Forum

Forum

Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Viewpoint: From the perspective of Avalanche, look at the competition among second-tier public chains

Original title: "Looking at the competition among second-tier public chains from the perspective of Avalanche"

Original author: Maco, W3.Hitchhiker; revision: Evelyn, W3.Hitchhiker

I. Basic information

1. Avalanche architecture and technology

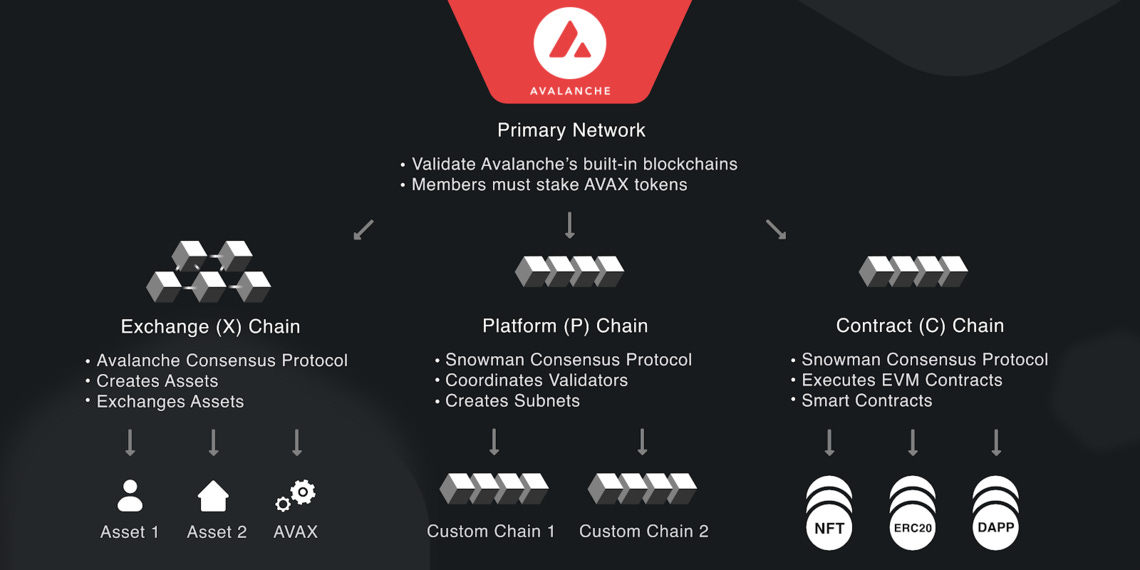

Avalanche is characterized by a three-chain architecture, namely the transaction chain (X-Chain, DAG), the contract chain (C-Chain), and the platform chain (P-Chain). The figure below gives a clearer division of labor.

Avalanche adopts horizontal expansion, similar to Cosmos and Polkadot. Here is a simple comparison:

- Dot Network validators maintain a unified global state, and parallel chains have shared security (highest security); the worst flexibility/autonomy, and future scalability and performance will be subject to the relay chain; the best inter-chain interoperability; - The validators of the Avax network are completely independent, and a subnet composed of a group of verification nodes does not share state but "partially" shares security (medium security, subnets can operate multiple chains, while enjoying the fee rewards of multiple networks and bearing the risk of penalties); medium flexibility/autonomy, good scalability; theoretically good interoperability within the subnet - The validators of the Cosmos network are completely independent, non-shared state and security (lowest security, with subsequent improvements), and the security levels of hubs/zones vary; the best flexibility/autonomy, high zone freedom, and unlimited scalability; good inter-chain interoperability;

Advantages:

New BFT Consensus: low latency and high scalability. It adopts small sample repeated sampling and DAG information transmission architecture, which eliminates the "quadratic message transmission complexity" between nodes (the amount of message transmission is the quadratic of the nodes), so the network consensus/verification efficiency will not become low due to the increase in the number of nodes. In theory, it supports more nodes than PBFT (number of nodes Avax: 1283, Atom: 175, Dot: 297)

Subnet: Brings horizontal scalability, called "overlapping verification network", requiring all subnets to be validators of the main network - staking 2000 Avax, which not only strengthens the security of the entire network, but also empowers Avax Token. Therefore, the economic model and theoretical network security are stronger than Cosmos and lower than Dot; but the subnet entry threshold is relatively low

Compared with Cosmos and Dot with similar architectures, Avax has C With the market-tested model of the blockchain, projects can create a sovereign chain more worry-free and customized

Disadvantages:

Inter-subnet interactivity: Interactions within a subnet are instant and protected by shared security, but interactions between subnets are currently only possible through bridges. Weaker than Cosmos' IBC and Dot's XCM.

The adoption rate of subnets is not as widespread as Cosmos and Dot, and is single (only GameFi). Whether the innovative consensus mechanism can withstand pressure in the formal market environment.

Avax has not experienced the test of a bear market

2. Key team members

Founder & CEO: Emin Gn Sirer, professor at Cornell University, founded IC3, a blockchain organization funded by the National Science Foundation of the United States, and developed the first POW currency system karma 7 years earlier than Bitcoin.

Co-founder & COO & CPO: Kevin Sekniqi, PhD in Computer Science from Cornell University

Co-founder & CPO: Ted Yin, PhD from Cornell University, inventor of the HotStuff consensus adopted by Libra.

President: John Wu, Cornell University/Harvard Business School, professional investor and manager, formerly worked at Tiger Fund

3. Financing

According to Crunchbase information, Ava Labs has raised 7 rounds of financing, with a total financing amount of 290M.

Investors mainly include: a16z, Polychain, ThreeArrows, Bitmain, Galaxy Digital, Dragonfly Capital, NGC Ventures, Initialized Capital

TL;DR:

The team has strong technical capabilities, the investors are not bad, and the expansion direction is also the mainstream. It has won and lost with the mainstream multi-chain, and has real use cases and customized features.

2. Public chain performance

1. Throughput

In order to form differentiated competition with ETH, the TPS values given by the official public chains are quite scary, thousands or tens of thousands, but after actual measurement and experience, we feel that there are still some differences in general, but not as big as the official propaganda.

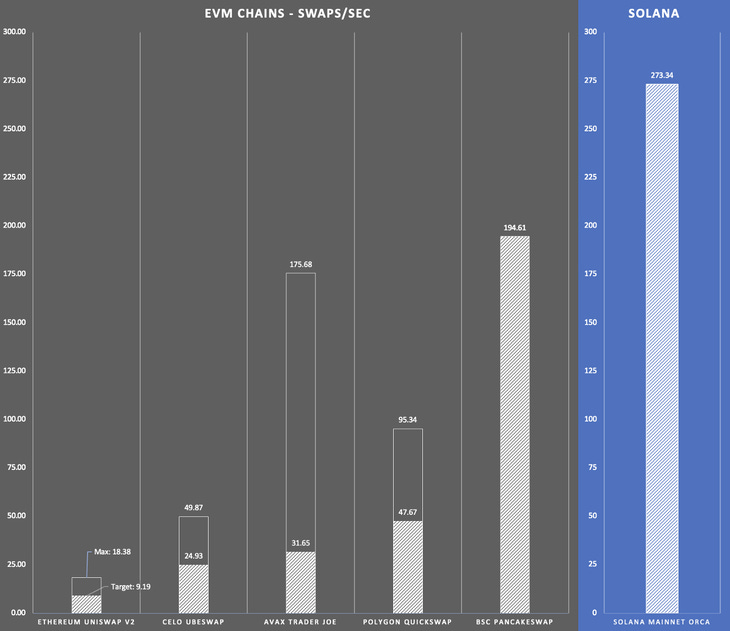

The most reliable way to evaluate the performance of public chains is Dragonfly's research article "The AMM test: A no BS look at L1 performance". The following TPS results are calculated based on the gas consumed by swap transactions (contract interactions) (this is also a relatively fair theoretical calculation method we recognize, because the transaction components of each chain are different, and the difference will be very large if only ordinary transactions are calculated).

Since some chains have the concepts of gas target and gas limit, the physical column represents Target, which means that the public chain operates well within this TPS range and the user experience is also good. Exceeding it will lead to poor experience/gas fee surge (as shown in Figure 2). We can see that the highest TPS cap of each public chain is SOL's 273, the highest BSC among EVM compatible chains is 194, and ETH is 18. Although there is a 15X gap between the highest and the lowest, it is not as big as the hundreds or thousands officially advertised by each chain.

(Figure 1)

(Figure 1) 2)

The above calculation is similar to the performance estimation of BSC made by W3 last year, but we use the gas limit and actual transaction in the actual operating environment to make the estimation. This logic will better simulate the real environment, but this method is only applicable to EVM chains with relatively stable block production and actual ecological usage reaching/approaching the chain limit.

We use the following formula to calculate the TPS limit that the chain can reach in the actual operating environment

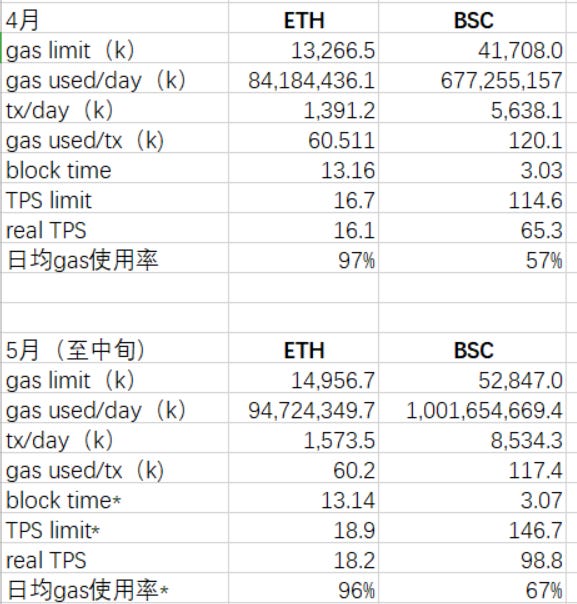

Get the corresponding data of each chain (gas limit, gas The average of the TPS of ETH and BSC is 18.9 and 146.7 respectively.

In the processing of the gas used/tx data, we can see that we take the average value that actually occurs on the chain, rather than simply using the consumption data of contract interaction or simple transfer (21k gas):

According to the above table, we can see that ETH is in a "full" state, and the gas usage rate is above 95% for a long time. Therefore, the actual performance is around 18.

As the "peak of EVM", the BSC ecosystem experienced a big explosion in the second quarter of last year, with frequent on-chain activities, and also tested the performance of the chain in a formal environment. Although the official has been continuously increasing the gas limit as a temporary performance improvement plan since April, the TPS has only reached about 146 at most. However, the user experience at that time was very poor - congestion and frequent block synchronization events. Therefore, in actual experience, the TPS that can run well is about 100, far from 194. (From the subsequent data in November, TPS hit a new high (219), which may be due to Binance's subsequent equipment upgrades, but there is limited room for improvement under the same architecture, so Binance has also begun to adopt the BNB chain multi-chain solution)

The SOL chain is special and has no concept of gas limit. Therefore, we have not found a corresponding calculation method for the time being. We can only observe the upper limit it may reach through historical data on the browser.

Excluding the influence of special events such as ID0 and NFT mint, the TPS of SOL can be stabilized at around 3000 under normal circumstances. However, we can see through the browser that on average, 76% of the 3000 TPS are messages (votes) for reaching consensus on the chain, which cannot be counted as real user transactions and should be excluded. In the remaining TPS, it is observed that simple transactions interacting with serum account for a large proportion (due to the special mechanism of the SOL chain, most protocols will interact with serum). Therefore, we believe that this cannot be counted as real user consumption and should be excluded. The remaining real user transactions are around 10%, so the real TPS is around 300. However, this method does not measure the limit value of SOL, so the actual TPS should be 300 +. As for the frequent downtime of the SOL chain leading to poor user experience, that is another matter and is not within the scope of this discussion.

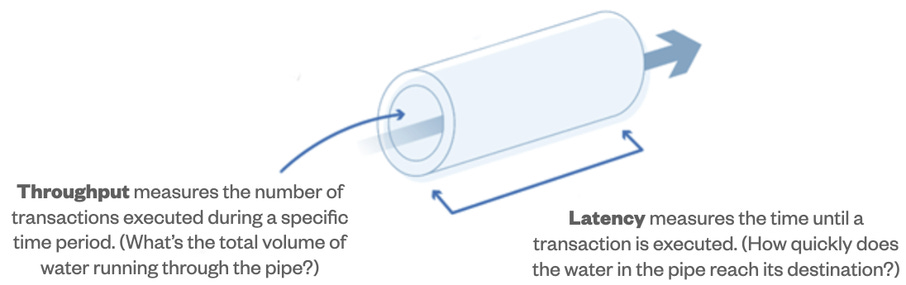

2. Latency id="§2-latency">When evaluating the performance of a public chain, most people only evaluate TPS throughput, because it represents how many transactions can be accommodated within a certain period of time (how much water can pass through the pipe). But we should also look at another dimension - latency, that is, how long it takes for these transactions to be executed (how long it takes for the water to pass through the pipe). This indicator is even more important to the user experience of a single user than TPS.

Latency This dimension is difficult to quantify. We mainly observe the transaction confirmation time. That is, the shorter the confirmation time, the better the user experience.

We first exclude the special case of high concurrency, because all chains will have high delays when facing high concurrency. Here, only the normal situation is considered. From the perspective of user subjective experience (random interviews and perception), SOL had obvious transaction confirmation delays and a particularly high transaction failure rate (average 15%-20%) during the outbreak last year. Subsequently, although the official had emergency flow control solutions, the effect was general; Polygon and BSC also had very high transaction delays after the outbreak, and they have not been resolved.

According to incomplete feedback and my own experience, each chain has the problem of transaction confirmation delay during peak periods, and it is not easy to solve. In comparison, Avax has a better experience-although the transaction fee is high during peak periods, there is no large-scale congestion delay (under normal conditions). In addition to the advantages in mechanism, it is also closely related to network utilization.

3. Events

For performance, all chains have had problems, and they are currently being actively improved

Solana: Previously, requests were limited during peak hours. With the latest v1.1 update, TPS has returned to its previous high, and the user experience has improved; data flow control technology will be introduced in the future to improve the gas mode.

Avalanche: The high-speed influx of large traffic may expose some performance issues. Avalanche once triggered a cross-chain function error due to the high load of DEX Pangolin, which caused a certain short-term panic in the community.

BSC / Polygon: In the second quarter of last year, due to the outbreak of on-chain activities, congestion occurred one after another, and gas fees soared.

TL;DR:

Currently, the single-chain TPS ceiling is SOL, and the performance ceiling of all EVM chains is basically BSC, but the gap is far less than the official propaganda, and the high TPS chains have more or less had problems (SOL downtime, BSC node asynchrony).

Each chain wants to reach the theoretical performance ceiling, and the cost is not small - the gas fee surge. SOL will not be affected by this because there is no gas limit concept.

Each chain is powerless in the face of instantaneous high concurrency, and the current various solutions do not support continuous high-frequency activities on the chain, and the user experience needs to be improved.

3. Ecosystem support and incentives

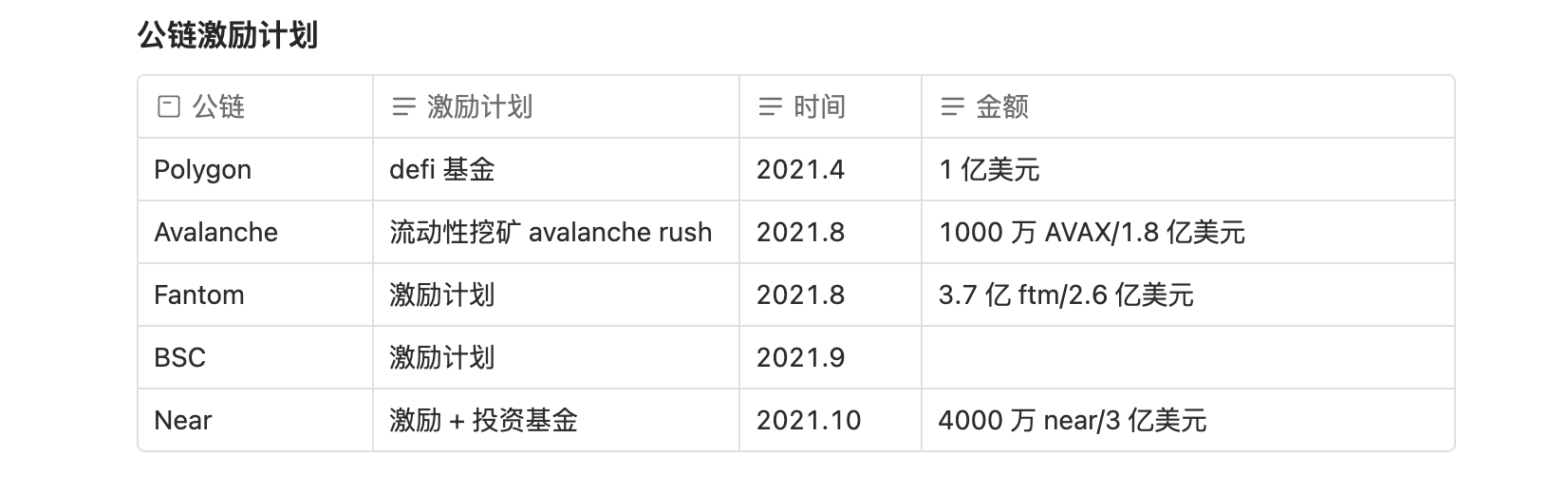

In 2021, in order to seize TVL, major public chains have launched a number of incentive plans. Here is a simple list:

The incentives of Avalanche Rush increased the TVL on the chain by nearly ten times in just ten days, from 260 million to 2.3 billion US dollars, and formed a positive cycle. Combined with the rise in the price of Avax, the public chain TVL has been soaring all the way, reaching a maximum of 13 billion US dollars. To date, although TVL has plummeted with the market, from the perspective of currency standard, there is no sign of outflow of assets on the Avax chain, indicating that the public chain has accumulated some loyal assets/users.

Other incentives

In November 2021, the Avalanche Foundation launched Blizzard, an incentive plan of more than 220 million US dollars. The incentive plan will focus on DeFi, enterprise applications, NFT and cultural product developers. The funds of Blizzard Fund mainly come from the Avalanche Foundation, Ava Labs, Polychain Capital, Three Arrows Capital, Dragonfly Capital, etc.

From December 2021 to early March 2022, the Avalanche Foundation and the Web3.0 development platform Moralis jointly conducted their largest hackathon, aiming to accelerate the development of DApps, Web3 applications and DeFi projects within the ecosystem.

In March 2022, the Avalanche Foundation announced the launch of the "Avalanche Multiverse" incentive subnet program, providing a total of 4 million AVAX Tokens worth approximately US$290 million. At the same time, Ava Labs, one of Avalanche's core developers, also provided assistance and support for subnet development.

It can be seen that the direction of each incentive is still very clear: liquidity incentive - hackathon - subnet incentive

TL;DR:

Avalanche's early incentives are similar to Polygon, directly targeting users' liquidity mining incentives; in the later period, Avax's incentives are placed on developers and ecological cooperation, and it is superior to its competitors in terms of funding and comprehensive coverage

Due to the diversion of CEX, BSC does not need to incentivize users, but focuses on incentivizing project parties; Fantom also adopts a similar solution

Fourth, Funds and Users

1. Bridge

Part of the funding for the public chain explosion comes from the support of CEX, and the other is the bridge. Therefore, we can take a peek at the eve of the public chain explosion through the amount of funds in each cross-chain bridge. From the figure, we can clearly see the obvious inflow of funds from Polygon (April), Avalanche (August), Near (August), and Fantom (October), which led to the subsequent explosion of various chain projects.

Avalanche launched the two-way cross-chain bridge (AEB) and Avalanche Bridge (AB) with Ethereum in February last year. Its characteristics are low cost and fast speed (1-5 USD. The transaction fee of any cross-chain mechanism is mainly on Ethereum. However, in the AB mechanism, the transactions on Ethereum are ordinary transfer transactions, which do not require the call of contract transactions, so the transaction fee must be relatively low)

2. TVL

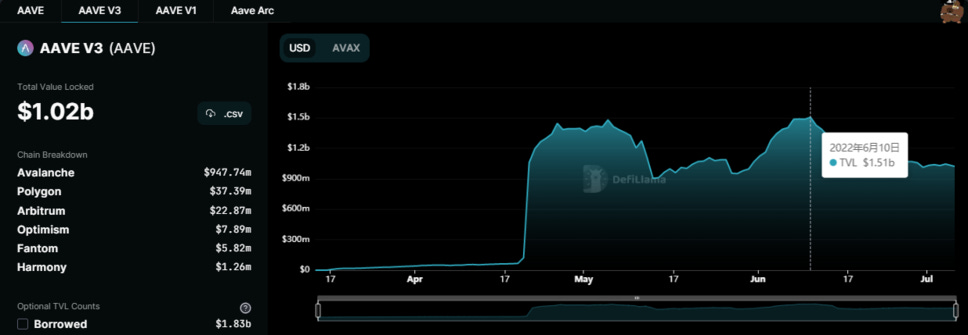

TVL has dropped by more than 80% from its peak, and its performance is at the same level as SOL and BSC, second only to ETH, but better than other chains. From the perspective of currency standard, there is no obvious outflow of funds in the entire Avax chain, but it is on an upward trend, which is significantly better than its competitors (mainly from the stable contribution of Aave), and Near also shows a similar trend.

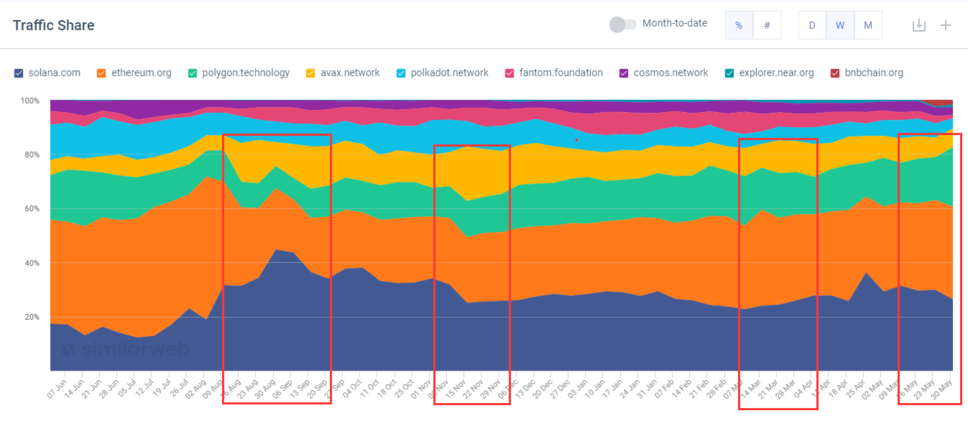

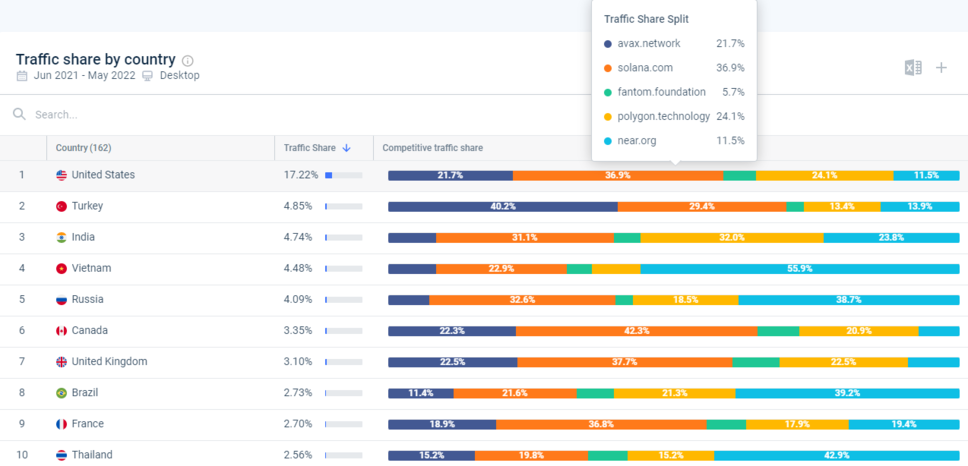

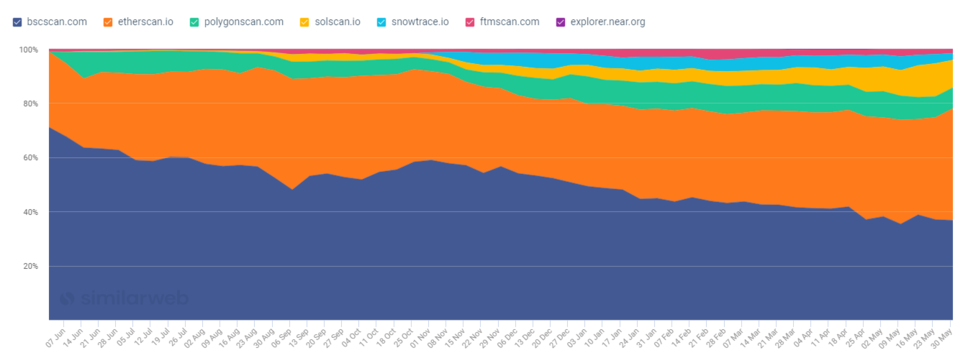

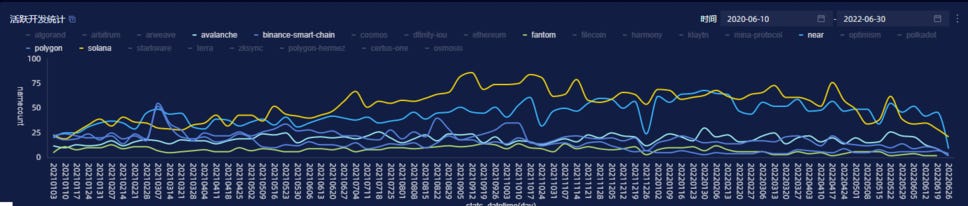

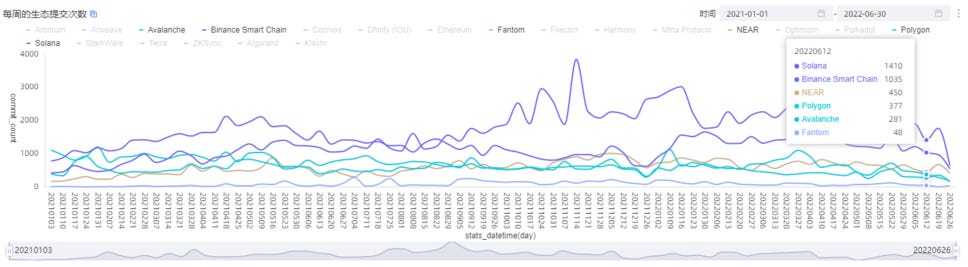

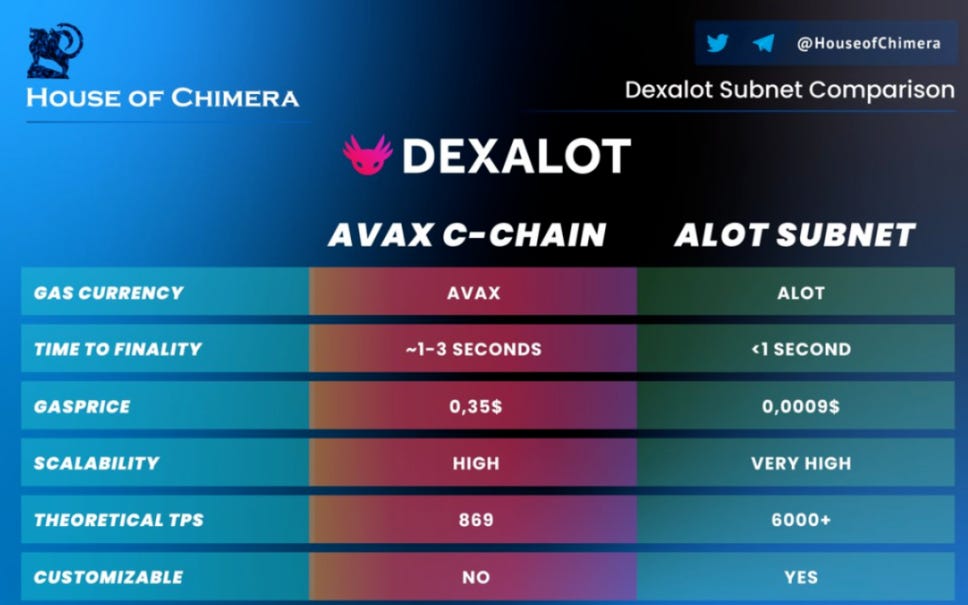

However, it should be noted that 90% of Aave V3 is on Avalanche, which is of course related to the Token incentives, but it can also be seen from the side that the Avax ecosystem is developing well. In terms of quantity alone, 7 of the top 10 projects by TVL are native projects, which are at the upper level among EVM-compatible competing chains. In terms of ecological segmentation, it is also relatively rich and healthy, with both large cross-chain protocols (Aave, Curve) and native boutiques (TIME, Traderjoe, Benqi). The categories include DEX (general and stablecoin exchange) and lending that serve as infrastructure, DeFi Lego's income aggregation projects and insurance, DeFi 2.0 (Defrost (Abracadabra), TIME (OHM)), the popular GameFi (Crabada), and projects that have strategically migrated from other chains (NFT platform Kalao migrated from Wax). In terms of coverage, DeFi and GameFi have not been missed. From the fact that TIME's market value once exceeded OHM, it can be seen that Avalanche's ability to create momentum and popularity are not low. From the official website traffic in the past year, SOL and ETH have long occupied more than 60% of the total volume; Polygon and Avax are also hovering between 10% and 20%; other chains account for a single digit. From the trend, Avax's incentive plans in August, November, and March have played a significant positive role. However, after losing the incentive, it has declined in the past two months; Ftm also has a similar trend, but the decline is more obvious; SOL and Polygon can basically maintain a high level, and Polygon's rise is also closely related to the recent hackathon; Near has maintained an upward momentum overall this year. From the perspective of the regions visited, there are also obvious characteristics: Avax has a Turkish background, Polygon has an Indian background, and Near has an Eastern European background (it is strange that Near also has a lot of traffic in Vietnam and Thailand?). However, in terms of volume and distribution uniformity, Avax and Polygon are basically at the same level, lower than SOL and Near. Let’s take a look at the visits to each blockchain browser. We believe that this indicator is more representative of real/retained users than the official website traffic. Looking at the total visits to ETH and BSC in the past year, It obviously accounts for a larger proportion, but BSC shows a continuous downward trend; SOL has the fastest increase; Polygon/Avax/Ftm have retained a certain amount after falling from the peak; Near is the lowest but also shows an upward trend. From the natural search of hot words, the most searched categories for each chain are several conventional categories: wallet, bridge, explorer. Avax is most concerned about the more conventional and application-oriented ones, while future-oriented ones like Subnet are rarely concerned. Ftm and Polygon also present a similar situation. After all, they are both EVM chains and have applications right from the start. It is worth mentioning that Polygon's Miden and Zero, which are more technical, have very few searches. On the SOL side, in addition to conventional keywords, Status, Rpc, and NFT are more concerned, which also indirectly reflects the characteristics of the chain: NFT is popular, and status often has problems. Near's NFT is searched more. We can observe from W3’s self-created tool “Twitter Hot Word Search Chart” that the Twitter search volume for Avax started in August last year and reached a peak in November. It reached its peak in June and remained at a relatively high level in the following six months, until it began to decline in the last month. TL;DR: From the perspective of users, funds, and traffic, SOL is undoubtedly the No. 1 altL1 due to the previous outbreak of applications. Near is a dark horse worth observing. Polygon and Avax are at the same level, and Ftm is relatively poor. Compared with the flow of users and funds, the observation of public chain developers may be a better indicator for evaluating the future development of a public chain. We will look at it from the following dimensions. We observe the following public chains from W3's self-created tool "Public Chain Developer Statistics Chart", and we can roughly draw the following conclusions: From the two indicators of the absolute number of code submissions and the number of active developers, it can be seen that Near, SOL, and Avax are among the top, indicating that they have done more work on the update and iteration of public chains. After experiencing the active period of development last year, the activity of the development of each public chain itself has declined. This phenomenon is particularly obvious in SOL and Avax, but Near has shown a completely different trend - it has maintained last year's active level and has an upward trend. Further, there is still a lot of optimization work to be done at the bottom layer, and the team is also actively building it. Compared with the development activity of the public chain itself, the development activity of ecological projects will be a more effective indicator for observing the development of the public chain ecology. In terms of volume, SOL and BSC have long occupied the top two positions, followed by Near/Polygon/Avax, and Ftm is at the bottom. The development activity fully reflects the outbreak of public chains: BSC and Polygon started to gain momentum in the first quarter of last year, with a peak around May, and then showed a downward trend (especially for Polygon). BSC has many subsequent projects, but the loss of developers is obvious; SOL has a strong trend. The number of code submissions increased by 9 times in the past year, and the number of developers also increased by nearly 4 times and reached a high point in February this year. The indicators have fallen significantly since the beginning of this year, but still maintain a high level (especially the number of developers); Near has the best performance in both indicators and has been in an upward state. The growth of developers has exceeded 4 times, which is the largest increase among all public chains, and the decline is also the smallest; Avax is relatively stable, with data rising by 2-3 times. After reaching a high point in September last year, it began to decline. The increase is not as good as SOL and Near, and the decline is relatively larger. Overall, SOL, Near, and Avax performed very well, especially in terms of developer retention, with a high retention rate of 68%, 80%, and 60% respectively, basically reaching the level of ETH (72%). In comparison, the retention rate of other public chains is less than 40%. However, due to the smaller size of Avax and Near, whether they can maintain this level remains to be observed. Finally, we can observe the traffic of new developers from the visits to the developer documents of each public chain in the past year (only SOL, Avax, Near are selected, and other chains have greater interference factors and are not of reference significance). We can draw similar conclusions: SOL has the largest volume, and its trend is similar to Avax. It has declined after the peak in the third and fourth quarters of last year, but still maintains a certain amount of visits; Near has the smallest volume, but its trend is different from theirs. Although it has declined slightly recently, it has maintained an upward trend overall. TL;DR: TL;DR: From the perspective of the indicators of various dimensions of developers: SOL has the strongest overall performance, followed by Avax, Near has the fastest growth, Polygon and BSC are large but in a downward trend, and Ftm has the worst overall performance. Subnets are divided into private chains and public chains, both of which can be customized according to customer needs. The two subnets currently in operation are both games. However, Avalanche currently has no communication solution between subnets, and the asset transfer between the mainnet and subnet is currently handled by a third-party bridge. DFK chain 4.1 DeFi Kingdom, the ace chain game attracted from Harmony, established a subnet DFK chain (avax provided 15 million incentives) DFK Subnet uses a customized EVM, which combines the directed acyclic graph (DAG) model in the EVM, allowing the blockchain to expand efficiently at a lower cost. Currently, the network has only 8 verification nodes and 40,169 addresses. Recently the network usage rate is less than 1%, and the rough estimate of the theoretical TPS can reach 600 SwimmerNetwork Before 5.14, the game Crabada on the C chain established a subnet Currently the network has only 8 verification nodes and 24,892 addresses. Recently, the network utilization rate is less than 4%. A rough estimate of the theoretical TPS can reach 150 Possible subnets in the future shrapnel: 3A shooting game Arrow Markets: Decentralized options protocol Dexalot: High-performance DeFi subnet. The following figure shows a comparison with C-chain. According to the publicity parameters, it is superior to C-chain in all aspects The adoption of enterprise-level institutions may become the next narrative focus of Avalanche. The initial effect of the cooperation is not significant (need to be observed): NFT: Cooperated with collectibles company Topps to issue a 2021 MLB NFT collection Payment: Digital payment platform Wirex announced the integration of Avalanche. The payment platform has 4.5 million traditional users Litigation Product ILO: Cooperating with law firm Roche Cyrulnik Freedman LLP and consulting firm Republic Advisory Services STO: Cooperating with US STO agency Securitize, which can use Avalanche chain for the issuance and management of private securities CAYG Disaster Relief Platform: Deloitte uses Avalanche for its disaster relief platform to improve efficiency and reduce costs through blockchain technology 3.1 Wallet core Ava Labs Released non-custodial multi-function wallet (browser extension): Core, with the following features: (1). Avalanche bridge, supports native BTC cross-chain. Currently, there are more than 690 BTC cross-chains, and ERC20 will be supported in the future (https://snowtrace.io/token/0x152b9d0FdC40C096757F570A51E494bd4b943E50) (2). Support NFT, subnet display (currently DFK chain, Swimmer) (3). Deposit and withdrawal (supported by MoonPay) (4). Basic swap function 3.2 Avalanche Summit in Barcelona A peek at the future direction of Avax from this hackathon in March: The 5 awards and winning projects given by the official Avalanche foundation are: EVM optimization solution (OracleEVM) Ledger-compatible subnets (SubnetX, ledger-compatible subnet creation and management tools) Create management tools for subnets (subnet.center, an analysis and notification platform for validators, delegators, builders, and users) Customized VM subnet solution (AEVEREST++, based on C++, with a theoretical TPS limit of 13,500) Create on subnet Dapp (zk-id, zero-knowledge identity protocol) In addition to the official awards, some institutions/projects were invited and set up awards: Axelar (cross-chain communication solution) Covalent (API solution) Ankr (node service) Aventures DAO; Chainlink Dexalot (DeFi subnet) Hacken (anti-hacker attack) LayerZero WOWswap Coinbase wallet From the award setting, it can be seen that Avax is currently focusing on the exploration of subnet construction, from the bottom-level execution environment optimization to project creation, and working hard on every aspect of the development experience. In summary, The technical capabilities/architecture of the Avalanche public chain itself are in line with the future multi-chain trend, and capital support is also at the upper-middle level From the perspective of the richness, popularity, and retention rate of ecological projects, the overall level is high, and the comprehensive ecological score is at the same level as BSC, SOL, and Near, which is higher than other competing products. From the perspective of public chains and ecosystems, SOL > Avalanche > Near > BSC > Polygon > Ftm (Since Cosmos and Polkadot are still in the early stages of construction and their ecosystems are just taking shape, they are not listed as comparison objects in this "ecosystem comparison session". However, we highly recognize the direction of their public chains and the capabilities of their teams, and will focus on observing them later.) The Avalanche ecosystem has new narrative capabilities for customized subnets/VMs and enterprise construction, as well as the ability to create momentum in the lower-level communities (grabbing projects and creating high-level imitations). Its ecosystem may take a different route from ETH and altL1/L2 in the future, and is worthy of continued observation. Follow-up observations Progress of enterprise cooperation Subnet interactivity and performance The outbreak of ecological projects (including imitations) Community enthusiasm, funding, and whether developers are sustainable Hackathons and other developer activities and project implementation

3. Traffic

V. Developers

1. Public chain development activity

2. Ecological development activity

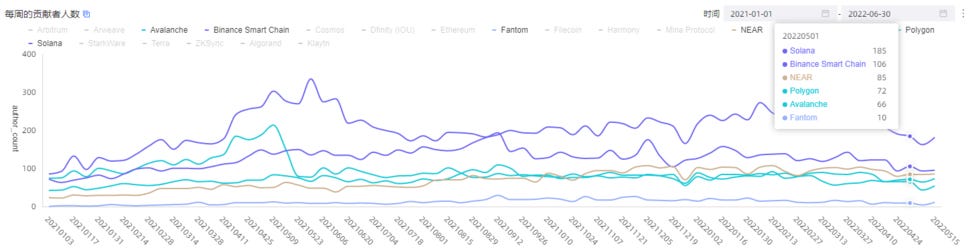

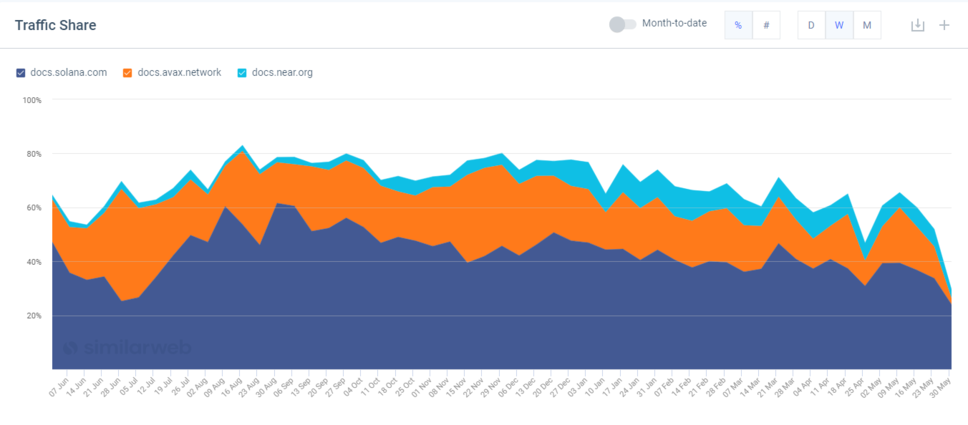

3. New developer traffic

Six, Subnets and Cooperation

1. Subnets

2. Enterprise Use Cases

3. Others

VII. Summary

References

《The AMM Test: A No BS Look at L1 Performance》

《A Comparison of Heterogeneous Blockchain Networks》

Original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia