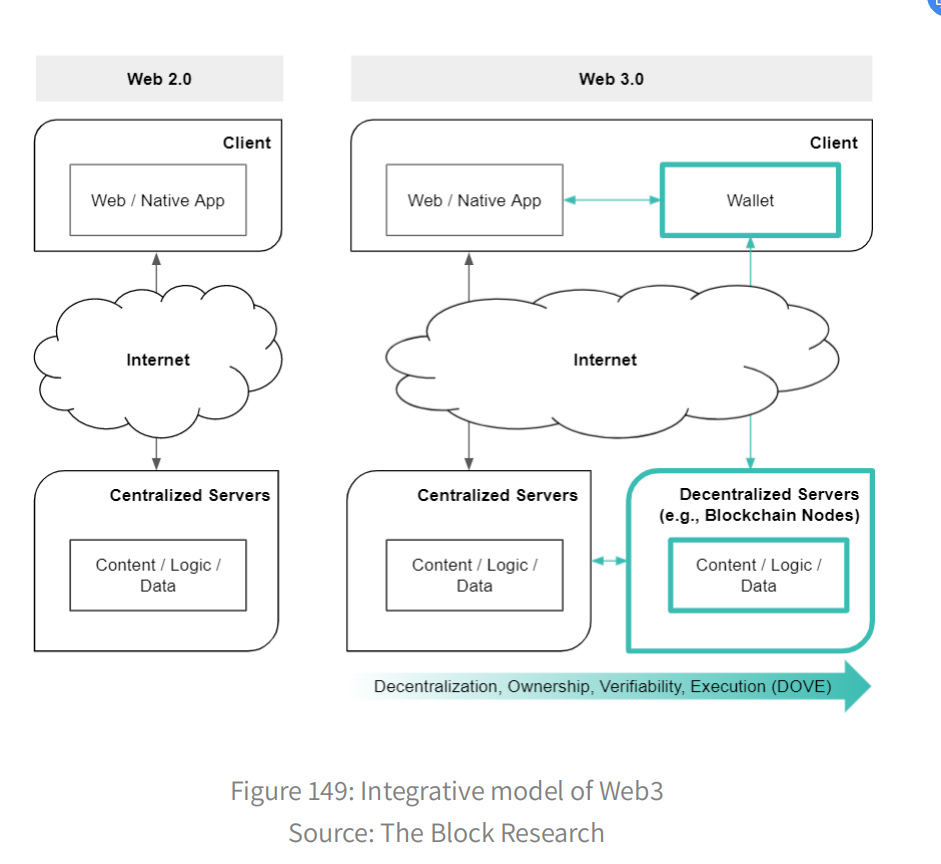

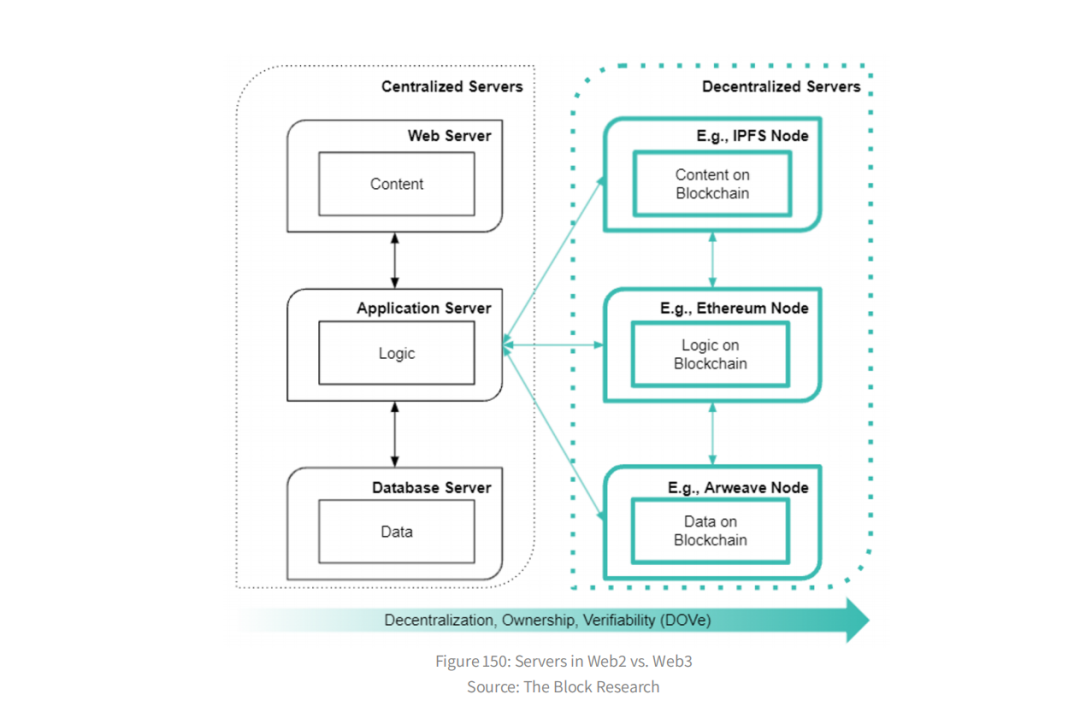

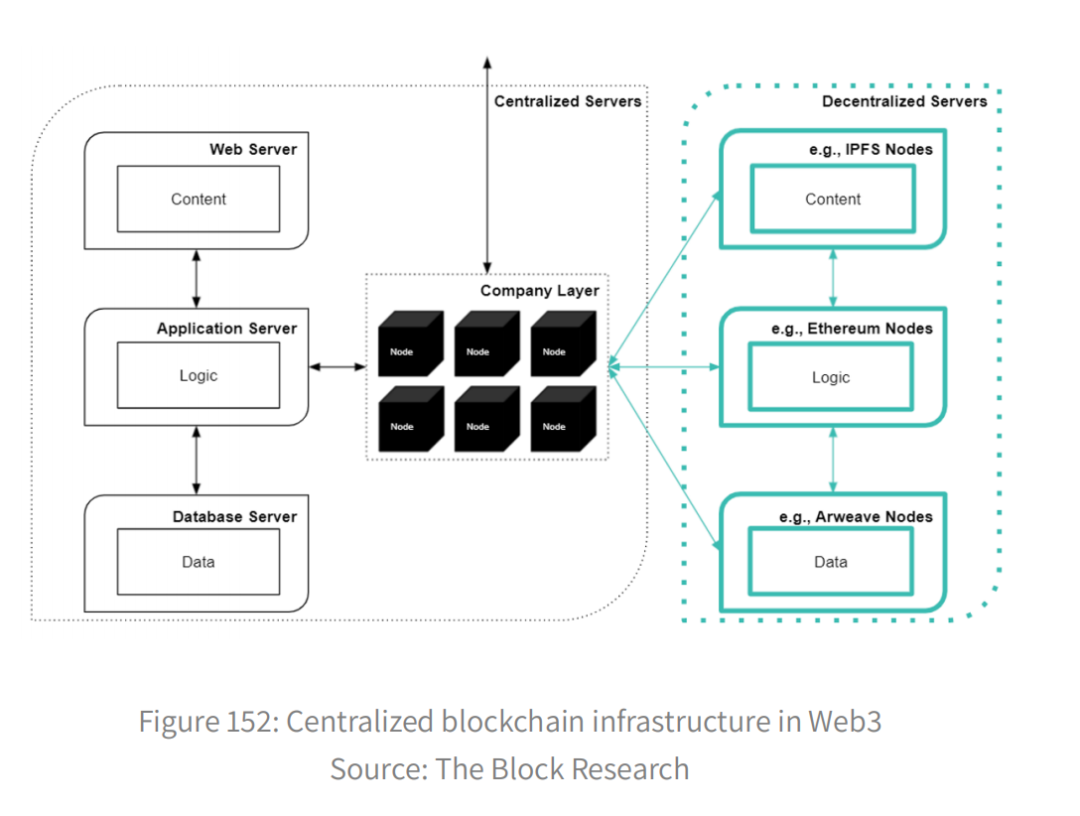

To understand the major technical differences of this new network, let's first review the major server-side developments. In the figure below, we zoom to the bottom of the Web3 diagram to provide simplified instructions on how to store and communicate various data structures in Web3. In Web2, we store Web content, application logic, and data in a centralized Web server, application server, and database server, respectively. User actions performed at the front end of the application initiate a series of information requests and responses at the back end. For example, an HTTP request sent from a client browser can trigger the Web server to communicate with the application server through API calls and the application server to communicate with the database server through SQL queries. The HTTP response is then sent from the Web server back to the client that contains the relevant information.

In Web3, data structures currently stored in centralized Web, application, and database servers can be stored separately in decentralized IPFS, Ethereum, and Arweave nodes. A centralized application server can request data stored in these decentralized servers (that is, blockchain nodes) via remote procedure calls (RPCS) and then provide relevant information to a centralized Web server. In addition, blockchain nodes can send relevant information via RPC to a Web3 front-end application, such as a wallet (for example, MetaMask) or a gateway (for example, IPFS gateway). This is just an example; other Settings are possible. For example, content such as HTML can be stored on the Arweave node, and data sets can be stored on the IPFS node. Application logic, create-read-update-delete (CRUD) commands, and financial execution can be implemented on Solana nodes or other decentralized computing platforms.

Decentralized design

One of the key choices developers need to make when implementing Web3 technology is the degree of decentralization they want to give their designs. The common misconception is that "Web3" and "Web2" websites and applications exist, but the reality is less clear, and applications now have access to a Web3 back end, opening up even greater potential for decentralization. Initially, the goal of many developers was to maximize the spread of their applications, but this has proven to be idealistic due to the slow and expensive nature of today's blockchains. In the short term, "Web3 applications" are likely to still leverage the Web2 infrastructure to some extent (perhaps we should label them Web 2.1, 2.2,... 3.0 applications to ensure accuracy). For example, Uniswap.org and other popular DeFi applications host their front ends on centralized servers, and their domains are purchased from centralized DNS hosts.

The wallet

Going back to the overall picture of Web3, we can see that Web3 also comes with front-end development enabled by the new back-end development. Perhaps the most prominent development to date is the user wallet, which allows us to securely view blockchain information, such as account balances and transaction histories. Importantly, we can "own" wallets -- so-called "self-hosted," "unhosted," or "user-controlled" wallets -- in software or hardware.

Ideally, the owner, and only the owner, has full ownership and control of the private key that accesses the wallet. In other words, the wallet software does not copy the private key information, preventing a third party from controlling the wallet in any way. Note that what we "own" is actually a private key for accessing a typical public address linked to common user data, such as account balances replicated and stored in a decentralized manner across many servers. Another option is "managed" or "hot" wallets -- these are typically controlled by centralised exchanges such as Coinbase and Binance, which manage user money through pooled wallets also controlled by the same entities.

As a result, they offer users less ownership and security, but also less responsibility and more convenience. A software wallet like MetaMask can also act as a gateway for Dapps. To use dApps, users need to understand the state of the blockchain and be able to interact with it. MetaMask, for example, allows users to access Ethereum blockchain data through Ethereum nodes provided by Infura by default, opening access to the expanding universe of Ethereum DApps.

However, users can set MetaMask to access the Ethereum blockchain through another node provider or even through their own nodes. Alternatively, they can access the Ethereum DApp through a different wallet or through RPC's custom application.

Again, these capabilities point to a continuum of user control that is not possible on a Web2 infrastructure. If Web2 is about the shift to user prominence and social, then Web3 seems to be about the shift to user control and empowerment.

Decentralization, Ownership, Verifiability, Enforcement (DOVE)

At the bottom of the figure, it illustrates how the shift to a Web3 infrastructure contributes to four key changes in the user experience -- from decentralization to ownership to verifiability to execution (DOVE). We use the word "change" instead of "benefit" because every change must have costs and benefits.

Decentralization is an effect of the way servers are connected in the Web3 and Web2 infrastructures. A simple way to think about it is that data structures in Web2 are managed primarily by large servers controlled by a few entities, whereas in Web3 they are managed by smaller servers controlled by a large number of entities. Also, in Web2, access to the server side is limited to those who own server farms, whereas in Web3, access to the server side is inclusive, so that one person can actually own both client and server computers. The former system provides users with a data network that is easier to deploy, develop, and maintain but more prone to single points of failure, security risks, and privacy intrusions. The latter systems promise open and trustless infrastructure, censorship resistance, and no single point of failure, but tend to have lower throughput, require more computing resources, and are more complex to implement and coordinate.

Ownership is the effect of the native state of the Web3 blockchain layer -- the way we keep state or history publicly by running nodes, which is guaranteed by consensus rules, rather than relying on private information brokers (tech giants) and gatekeepers who act as creators of both parties to our own user state and history. In other words, due to the lack of native state in Web2, the user has no history -- no data, identity, security, or transactions -- and no requests for these from trusted intermediaries. In this way, the state properties of the Web3 infrastructure lay the foundation for a trustless infrastructure in which mediations can be removed without losing functionality. However, ownership comes with responsibility. In the absence of a mediation, we gain user control at the expense of the services of the mediation.

Verifiability is the effect that blockchain data is publicly available through a fault-tolerant group consensus mechanism. In the case of a truly decentralized blockchain, anyone could download and verify the entire history of verified blockchain data. With no intermediary entity between users and their country, blockchain "belongs" to everyone equally and fairly. In this way, decentralization and ownership are verifiable like never before. They can directly verify selective and copyrighted information about what we own and what others own, making it possible for parties who do not know each other to reach value agreements over the Internet for the first time. The downside here is to implement verifiability;

Fault-tolerant consensus mechanisms require an extreme form of cross-node data replication and processing that can quickly become computation-intensive. Execution is a smart contract executed exactly as it was written, with no mediations or closed protocols and opaque code. In other words, a smart contract is automatically executed, and the terms of the agreement between the parties it interacts with are written into open source lines. In addition, there are many open source smart contract libraries available that provide reusable building blocks for Web3 projects. It is in this way that Web3 returns to the open and inclusive spirit of Web1. Modular and open design allows for a greater degree of networking and community collaboration that is not possible in a Web2 framework. The challenge in this case is how network collaboration can develop and deploy applications at a pace that competes with centralized Web2 operations.

discuss

All in all, Web3 opens up the potential to openly own much larger portions of the web (again). It does this by building a base of linked data on the back end that we call a blockchain -- data that is decentralized, censor-resistant, verifiable and publicly available. These technological developments and the trust-free systems they produce have created what some see as a new layer of Internet value settlement -- a way to exchange value securely across the globe without borders.

The future will tell us just how valuable the new web quality brought about by the Web3 infrastructure will be. Now infrastructure has begun and time-tested Web2 combination of infrastructure, we can expect the developers would be more horizontally their platform and Web3 technology integration, to meet the users to decentralization, ownership, verifiability and implement demand demand will naturally consider the benefits and costs involved. One of the key challenges in moving to the Web based on distributed data is how users and developers can efficiently and economically bring blockchain data into applications. If Web3 is to be decentralized, a robust, secure, and economical node network infrastructure is essential. Next, we'll focus on the Web3 infrastructure that can leverage blockchain data in an efficient, secure, and economical way.

Centralized and decentralized Web3 infrastructures

Currently, there are centralized and decentralized operations that can simplify blockchain data access. For example, blockchain infrastructure providers like Infura and Alchemy provide portals to blockchain data, but they are developed, owned, and operated by centralized entities. On the other hand, projects like The Graph and Pocket Network already offer decentralized solutions for accessing blockchain data.

Decentralized access to decentralized data.

It seems that the future of Web3 will depend on a base layer of distributed, secure and immutable ledger data across multiple blockchains. Then, Web3 faces three key challenges:

1) How to efficiently transfer data from blockchain to application;

2) How to easily access data across multiple blockchains;

3) How to do A and B in A decentralized way.

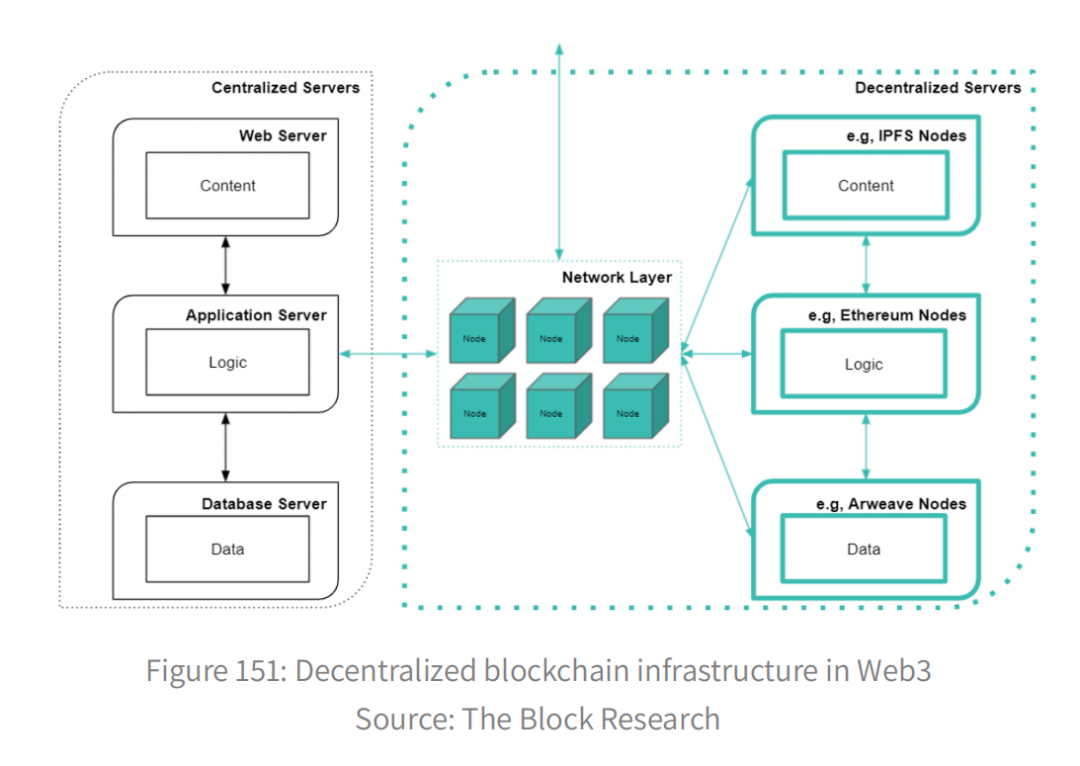

In a decentralized Web architecture, a reliable node infrastructure is critical for decentralized computing. A decentralized computing network can be divided into three general components:

1. Apps. These are any software that submits API requests (for example, queries, relays) that will be routed to any public or encrypted database node.

2. The node. They are decentralized servers that provide functions such as storing database indexes, sending session information to applications, servicing API requests submitted by applications, and storing network state such as account balances and work reports.

3. Network layer. The ecosystem that sustains the operation of decentralized protocols, including governance, protocol rules, the participants involved, and the economic games in which they play.

As shown in the figure below, relay or index nodes sit between applications and blockchain nodes (or other decentralized network of servers) from which they retrieve data. After processing the data from the blockchain nodes, they send the information to a centralized or decentralized application server.

Next, we'll explain how a decentralized computing infrastructure works with two sample cases: diagrams and project networks.

The Graph: Spread indexes and queries across a package

Web3 applications can query data from the blockchain by filtering or searching. Since blockchains store data and handle state transitions, the process can be slow and computationally intensive, but they don't index the data. Indexes make finding related data faster and less computationally demanding. Before The Graph, Dapp developers built their own database indexes for their users and clients. However, this approach reduces the credibility of the DApp by keeping the index data in a centralized database (rather than scattered nodes). Setting up your own index server is also redundant for many teams. In The Graph, The subgraph shows what data to store and how to store it. Although project subgraphs are usually defined by the project developer, anyone is free to define these subgraphs.

Next, the Graph node stores this data in a database index (creating a service subgraph), continuously scans for event changes on the relevant blockchain (for example, the Ethereum blockchain), and updates the data accordingly. Applications can then query the generated endpoints through GraphQL, making it possible to access cross-chain data indexes through a unified query language. Indexnodes were originally owned and operated by The Graph, but earlier this year, ten projects began migrating from hosted services to The Graph's decentralized main network. Ultimately, The Graph aims to realize its vision of a fully decentralized data economy. In this economy, the Graph protocol defines rules by which anyone can run or query a Graph node.

How does The Graph decentralize its anonymous vendors while providing service guarantees? It all comes down to the network layer. Like other decentralized computing solutions, this diagram has a network structure with the following four characteristics:

1. Supply (data providers) and demand (applications, users) meet in an open market.

2. Suppliers engage in an economic game (bet token) designed to ensure service assurance.

3. Suppliers' performance is checked by some mechanism (quality of their work is checked by encrypted certificates or "fishers" and rewarded for correctly reporting misconduct).

4. If providers are found to have failed in their duties, they will be punished in some way (losing part of the token they hold or not being selected to participate in income-generating services).

Graph utilizes the work token model, in which the Graph node provider lets GRT receive work index data defined by the Graph child Graph list. This model introduces an economic incentive for quality of service, as indexers may lose jobs or be cut (lose tokens) for providing incorrect data. The network layer or "query market" of the graph consists of four main players. The token incentive mechanism for these participants is designed to ensure high quality of service and provide token utilities.

Developers. These entities define the subgraph. Currently, they are typically developers of a given protocol, creating subgraphs of data for that protocol. In theory, however, anyone can create a subgraph of data from a public blockchain. Currently, developers have to pay for requests. Ultimately, The Graph envisions end users paying for their own queries when The second-tier solution is widely implemented in The Web3 wallet.

The indexer. These entities enable GRT to get work from The Graph network. Their work involves indexing blockchain data on the graph nodes of each subgraph list. Indexer income (and extension delegator income) comes from rewards for indexing work. The collective query fee of the agreement is allocated to indexers (and delegators) in proportion to GRT, and they also receive index rewards from GRT inflation of 3% per year

Curators. These entities indicate which subgraphs display better quality so that the indexer knows which subgraph nodes need indexing. Any developer can use decentralized blockchain data promoters, so The Graph Network needs these participants to identify useful participants. The administrator signals the indexer by marking GRT after a particular subgraph. For their services, they receive a portion of the query fee generated by the subgraph they signal. This share is determined by a combination curve that pays curators according to the early arrival time they signal, creating a predictive market in which curators can guess the future popularity of subgraphs.

The principal. These entities own the GRT by the indexer and share the indexer's indexing fees and query fees, which are set by the indexer. The client's interest in indexer is limited by the GRT interest of Indexer. It creates incentives for both sides. Delegators earn more by delegating to the "best" indexers, who index the most important subgraphs determined by the curator. Indexers earn more by "winning" their clients' money, which gives indexers an incentive to share their gains fairly with their clients. Currently, The Graph network has 7,306 delegates, 2,266 curators and 160 indexers. The figure is an example of how the network layer can successfully operate a decentralized computing network without the responsibility of a centralized entity. It demonstrates a working decentralized solution that brings data from the blockchain to the application and makes it easy to access data across multiple blockchains with a unified query language.

Pocket: Solve the node motivation problem

Like The Graph, Pocket has application, node, and network layers. Perhaps the main difference is that Pocket focuses on solving the specific problem that limits Web3's growth potential: the node incentive problem. The Graph, on the other hand, compares itself to a kind of "Google for Web3," aiming to organize the world's blockchain information and make it universally accessible and useful. For decentralized networks to flourish, it is necessary to develop a reliable nodal infrastructure. However, it is not practical for developers to both host their own complete nodes and provide back-end support for their own applications. As a result, Web3 developers rely heavily on centralized solutions, leading to centralized risks such as single points of failure, security risks, and privacy intrusions. There is currently a lack of reliable node infrastructure run by third parties.

One of the reasons for the lack of full nodes run by individuals and companies is the lack of native relay node incentives (other reasons include complexity and inconvenience of setup). To address this issue, Pocket Network encourages individuals and companies to deploy and run complete nodes for any blockchain with application requirements. With a combination of token incentives, cryptography proof, and pseudo-random selection algorithms, Pocket can create a reliable decentralized relay network in which developers can access cross-chain data with greater security and lower cost.

Again, the question arises, how does Pocket provide service guarantee through the decentralized service provider network that we don't know about? The lack of trust is again established through a decentralized network layer, although The rules and incentive schemes are different from those of The Graph.

Pocket's main difference is that it uses a session model, unlike The nodes in The Graph network, which are dependent on nodes storing indexed data. The Pocket node has three functions: providing session information to applications that contact it, servicing relay requests sent by applications, and storing information about the Pocket network state to assign work and validate work reports. Sessions are the mechanism the network uses to mediate the interaction between applications and nodes. They are data structures that use data stored in nodes about the state of the Pocket network to pseudo-randomly pair an application with a collection of up to five nodes in each chain to provide services for which the application pays.

Then, two key players in the Pocket network are applications and relay nodes, which are also validators and block producers for the Pocket Blockchain, which is based on tendermint's database and is used to ensure consensus about infrastructure provisioning between applications and nodes.

Nodes are rewarded based on the number of requests they serve during the session. Each relay (e.g., MetaMask call to get balance, get transaction history, send transaction, query smart contract) is serviced by the node and validated by the protocol, generating 0.01 POKT. The reward for each verified relay will be split as follows:

1) Service nodes account for 89%

2) 10% to Pocket DAO

3) 1% to block producers

Ultimately, Pocket Network will address the same core issues as The Graph, namely how to efficiently bring blockchain data into applications, easily access cross-chain data, and decentralize these processes. However, the scope is different, Pocket is more focused on becoming a unified cross-blockchain API through node motivation, while The Graph is more focused on becoming a unified search engine for blockchain data.

Centralized blockchain infrastructure technically, all we need to access blockchain data is a connection to a blockchain node. These nodes can be distributed across decentralized networks of individuals and companies, such as The Graph and Pocket networks, or they can be owned and operated by central entities, such as Infura and Alchemy. To illustrate the difference, see the chart below.

For blockchain data, the main difference between centralized and decentralized portals is that companies are responsible for maintaining the operations of the nodes -- all of their operations can be grouped into a "corporate layer." In addition to providing access to the complete archived node data, participants in the corporate layer can also decide to set up database indexes to facilitate queries involving filtering or searching. As with any centralized computing network, there are benefits and costs to this setup. On the upside, a centralized solution can make data networks easier to implement, develop, and maintain. For example, within a few years Alchemy and Infura were able to develop and release various tools to facilitate prototyping and development.

However, this introduces various forms of security risks and single points of failure. Infura's Ethereum infrastructure, for example, suffered a major glitch last year that delayed price feeds of ETH and ERC-20 tokens for popular services including MetaMask. It also caused major crypto exchanges including Binance and Bithumb to temporarily ban ETH and withdraw ERC-20 tokens. Infura says the roots can be traced to several components in its Ethereum infrastructure that were locked in an older version of the Geth client. Postmortem analysis has sparked debate about ethereum decentralization and over-reliance on centralized blockchain infrastructure providers.

Having said that, we note that Infura and Alchemy do not own or control the basic blockchain data, but rather serve as a centralized portal for decentralized data. If Invera or Alchemy fails, we won't lose blockchain data. If needed, we can use another centralized or decentralized infrastructure provider to access the same data. Or, we can build our own complete nodes to serve ourselves. One can make some comparisons with Internet service providers -- if Comcast goes out of business, we can switch to another Internet service provider to access the Internet.

discuss

Depending on the pros and cons involved, centralized and decentralized infrastructure solutions may play different roles in the next iteration of Web3. For example, if a part of the project requires advanced prototyping and development tools. In this case, a centralized solution like Alchemy or Infura might be a good fit for these parts. If other parts of the project are looking for unreliability and security, a decentralized solution like the Graph or Pocket Network might be a good fit for those parts. The vision is a new Web, much of it based on distributed, secure and immutable blockchain databases, communicating through centralized and decentralized infrastructures.

Next, let's examine how some decentralized blockchain infrastructure is gaining traction by analyzing the numbers and drivers behind Pocket Network's recent surge in Network activity and revenue. By maintaining almost 100% uptime, we can see how these decentralized data providers can support the growing Web3 economy.

Case Studies:

Network activity

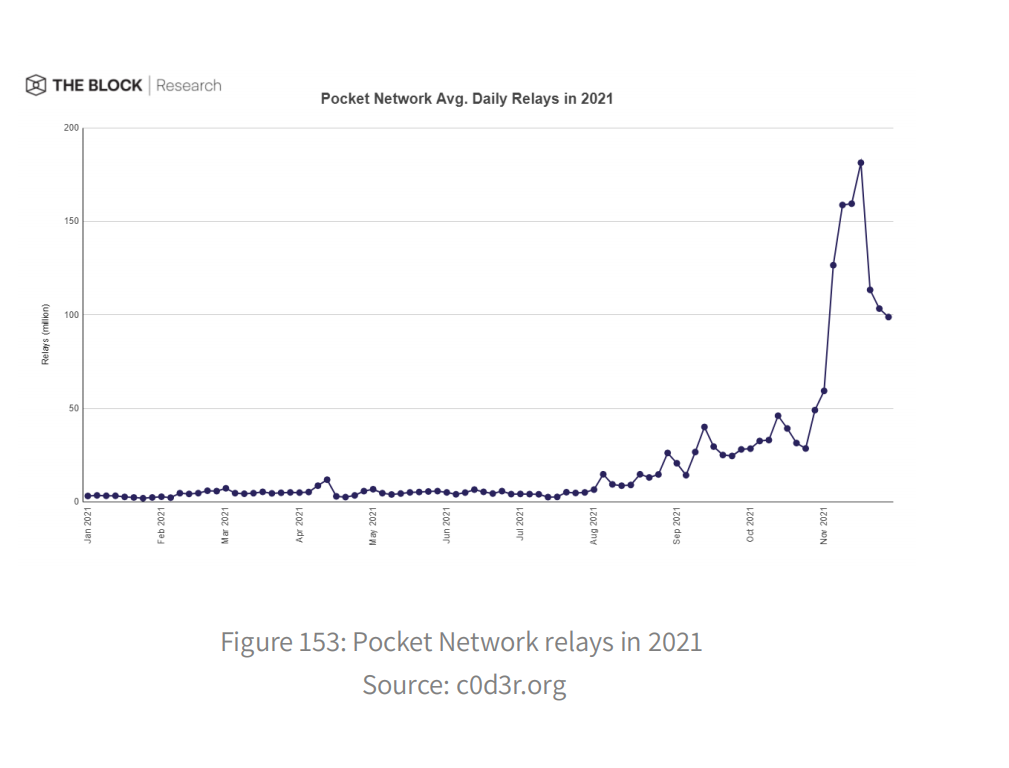

In order to study the usage and growth of Pocket before 2021, we first pay attention to the average daily power connection. Relays are only application requests for any common database node. The figure below plots average daily precipitation at 4-day intervals from January to November 2021.

Pocket Network usage has seen huge growth this year, particularly with the explosive growth of web activity that began in October. What are the main drivers? First, in February, Pocket Network announced that they would start providing the Ethereum infrastructure for Fuse, a platform for building decentralized payment systems. As an Ethereum side chain, Fuse requires a stable, well-functioning FUSe-Ethereum bridge. By integrating with Pocket, Fuse can further decentralize the platform, increasing user privacy while reducing the cost and efficiency of running your own Ethereum nodes.

Then, in August, Pocket announced support for xDai Chain, another Ethereum side chain that supports xDai staboins, which are bridged from Dai on Ethereum. One of the main use cases for xDai is to enable fast and low-cost transactions in the MMO space conquest game Dark Forest. Similarly, by integrating with Pocket, xDai can increase decentralization while "outsourcing" their Ethereum infrastructure needs.

More recently, network activity surged from October after Pocket announced it would handle Harmony RPC traffic. Harmony is a Layer 1 blockchain that can be used as an interoperable layer 2 extension solution for Ethereum by using random state sharding, allowing secure block confirmation at low cost and high speed. Harmony's network had between 50 and 100 million API calls at the time, and they were trying to re-route traffic through scalable and decentralized apis. Developers can now create Harmony RPC endpoints from Pocket's front-end API portal to use in their Dapps. These pocket-driven endpoints provide an additional layer of flexibility, reliability, and privacy for dApps.

In Pocket network, application peg is the entry point registered as an application in the network. The application locks the POKT into a binding within the network to receive throughput allocations performed over network node relays. The binding rule is determined by the monetary policy and protocol rules set by Pocket DAO. As the chart below shows, the amount of POKT that applications use to reserve relay requests has grown more steadily since the beginning of the year.

The daily reserve of relay requests is equal to the number of POKT bet by the application multiplied by 40. Then, we can see that the application has "paid" (invested enough POKT) to reserve nearly 1 billion relays per day while using about 160 million, or 16% of the reservation. This is not surprising, however, as applications should have a backup buffer to deal with a surge in network activity. Eventually, assuming these held tokens deplete the reserve of relay requests, the approximately 1 billion relays will be paid as "revenue" to relay providers, Pocket DAOs, and POKT block producers. Now let's look at these benefits and rewards in more detail.

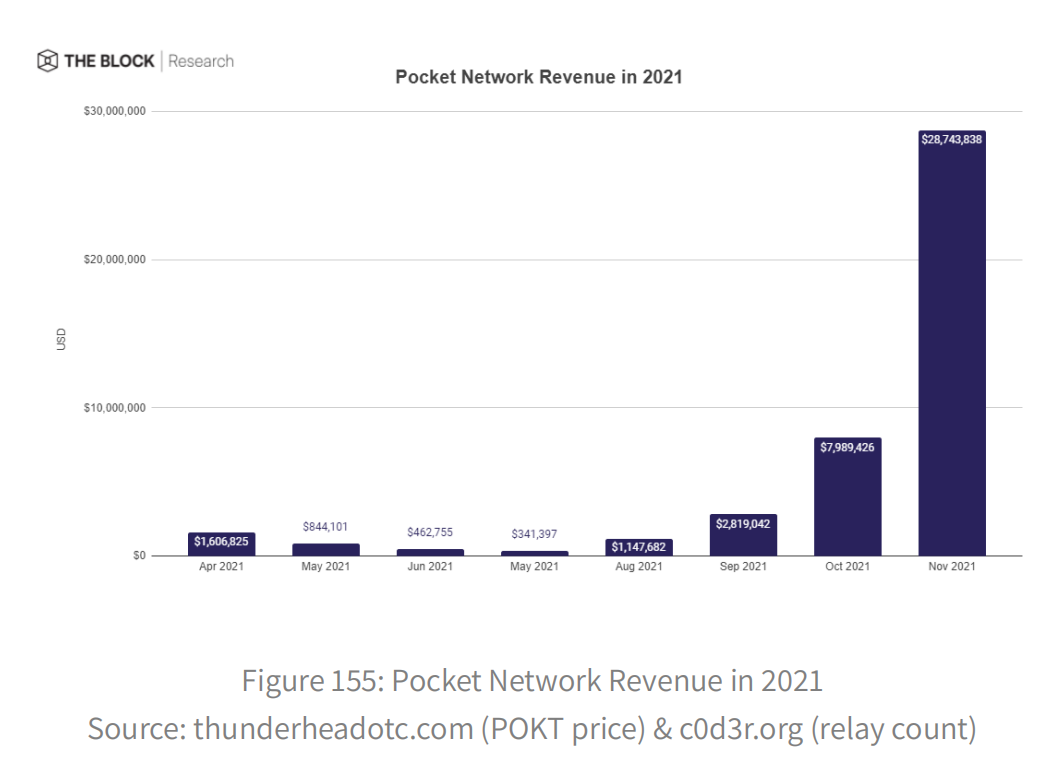

Income and return

To convert trunks into revenue, simply multiply the number of trunks by 0.01(number of POKT generated per trunk) and POKT price. The figure below shows monthly POKT revenue for 2021, based on average daily access points and monthly POKT prices. Price data is available from April to November.

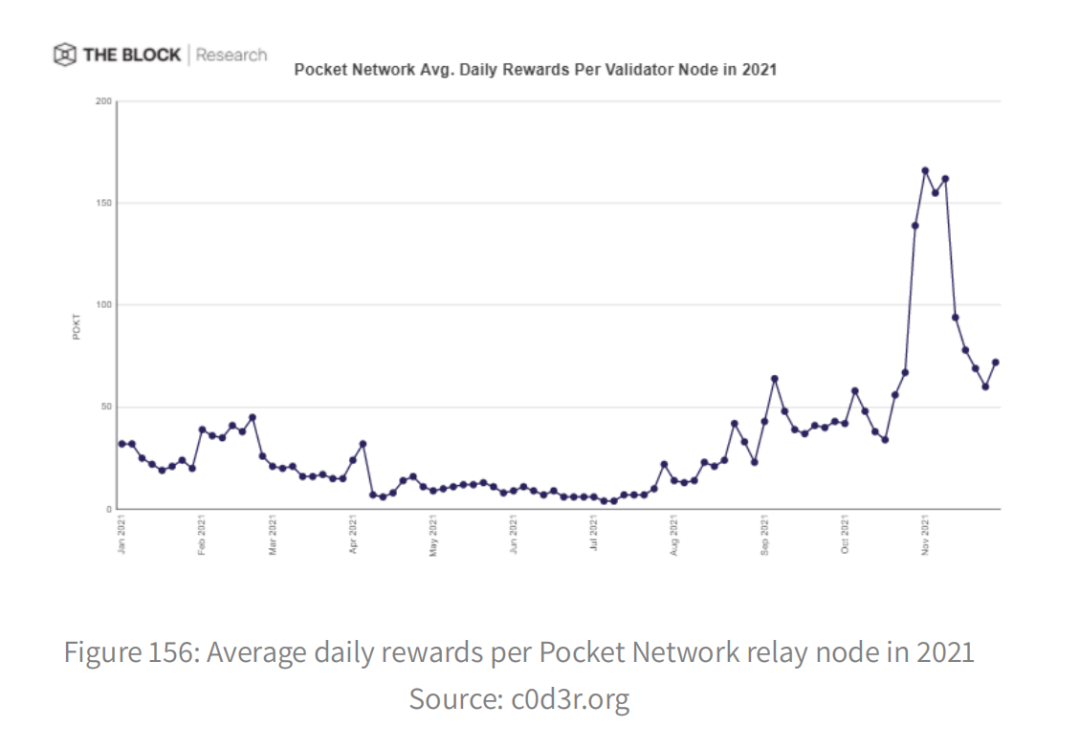

Network activity decreased from May to July, at the same time as overall activity in the Ethereum network and crypto market decreased. But Pocket apparently saw a big jump in revenue this quarter after building terminals that connect to Harmony's network. We can also look at how many POKT get per relay node the number of relay nodes divided by the total number of relay nodes and multiplied by 0.89(from 89% of distributed POKT service nodes, pocket knives,10% and 1% block producers). The chart below shows the average daily rewards for each verified node from January 1, 2021 to November 8, 2021, four days apart.

At the beginning of the year, POKT nodes received more daily rewards because there were fewer nodes in the network. The chart below shows the number of active validator nodes in the network from January 1 to November 8, four days apart.

To date, active validator nodes have increased more than 15-fold since the beginning of the year, from just over 600 nodes to over 9000 nodes today. This month, the average daily rewards per validator node soared to an average of 161 POKT(~ $118 $0.73 / POKT) per node per day, coming out over 300% of the minimum number of POKT rewards per node in the network (assuming a share of 15150 POKT per node).

These rewards are not necessarily sustainable in the long run. Attractive returns may lead to more node providers, further separating the total verifier reward from the POKT reward paid through supply dilution (creating 0.01 POKT per delivery). There is also the question of whether compensation paid through supply dilution should be considered income. On the one hand, they do represent the real needs of Pocket services. On the other hand, the interests of the application and nodes will be diluted every time the work is performed on the Pocket network.

At the November peak, that would add about $412m a year to the market. That said, Pocket DAO may vote to curtail new POKT releases in the near future. Moreover, despite these staggering numbers, Pocket Network can still handle only a fraction of the traffic of its concentrated competitors, with Infura alone serving more than 2.4 billion Ethereum relayings a day in 2020.

Due to the huge potential market and the success of harmonizing with the integration of other protocols with pockets, we can see an increasing number of protocols rerrouting and decentralizing with pockets of transportation networks that raise the dependency of prevention or response issues with centralized blockchain infrastructure. Whether this decentralized infrastructure can support a Web3 economy with billions of DApp users will depend on the resilience and ideal anti-vulnerability of node and network technologies.

The emerging Web3 economy

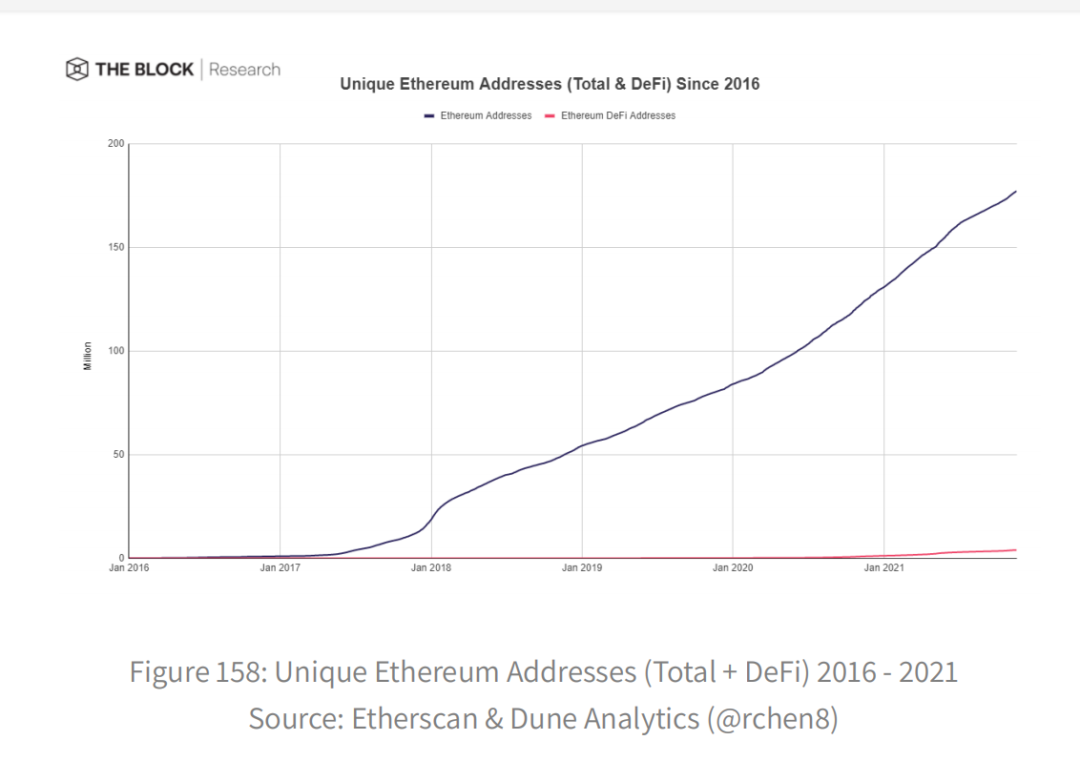

To conclude this chapter, we'll look at some data on the emerging Web3 economy to get a sense of where we are and where we're headed. While there is no single metric to track overall Web3 development, we can look at several proxy metrics that track different aspects of Web3, from DeFi to NFT to adoption of Web3 front-end applications such as wallets. Below, we plot all unique Ethereum addresses and unique Ethereum addresses that interact with the DeFi protocol from January 1, 2016 to November 17, 2021.

The total number of unique addresses on Ethereum has steadily increased since the beginning of 2018. Ethereum's unique addresses have grown by an average of about 52% a year since the start of 2019. Ethereum addresses interacting with the DeFi protocol have also exploded since 2019, growing by about 700% yoy, but slowing slightly from around 875% yoY from 2019 to 2020 to around 500% yoY from 2020 to 2021. Currently, only 2% of Ethereum addresses interact with DeFi, but that's still more than double the 0.9% at the beginning of 2021. DeFi still seems to have a lot of upside potential.

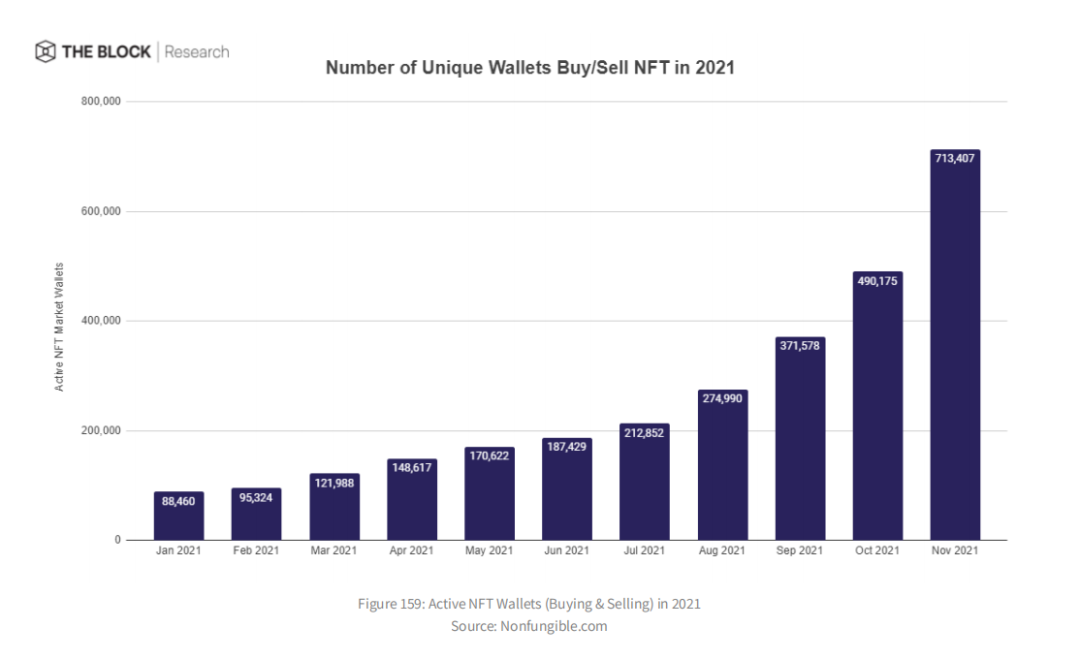

Another agent that tracks the NFT transaction submarket in the Web3 economy is the total number of unique wallets that buy or sell non-functional transactions. There are varying degrees of significant month-on-month increases - for example, 8% in January-February, 28% in February-March, 10% in May-June, and 35% in August-September. Overall, the number of active wallets in the NFT market has grown 600% this year alone.

We can also use the number of monthly active MetaMask users as a proxy for Web3 economic activity. Below, we've plotted the monthly active user accounts provided by Consensys from the beginning of THE first quarter of 2020 to the end of the third quarter of 2021.

In July 2020, Consensys reported that MetaMask had 550,000 monthly active users. By August 2021, there were more than 10 million, an increase of 1,800% in about a year. A brief look at the Web3 economy from these perspectives really helps to understand the hot topics behind Web3 and the explosion of vc interest in supporting projects in these areas, from DeFi to NFT to gaming. Given the upward trend over quite a long period of time, we can begin to have some confidence that Web3 is indeed beginning to consolidate itself outside of the Web2 architecture.

These new user experiences are enabled by decentralized, secure, immutable databases such as blockchains;

New ways to simplify access to data structures using token incentives, economic games, and cryptographic proofs;

And a series of new tools for Web3 prototyping and development.

Chapter 7: NFTs and Blockchain-based games: Overview of 2021, Vision for 2022 & NBSP;

Data-driven overview of NFT and blockchain-based gaming landscape, growth metrics, theme highlights, and more.

The profile

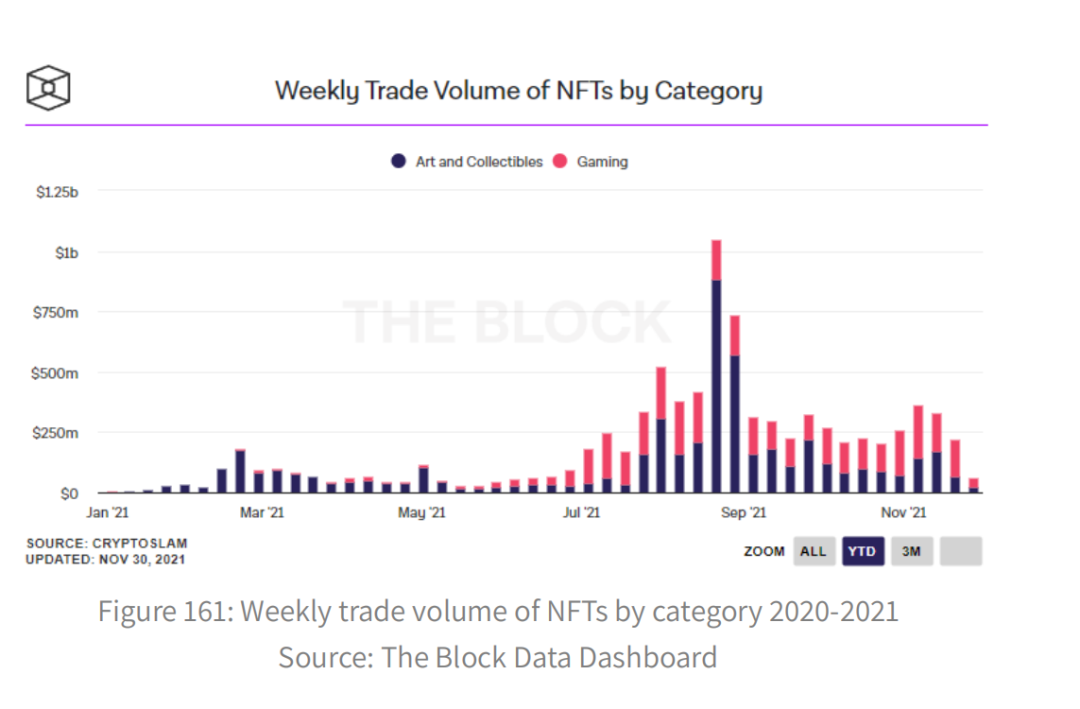

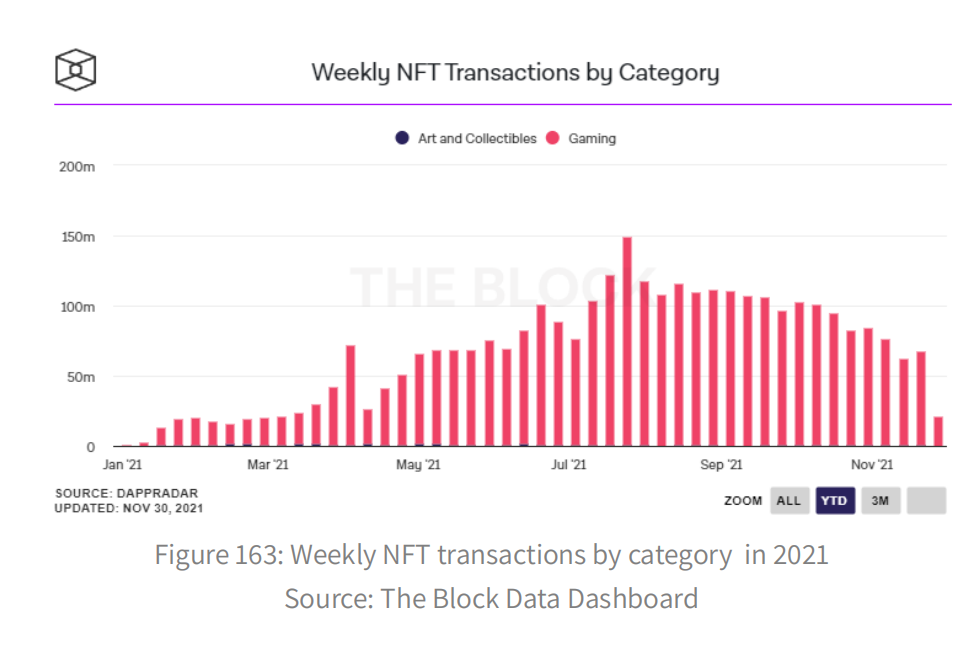

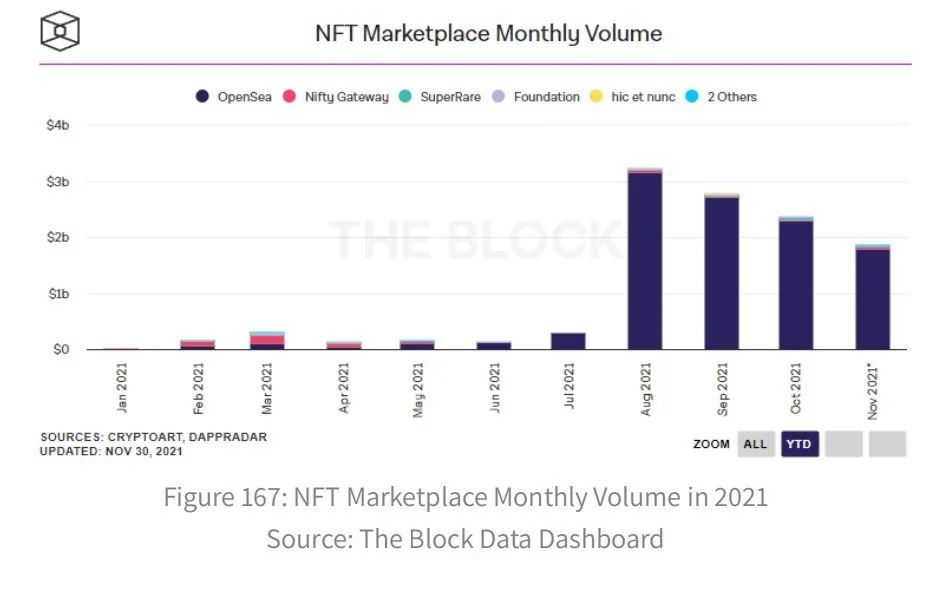

-- $8.8 billion in non-functional transactions, 59% for art and collectibles and 41% for games;

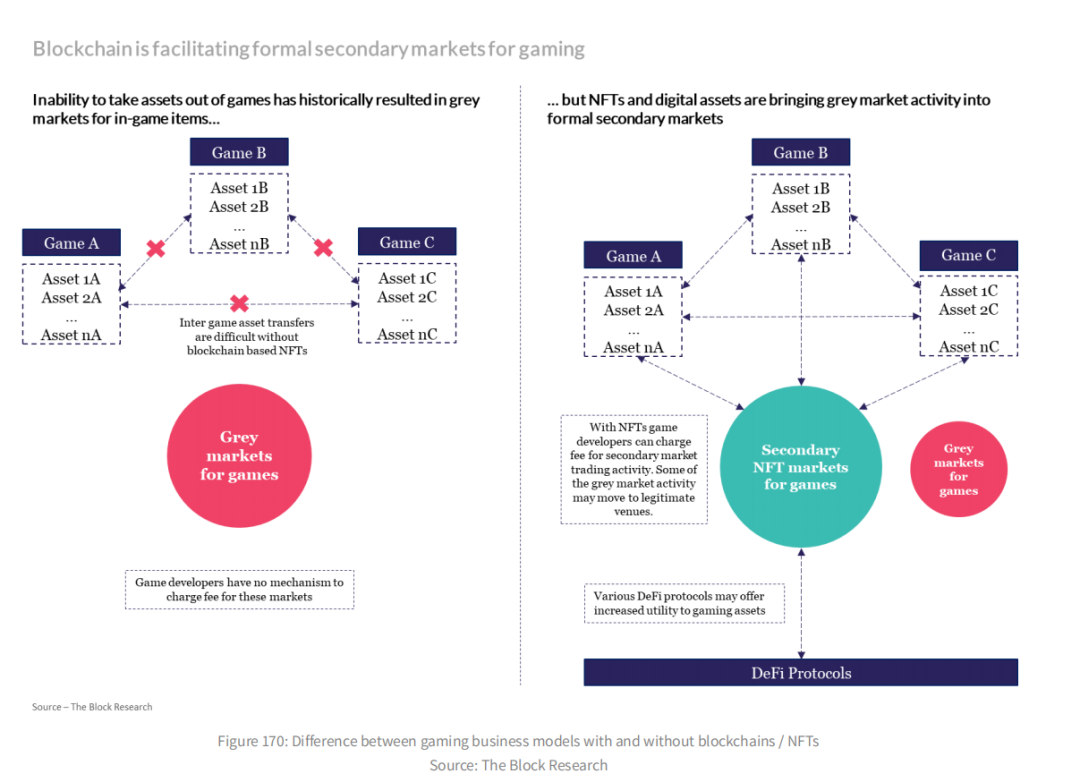

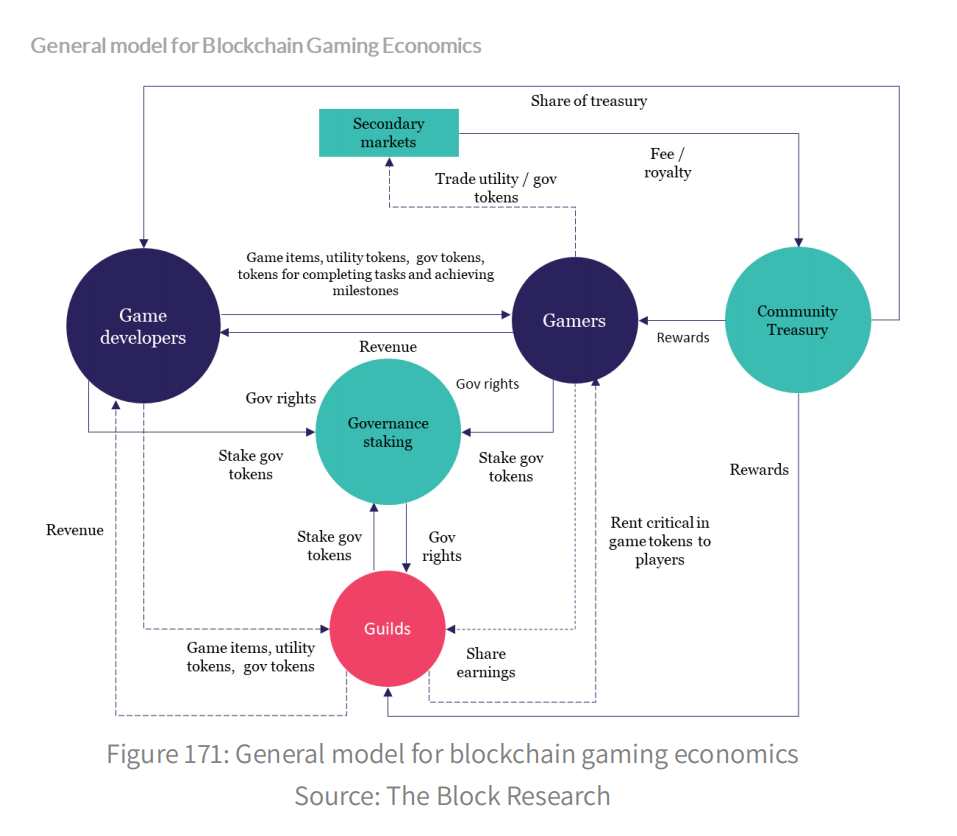

- Blockchain-based games have found a product market suitable for the new business model, where game developers can oversee the entire lifecycle of in-game assets while earning fees from secondary market transactions and introducing users to the interoperability of their assets and potential in-game revenue;

- High gas costs have forced non-deliverable transaction activity from Ethereum to other tier, side chain and tier 2 solutions.