Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

What are we talking about when we talk about Web3 Trusted Neutrality?

Original title: "Web3 Trusted Neutrality"

Original author: Luca Prosperi

Original compilation: Block unicorn

< p>Traditionally, the Roman Emperor Titus Flavius Vespasianus, when asked by his son about Rome's disgustingly large tax revenues, replied: Money It is not smelly. Vespasianus' Rome had just taxed public urine collected by leather traders (and used to produce ammonia) through a so-called percentage of sales, and the political opposition was trying to capitalize on this conspicuous source of revenue. Legend has it that the emperor lifted a coin abandoned in a cesspit in a traditional public toilet that is forever named after him -- in modern Italian, vespasiano is synonymous with urinal, and he put the The metal was brought up to his nose, and a fateful sentence uttered: ecunia non olet (Latin for money doesn't stink). While many have extrapolated the eschatological story of currency fungibility from this event, my interest remains in the urinal, and the political demonization of a hole in the wall, rather than its very artificial abuse -- That is, during depositing or collection of feces.

Today's comment. Given the critical times, I hope I can be forgiven. If you really don't have the patience to read the whole article, please at least scroll to the bottom and start reading from the title to read what you should care about, it is precious to me, and it is also true to you.

Two distinct approaches to regulation of infrastructure

For political games, It's not uncommon to assign meaning to tools rather than users. Our tendency to humanize everything in order to connect within a system and facilitate our behavior is an ancestral phenomenon that makes for a very powerful narrative. It works on the way up, worshiping the face that represents a movement or technique, and on the way down, demonizing the same movement or technology because of such acts of face. What's more, the humanization of technology (the term used here - technology, is the raw connotation of mechanically applied knowledge) artificially fuels the ascent and dramatically exaggerates the absolute human self-journey, heightening the destructiveness of the decline strength.

Gun Control This is all very common and dangerously wrong. But if you think you're immune to such civilian behavior, you're wrong. To the liberal Europeans and pragmatic Americans among my readers, I whisper: Think about where you stand on gun control legislation. Whether you despise the danger of the widespread distribution of weapons among the general populace, or welcome it in the spirit of territorial need: you may well be imbuing a piece of metal and plastic with human intent. The mathematicians among you might demonstrate that a broad distribution of self-defense capabilities could have positive effects on resource optimization and the survival of democracies that outweigh the negative effects of random violent misconduct. You can also replace guns with memory states (read ethereum) and get into a similar philosophical deadlock. While guns (and infrastructure technology) are just tools and should in principle be considered tools, ignoring or not ignoring (and to what extent) the underlying graph has several profound implications for human existence.

& nbsp;

Regarding how to (and extent) The decision of the interaction between Fan Technology and humans is in the final analysis. Decide. For my own applied research purposes, I have summarized two main schools of thought: Technology Agnostic -- TA & Technical Pragmatism -- TP.

The TA is unique in its ultra-liberal stance that technology itself should not be regulated and that regulators should prioritize the potential macro benefits of technology applications over A microscopic tragedy caused by human misuse of technology. TA tends to remain free ex ante, but strongly exercises its coercive power ex post. Its presentation of facts is also often very dramatic.

In contrast, TP seeks to anticipate human interactions with new capabilities provided by technology and to exercise its regulatory power ex ante so that any possible negative spillovers on individuals minimized. TP is high-touch and pragmatic rather than purist, and the abuse of regulated matters by ex-ante coercion and ex-post leniency TP can be attributed, at least in part, to flaws in the regulatory process.

The debate over which method to favor is well beyond the scope of our study. Preferences can be traced to what should be the ideal role of the state as a collective contract in dealing with its citizens. In a game of survival of the fittest, for the greater good of human progress, should the state be the protector of the rules of the game, or should it act like a family father who knows better and wields authority over everything within his reach? and acting in an annoying way? That's not something I can say.

This is a publication that focuses on the technical and philosophical advancements brought about by the DeFi movement, how does all of this relate to the current state of our industry? Obviously there are. With recent developments (a lot has been written about this), two ideological camps have once again formed, while some have changed sides. Humans are inherently pro-cyclical, reacting quickly to the short-term effects of their actions but less intelligently to the long-term effects. Even those who have been advocating a low-key approach to DeFi (and blockchain technology in general) have been backtracking lately. They now say the observed and potential damage was too deep.

Yes, I am a researcher/advocate/investor/builder of decentralized infrastructure and I would like to strongly advocate leaving the infrastructure alone and is to closely supervise the humans who use it. I'll let companies like @Milesjennings do the heavy lifting for the industry. My concern here is making sure we approach the debate with a solid understanding of the problem space and exposing those who thrive in gray areas.

The Importance of Credible Neutrality

In the absence of a working framework that constitutes infrastructure, we cannot debate whether technology infrastructure should fall within the purview of regulators. Ironically, I think that among radical liberals, the most active are not moved by a sincerity to protect infrastructure, but by a desire to keep the authorities out of their way while caring about their own affairs shake. Once again, we should tread carefully to avoid getting caught up in more sordid scandals. Laziness should never be an excuse.

We tend to overlook the acumen of lawmakers in dealing with new technological phenomena, but I have found that the SEC's guidance is a great way to think about what is infrastructure and how it should be regulated very useful. Excerpted from Myers' Decentralization for Web3 Builders: Principles, Models, Approaches, my emphasis is:

First, US securities laws generally aim at Create a "level playing field" for securities trading by limiting the ability of those with more information to take advantage of those with less information. This is the principle of information asymmetry, and U.S. securities laws generally seek to remove the asymmetry in certain securities transactions through the application of disclosure requirements. This principle comes into play in the Howey Test, a subjective test used to determine whether U.S. securities laws should apply to transactions in digital assets that: (1) invest funds in ordinary businesses (2), (3) ) and a reasonable expectation of profit(4) primarily based on the management efforts of others. The fourth aspect seeks to solve the problem of information asymmetry, based on trust. Where reliance is placed on "management efforts," the potential for risk of asymmetric information is high (managers vs. outsiders), so application of securities laws may be warranted.

I am not a lawyer, but even to the layman it seems that legislators do not start from the standpoint of the scope of individual liberty, but from the desired fair outcome. In my view, retail investors generally benefit from the strictest form of protection, which has more to do with a recognition of the retail industry's inherent disadvantages when dealing with professionals than some ideological intent to control the masses. As Miles pointed out, (4) is still more interesting in the context of Web3 infrastructure. The author continues -- my emphasis is:

Based on the above and the SEC guidance, we can speculate that if Web3 systems can (A) eliminate the occurrence of significant information asymmetries , (B) removes reliance on the management efforts of others necessary to drive the success or failure of that business, then the system may be “sufficiently decentralized” such that U.S. securities laws should not apply to its digital assets. In this post, I refer to these systems as legally decentralized. Admittedly, most businesses will not be able to meet the threshold of decentralization in statute, but as I outline below, novel components of Web3 systems enable them to meet such a threshold.

Then the question arises: Are most efforts to address (or facilitate) the use of encryption sufficiently independent of administrative efforts and controls? Interestingly, CeFi exploits a narrative of convenience for the average user to disguise the fact that it is simply a very centralized business, unencumbered by any of the boundaries and protections regulators have put in place over the years to avoid pulling the rug . But I wouldn't shoot a dying body. However, while the answer to all so-called CeFi projects is a resounding no, I think the same is true for most successful crypto-native DeFi projects.

A short story of financial innovation

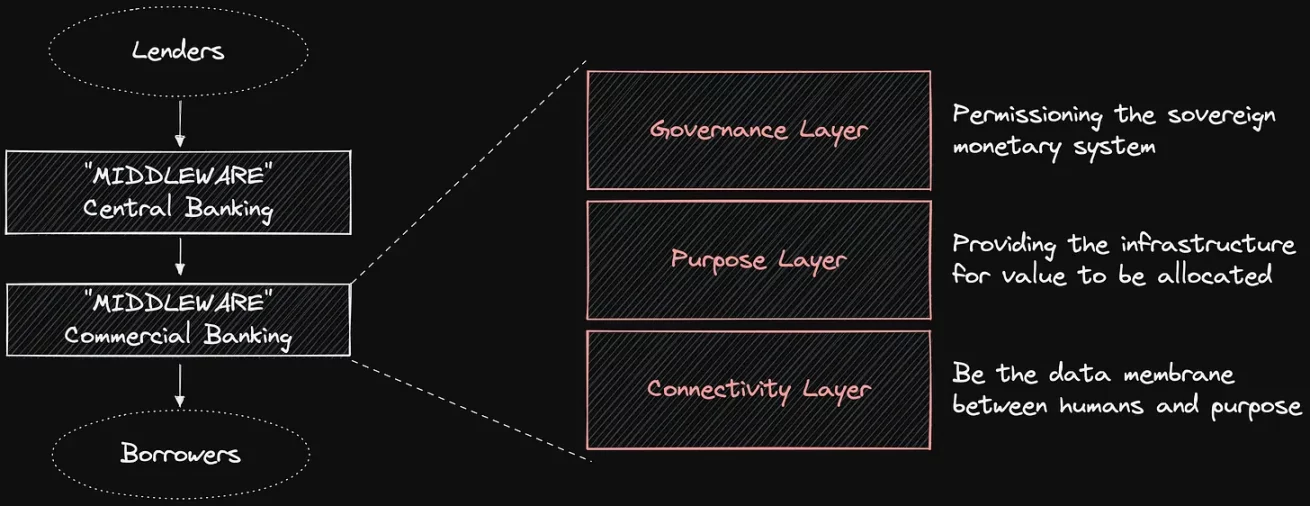

I have been joking that money is Most complex product accepted. The set of mechanics behind this piece of paper we call dollars is profound, but all of these complex interactions have been smooth (enough) for users to ignore. For most of us, a dollar is just a dollar, not a physical representation of future government debt. The maturity mismatch and allocation complexities of these liabilities are managed on an ongoing basis by an intricate network of qualified financial intermediaries. Users just use USD, that's all. In exchange, the minters of these dollars can finance themselves at extremely attractive (and predictable) exchange rates. In other words, modern currencies are extraordinary middleware for value transfer.

Currency middleware can be broken down philosophically into a composition of three different layers: Governance- In which to decide what can come and interact with the middleware, the purpose - representing the infrastructure through which value is managed, and the connection - forming the front end that connects the user and the infrastructure.

As always, macroeconomic factors played a key role in guiding innovation. So-called tech finance, for example, has largely focused on the connectivity layer over the past 10 years -- that is, trying to achieve and package alternative forms of yield to satisfy a return-hungry market that has had zero real yield for almost 15 years. Meanwhile, not much has changed at the infrastructure level of wholesale banking, with large parts of the system still running on antiquated tracks. Governance, however, has always been a battleground of two distinct armies: on the one hand, instruments that seek to amplify traditional agnosticism - LTROs (the ECB's traditional financial instruments), TLTROs (Targeted Long-Term Refinancing Operations) and the extraordinary monetary The centralizing force of the measure, on the other hand, is the decentralizing force aimed at redesigning the monetary balance of power.

To me, DeFi is just good infrastructure on the consensus layer, while the political impact of blockchain technology and distributed systems is huge and groundbreaking . Meaningful innovation in DeFi has largely focused on infrastructure advancements -- eg: automated and open source market making, derivatives structures, margin lending, and collateral management capabilities. Instead, DeFi’s success and influence in governance is, in my opinion, vastly overrated — and riddled with immature or dishonest ideologies. We spend a lot of time discerning between good and bad infrastructure design and good and bad governance mechanisms, and I must say that there are very few examples of good governance.

What is good DeFi governance My main conclusion (so far) is that a well-designed governance mechanism should:

< /p>

Guaranteed censorship-resistant (basic consensus layer). Incentivize good deeds (minimize evil deeds). Minimize (meaningful) human intervention (beyond maintenance). Stalling infrastructure, isolating the human element

If we focus on the protocols that provide crypto-native access to lending today, the picture is bleak -- as usual Again, we look at Maker as an example.

Censorship - Resistance: Maker effectively centralizes control with founding team Incentives for good in hand: a combination of permissioning decisions (i.e. this collateral has the characteristics required to open a vault at Maker) and funding decisions (i.e. the protocol will implicitly fund this collateral and socialize the risk) , when coupled with unsatisfactory censorship-resistance, accepting anything more complex than $ETH and $BTC is dangerously artificially minimal: although Maker still relies heavily on humans to develop (e.g. monitor risk parameters, provide new collateral) and running (e.g. governance oracles and liquidation engines) the protocol, but the human footprint is transparent enough in a way that those interacting with the protocol can draw their own conclusions isolating the human factor: any Anyone with a head can see where the protocol stops, who is making the fundamental decisions, who is driving risk taking and management decisions

Dynamic standard for any decentralized test The minimum satisfaction threshold for , as shown in the graph above, should vary depending on the activities the protocol is engaged in -- or better yet, the activities to which the protocol is directed by its governance participants. Although few would argue that Maker operates as a centralized management company (based on SEC testing). Back then it offered a transparent funding window for anyone wanting to gain leverage against their $ETH or $BTC, but things are murkier now. Given that the protocol now accepts significant (profitable) counterparty and collateral risk (central lending facility's approved debt ceiling is approaching $500M), at the expense of $DAI holders, Maker can also be considered neutral infrastructure? I do not think so. The agreement is currently driven by (highly contested) management decisions that shift rewards and risks at various points and provide some insiders with preferential views over other participants. This means that, in all its forms, $MKR can be considered a security. And $DAI, assuming it will start floating at some point, reflecting the risks inherent in the maker liability profile, should also be considered a security.

But it is fascinating that projects with less enduring success within DeFi may be the only ones that meet the decentralization test. Liquity and Reflexer are good examples. When you stop and think about it, there's nothing surprising about this. Infrastructure should be just infrastructure, the relevance of which should be attributed not only to its intrinsic characteristics, but primarily to the external conditions and creativity of its users. There are no successful or unsuccessful bridges, sometimes there are poorly designed bridges, but well designed bridges go nowhere; sometimes there are well designed bridges connecting two prosperous economies, but poorly designed bridges are very strategic Places of meaning survived, and so on.

Things you should care about

It would be great if you could see this all the time . If you skipped it and went straight to this, well done. We're approaching David Foster Wallace's level of reflection in this debate, and things should come to a conclusion. As such, you can find a well-crafted debate on the implications of crypto regulation below my Wittgenstein-esque guide. I print it next to my screen. Maybe I should send it to Bankless for some higher quality podcasts -- just in case.

A. Is the term infrastructure a relevant discriminant for your analysis?

B. Given A, do you have a good definition of the (neutral) infrastructure?

C. In the case of B, do you think the analysis object satisfies it? If yes, why?

Analysts will likely realize that, assuming A and B, most protocols active in DeFi fail C. Few protocols are decentralized by any form of good definition. For most crypto projects, decentralization is an illusion or a disguise. But let's assume C is satisfied and move on.

D. Given C, can you clearly distinguish the actors interacting with the infrastructure?

E. Given D, can you identify the effective capabilities of governance participants?

Now, you have an effective discriminant, a good definition and a satisfactory manual. So this debate is all up to you. Don't trust those who turn a dry analytical process into an impossible ideological campaign, because they may well be hiding something. But if you want to heed one piece of advice, all that energy and passion is better spent creating the proper infrastructure layer for the future of finance. It will also boost the work of those actively working to protect the ecosystem from misguided politicians and at-risk incumbents.

Original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia