Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

MakerDAO protocol engineer talks about Maker's past, present and future

Original title: "MakerDAO protocol engineer tells Maker's past, present and future"

Original author: Sam MacPherson, MakerDAO Protocol Engineer

Original Compilation: The Way of DeFi

I think the mental model of many people in DeFi thinks that Maker is "A protocol for issuing DAI loans against various ERC20 tokens". This was true before the explosion of DeFi in the summer of 2020, but things have changed a lot since then. I wrote this post to describe the evolution of thinking at Maker DAO from then to now, and where I think we are headed in the future.

March 2020 - Black Thursday

The new crown pandemic was just beginning, and we all remember the events of Black Thursday, when the cryptocurrency market fell by 50%. The Maker protocol, which was only 4 months old at the time, came close to collapsing due to unprecedented pressure and a neglect of how the auction system worked. But we made it through in the end... just barely.

While most of the attention has been on the failed liquidation and recapitalization of the MKR mint, there were a few more things happening on the day delicate matter. On this day, the demand to hold DAI exceeds the demand for ETH leverage.

Until that day, Maker had the opposite problem. DAI has been trading below the peg. You might be wondering what's wrong with DAI being worth more than $1. This is a good question. Strangely, this is harder to deal with than a stablecoin that trades for less than $1.

It's all about the balance of supply and demand. Excess supply of DAI drives down its price below $1 as people mint and sell DAI for leverage or other use cases.

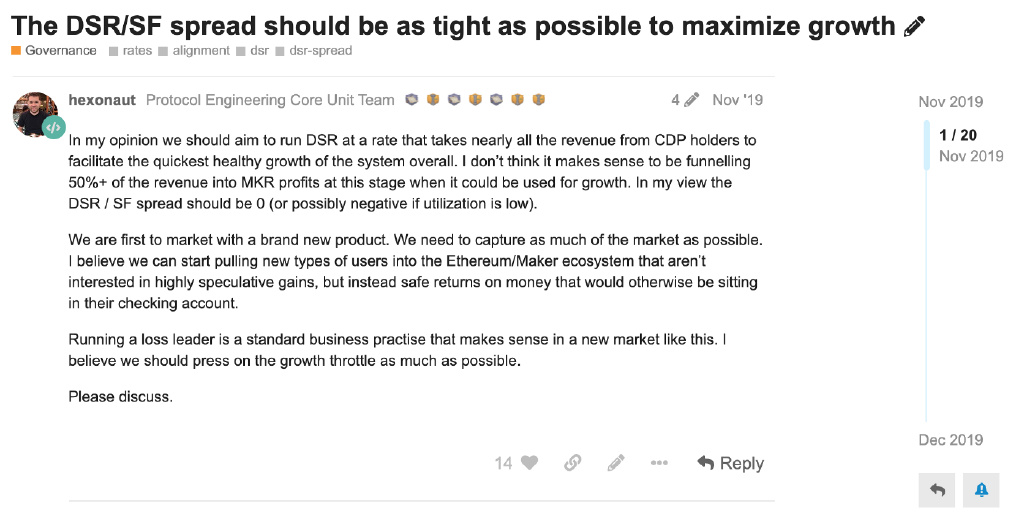

Maker has two powerful tools to combat this: a stability fee and the Dai Savings Rate (DSR). The former restrains supply growth by taking more loans. This will cause some people to reassess whether they want to use leverage at the new higher interest rate, and possibly even repay some previously acquired loans. This is the big stick with which to beat the market.

In comparison, DSR works better. It incentivizes demand for more DAI by providing a risk-free rate for holding only DAI. This is in addition to any lending rates offered by Compound or Aave.

Things have changed drastically after Black Thursday and we have too many people wanting to hold DAI. Numbers that exceed the leverage you want to cast. DAI price increased by 6 cents. At the time Maker did not have any leverage to reduce DAI demand (negative interest rates) or increase supply (non-crypto collateral).

USDC to the rescue

As an emergency response, Maker holders chose to add USDC to restore the peg price, and finally succeeded! But there was an ideological price paid. It is our first custodial, blacklistable centralized asset.

It's clear to me that DAI wouldn't exist today if we didn't take the steps we did. Some people want to take the negative interest rate approach, but my personal opinion is that it would be disastrous for people's trust in DAI.

In a startup, you want to focus on aggressive growth at almost any cost. It's survival of the fittest. Single-collateral Dai has only one lever to control supply, but multi-collateral Dai introduces DSR, which works by increasing DAI demand rather than trying to punish borrowers. Using DSR was something I personally advocated when Maker launched.

Similarly, by using USDC instead of negative interest rates, we can continue to grow the protocol instead of penalizing our user base. This is why I am in favor of increasing supply by adding USDC rather than introducing a negative interest rate mechanism.

My mental model at the time was that the market would eventually be bullish again and we would return to positive rates without relying on centralized assets . But then the DeFi summer boom ensues.

Compound came up with the neat idea of minting a speculative governance token and distributing it to liquidity providers . This drives demand for all assets in Compound — including DAI. The yield farming model was born. We have no choice but to add more USDC, otherwise it may trigger the risk of the peg rising again. We solved this again, but got stuck with a large amount of USDC backed DAI, which was considered undesirable by some.

With the launch of the Pegged Stability Module (PSM) at the end of the year, the addition of USDC continues to effectively peg us to USDC and USD . Relief appears to be on the horizon as the market turns bullish again.

2021: Year of the Farmer

In the first half of 2021, it is increasingly clear that, in addition to ETH and WBTC, the There is almost no demand for stablecoin loans on the scale of 100 million US dollars. This is a shift in belief from the previous belief that small-cap ERC20s (LINK, UNI, MATIC, etc.) will help supply DAI in a meaningful way. In many cases, the cost of running an oracle is higher than the income generated by these collaterals.

Another influence also emerged. Yield farming models are exploding in popularity, and nearly every protocol is fighting for stablecoins. The release of tokens for yield farming is usually a constant rate, so when the market goes up, it increases the USD value of those tokens, which increases the APY of the liquidity pool. This in turn will increase the demand for DAI. During market downturns, people choose DAI as a safe-haven asset, so the demand also rises. Aside from temporary reversals, the trend in DAI supply is mostly up — a good question, to be fair.

It became very clear this year (if it wasn't already) that if we wanted a A centralized stablecoin, which needs to include a wide range of Real World Assets (RWA) to back it. The first is USDC, but it certainly won't be the last. In 2021, we added two stablecoins, USDP (rebranded from PAX USD) and GUSD, to help diversify counterparty risk. Some may think this is just a more stable coin, but it is an important part of the emergent decentralization through a centralized component.

A fundamental point I want to make is that you cannot scale stablecoins by being purely backed by crypto-native assets. There is simply no way to do this. All stablecoins have to be overcollateralized or at risk of crashing, and there simply isn't enough value in purely crypto-native assets to do that. There is no alternative to utilizing real-world assets, and no amount of fancy algorithms can get around this fact.

Therefore, we must tokenize more assets from the real world - especially in different jurisdictions . This is how we scale DeFi. The alternative is that cryptocurrencies are still a niche gambling product that has faded into obscurity.

Direct Lending

When MCD launched in November 2019, DeFi was pretty much all about Maker, Compound and Uniswap. However, a few months later, Aave V2 was deployed, providing end users with possibly one of the best retail lending experiences. Cross-collateralization, tons of assets, multiple stablecoin options make Aave a killer lending app.

This is a pivot point for me. At its core, Maker is not a lending tool. Maker's main product is the DAI stablecoin. Borrowing is just our way of controlling the peg. Instead of competing with products like Aave and Compound, give them privileged access to mint DAI on demand. This will allow Maker to reach a portion of Aave's user base. In exchange, Aave gets stable interest rates. It's a win-win.

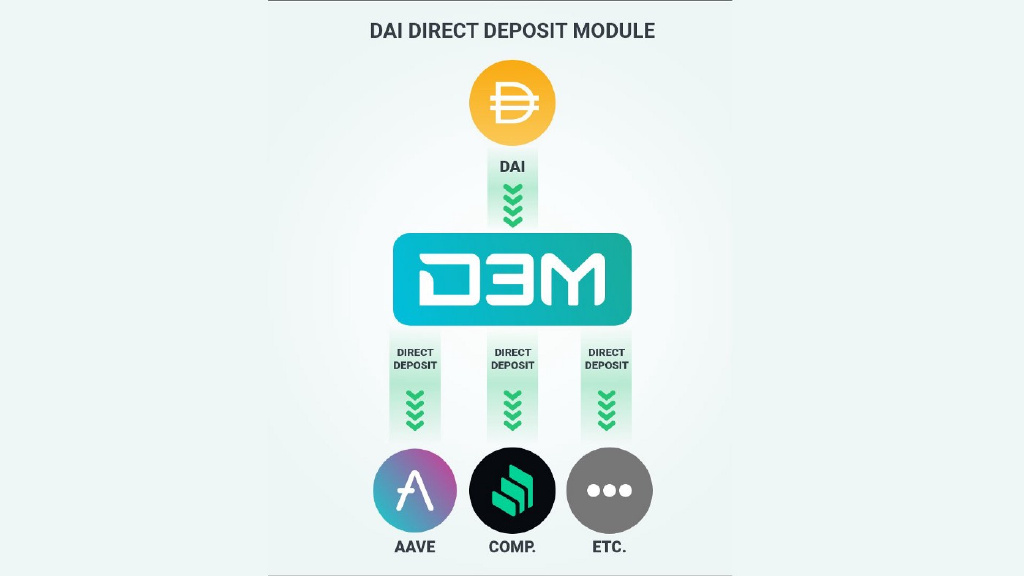

Thus, the Dai Direct Deposit Module (D3M) was born. Rather than competing on the retail side, Maker can delegate minting rights to protocols that specialize in specific market segments. The low hanging fruit is a crypto lending market, but there's no reason it couldn't be attached to Maple or other real-world lending markets.

This is not to say that we should abandon direct lending to users entirely, but just stick to the major cryptoassets (ETH, BTC and staked ETH) makes sense.

The future of Maker

In my opinion, the future of Maker is delegation. MakerDAO can focus on a high level of due diligence rather than messing with personal assets. Evaluate whether to extend DAI minting power to the entire protocol.

This is similar to the relationship between a commercial bank and a central bank. Central banks provide liquidity to commercial banks, which in turn can provide highly specialized services to their clients. Maker's job is not to be the best at everything. We can use DeFi Lego bricks to build something greater than the sum of its parts.

I am optimistic that protocols will emerge that fully handle extending credit instruments to the real world. We've seen some small-scale experiments so far, but this will take orders of magnitude to scale the ecosystem. Maker will be ready when these protocols emerge, and there is a gold mine waiting for whoever cracks the nut first.

It is now clear that we are entering a multi-chain world. As Ethereum transitions to a pure settlement layer, we are working on scaling Maker to every reputable L2 and sidechain. This, combined with the Maker Wormhole network, will make DAI one of the most liquid cross-chain assets available.

In the long run, the master instance of MCD will become rigid and innovation will be pushed to the fringes in a decentralized, fully independent team Build new innovative products. The core protocol will protect itself by providing debt ceiling allowances to these teams. Highly diversified risk is the key to survival here. Core protocol updates will be rare and locked in for months or years. A product that people can actually depend on.

Eventually DAI will be de-pegged from the USD as it becomes competitive as one of the global reserve currencies. This is the end state I see for Maker — a rock-solid, trusted, neutral foundation on which the world can transact. Let's start building.

Original Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia