Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Analyze three models of NFT mortgage lending: point - to - point, capital pool and centralization

Simple Thoughts on NFT Mortgage Lending

Original article by Jiawei (Twitter: Elegy4TheArctic)

primers

It's been more than 10 months since the summer of DeFi 2020. Aave, the white horse of DeFi lending, has slipped to 61st in market cap, while Compound has fallen, somewhat surprisingly, outside the top 100.)

说回抵押借贷,对于 NFT 而言,抵押显然需要承担一定的流动性成本:面对 Token 上涨,无法出售并获利;面对 Token 下跌,只能被动持有。

For institutions or core players of long-holding NFT projects (such as CryptoPunks and BAYC, etc.), there may be no intention to sell, so when assets need to be liquidated, mortgage lending is an option worth considering. The price of head NFT is also relatively stable.

Furthermore, for speculative purposes, there may be frequent trading of NFTS in the hands of retail investors, and the overall value of NFTS is not high, making it relatively unsuitable for collateral.

Therefore, in the short term, NFT lending will be a niche racetrack, mainly for head/blue chip NFT holders.

Three types of projects

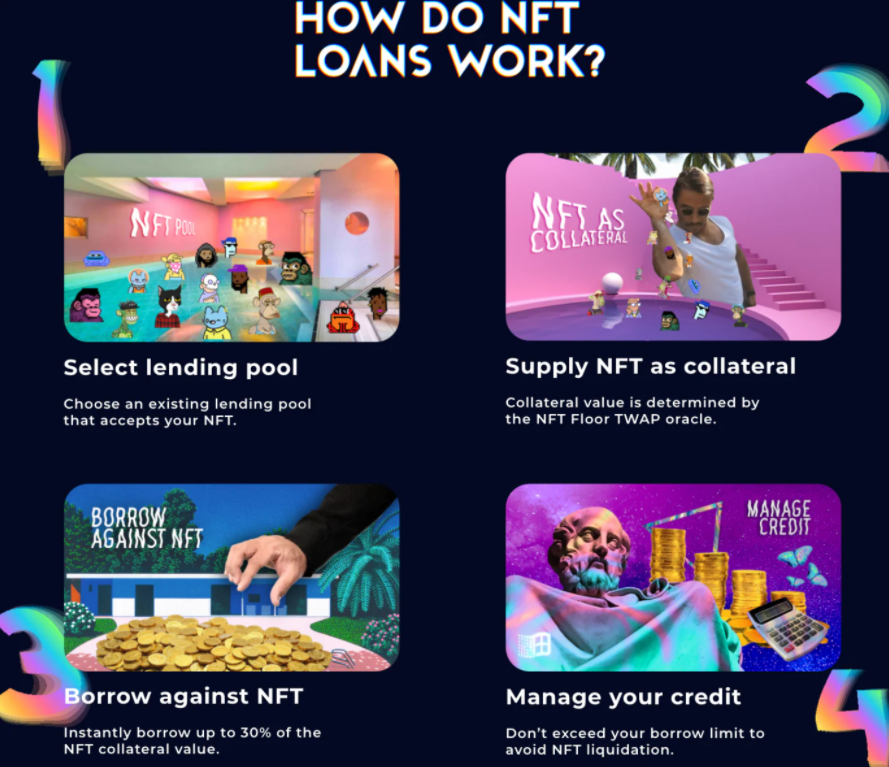

Point-to-point mode

Ethlend, Aave's predecessor, used the peer-to-peer model in DeFi lending.

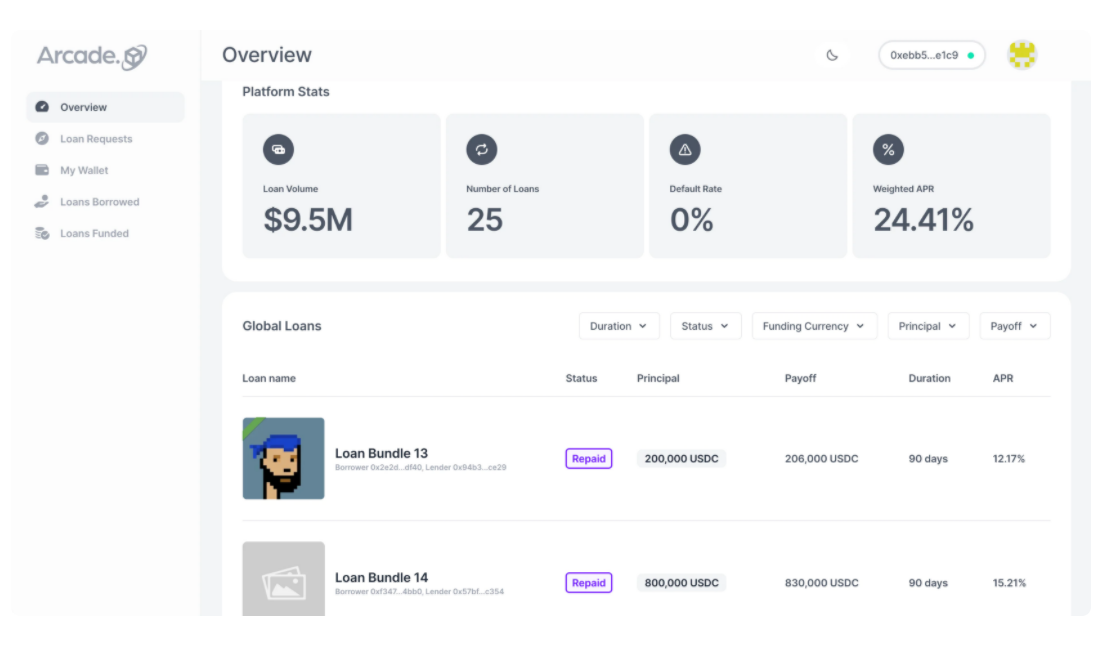

In a similar vein, Arcade's AssetWrapper contract backs bundled mortgage assets ERC721, ERC1155 and ERC20, which in turn generates wNFT. The borrower sets the loan amount, repayment amount, currency and time, and then waits for the lender to match the order. Arcade will add installment payment mode in future versions.

It should be noted that Arcade does not set up automatic liquidation, and in the event of default, the borrower can still repay the loan before the lender claims collateral.

For a peer-to-peer platform, the timely response of lending needs is directly related to the user experience of the platform. The average waiting time for a match is not yet available in Arcade's platform data. According to team members, BAYC and CryptoPunks responded to loan requests for floor prices almost instantaneously.

In addition, the difference between NFT and FT is that the same series of NFT are different, so it is difficult for the lender to evaluate the NFT with high rarity, or the lenders and borrowers have different valuations on the collateral, which increases the uncertainty of lending.

Arcade's platform currently has a total loan of $9.5 million, supporting 49 NFT collections. In late December, Arcade raised $15 million in Series A funding, led by Pantera Capital.

Capital pool model

The second type is the fund pool model similar to Aave and Compound, such as Drops DAO.

In this model, the loan has no maturity date and the interest rate is calculated based on the utilization of the asset. NFT's real-time prices are quoted using a predictor.

Dyo Hu elaborates on the advantages and disadvantages of the peer-to-peer model and the capital pool model in this article.

For highly rare NFTS, the value in the capital pool is actually diluted, making the loan-to-value ratio of this portion of NFTS uneconomical.

Overall, the pool model is complex, with the possibility of malicious price manipulation and serial liquidation. In the case of general liquidity of NFT market, there is a high systemic risk. In the early stages of decentralized NFT lending, the peer-to-peer model was more stable and reliable.

Centralized model

Late last year, Nexo , a digital asset financial services firm; In cooperation with Three Arrows, we launched a centralized NFT lending business. Kraken, an exchange, plans to do the same.

Nexo provides the equivalent of an OTC service, requiring the completion of a simple KYC application form. Currently, only BAYC and CryptoPunks are supported as collateral. The NFT value of the collateral must exceed $500,000. The annual lending rate is about 15%, and the loan-to-value ratio is between 10% and 20%. That is, an NFT worth $500,000 can get a loan of $50,000-100,000.

The centralized NFT lending model is suitable for institutions, but may not seem so native to Crypto OG.

Closing Thoughts

If you look at the real art market, global art sales in 2020 fell 22% from the previous year due to the pandemic, and are still over $50 billion -- looking at the numbers alone, art collateral seems to have a good market.

However, the appraisal of works of art (including antiques here) itself is controversial and lacks authoritative guarantee, making valuation difficult; And because of the lack of liquidity, it is uncertain whether the collateral can be sold even after liquidation. To compensate for this risk exposure, traditional pawnshops underprice heavily, often offering very small loan-to-value ratios.

Going back to NFT, compared with traditional works of art, NFT authenticity can only be verified by checking the contract address; Valuation with the same series of NFT floor prices for reference; Online trading also makes it relatively easy to cash in. Technically and operationally, NFT lending faces fewer problems.

Recently Azuki quickly became the 8th most traded OpenSea NFT, and there may be more blue chips like this in the future. Head NFT (CryptoPunks and BAYC), blue chips (Doodles and Azuki) and Sandbox and Decentraland will be the first to become the main target of NFT lending in the future.

The original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia