Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

New narrative or cut again, Su Zhu into the bureau encryption claims market GTX can become

Recently, according to a financing information circulated in the market, Su Zhu and Kyle Davies, the original founder of Three Arrows Capital, are preparing to build a new centralized encrypted trading platform "GTX", The platform, whose co-founders include Sudhu Arumugam and Mark Lamb, CoinFLEX's co-founders, has sparked much discussion in the industry.

Some people think that the bond trading market formed for crypto assets is indeed a neglected blue ocean market at present, but also a good business to make money. However, there is also a different view. Based on Su Zhu's and GTX's other partners' previous failures and credit depreciation in the crypto sphere, their new trading platform will be used by no one.

So what kind of market is debt trading, and how did it form and develop before? Su Zhu has officially entered the crypto bond market. What is the chance of GTX, which he helped create, or is it just another "leek harvesting"? BlockBeats will make the following introduction and analysis.

The advantages and origins of debt trading

First, let's look at what problems are solved through debt trading and how it can be traced back to its origins.

Corporate bankruptcy is one of the most misunderstood topics in the business world. For many people, the first words that come to mind when they hear about a company that has filed for Chapter 11 bankruptcy protection are often "failure" or "loss." Bankruptcy is rarely associated with words like "opportunity."

This is often because Chapter 11 bankruptcy is a complex court process for both debtors and creditors. Many complexities and unpredictability occur during the legal process, and Chapter 11 does not always lead to a favorable recovery for all parties involved.

Fortunately, though, there is another, more convenient recovery option for creditors caught up in the chain reaction of endless Bankruptcy cases, and it's a little-known area of corporate bankruptcy: a common practice known as Bankruptcy Claims Trading, or "debt trading."

In the normal course of bankruptcy proceedings, a creditor asserts its right to repay by submitting a "proof of claim" to the debtor, which specifies the amount owed to the creditor based on its accounting records and which the debtor is obligated to pay. In addition, the creditor usually provides supporting documents (i.e., contracts, invoices, lease agreements, etc.) along with the proof of claim form submitted as evidence of the creditor's bankruptcy claim.

But after all that, creditors still have to wait for the debtor's bankruptcy case to work its way through the court process before their claims can be approved and payments released, a process that can take years before creditors receive any amount owed to them. In addition, for creditors seeking recovery assurance and financial certainty, the outcome of their bankruptcy adds some uncertainty due to four factors:

1) Check claims

A creditor's claim is considered valid if proof of claim has been submitted or if the debtor does not object to the claim. At the same time, the debtor can also object to the claim, so as to make the claim invalid or rejected, thus reducing its own liability, so as to facilitate restructuring. If the debtor's objection is successful, the court will dismiss the claim and the creditor will not be able to share in the payment distribution from the debtor's bankruptcy estate. For creditors, opposition from debtors and rejection of their claims by courts may lead to increased uncertainty about eventual recovery.

2) Priority of creditors

Another factor contributing to the uncertainty of creditor recovery is the priority of bankruptcy claims. This is the result of the Chapter 11 claims classification process, which determines the creditor's priority in getting paid. Prior to the payment of the lower priority claims, the higher priority or secured claims will be paid in full from the debtor's bankruptcy estate. Unsecured and equity holders, on the other hand, fall into the lower category of bankruptcy claims and typically pay only a percentage of their claims, offer alternative payment methods, or receive no payment at all.

3) Debtor restructuring plan

Within 120 days of the bankruptcy filing date, debtors must submit a reorganization plan outlining how they plan to reorganize and re-emerge as healthier businesses, but they also reserve the right to request an extension if needed. In this process, it takes time not only for the debtor to formulate and submit the reorganization plan, but also for the creditor to review, vote and approve the terms of the reorganization plan, and there are often some differences between the two parties on the future reorganization plan.

4) Claim procedure

Upon receipt of the court's confirmation of the restructuring plan, the claims process began. Finally, the debtor can begin implementing the approved plan and begin making payments to the creditor in the order defined by the creditor's class and seniority level. Even at this point, if the funds in the bankruptcy estate are exhausted, creditors with unsecured claims may not receive payment or may be offered alternative forms of remedy.

Given these uncertainties, this is why debt trading offers creditors a unique opportunity to recoup their losses and minimize uncertainty.

In addition to waiting for a lengthy bankruptcy claim process and potentially protracted court proceedings, creditors can choose to monetize their claims in exchange for immediate cash. Thus, a claim transaction describes a financial and legal transaction in which a creditor sells its title in a claim in bankruptcy and transfers it to another entity in order to obtain immediate monetary payment of the claim from the buyer.

In short, creditors are selling their receivables for immediate cash from interested buyers. As a result of this transaction, a formal claim for this debt has been recorded in bankruptcy court and legally transferred to the Buyer, who then assumes the risk of recovering payment from the debtor.

Although there is no official historical record of the origins of bond trading, the first instance of debt trading in the United States dates back to its founding. After the Revolutionary War, the 13 founding colonies of the United States became financially insolvent after the war. They owed debts to individuals who fought in the war, such as soldiers, farmers, and merchants. Opportunistic buyers bought these claims on the insolvent colonies at a discount, hoping to eventually recover all payments when a new U.S. government was formed.

Crypto claims market status and opportunities

In a traditional credit transaction, most of these steps are handled manually and via paper documents, fax transmissions, or telephone/mail communications. It is the responsibility of creditors and buyers to cooperate with each other to make the transaction successful. Similar to buying a house, the process can be very complicated, and each manual step has the potential to go wrong and jeopardize the transaction.

Before there was a centralized bond market, there were mainly OTC markets where buyers and sellers negotiated and settled in QQ groups through phone calls or E-mail documents or even some domestic transactions. Debt trades either directly from seller to buyer, or indirectly from seller to buyer through a broker. The market is highly lopsided, with tens of thousands of creditors in a bankruptcy case but orders of magnitude smaller buyers.

As markets evolve, this process today is not only inefficient and inconvenient for both sides, but also risky and opaque, making a currency recovery harder to achieve. There is therefore an urgent need for the bankruptcy claims market to build a centralized platform that digitally connects creditors with verified buyers and provides a secure and reliable online environment to trade claims efficiently and recover cash quickly.

In the crypto space, with the cascading explosion of crypto companies in 2022, including the bankruptcy of FTX alone, millions of crypto account holders have become creditors of the exchange. 'This is going to be a $20 billion emerging market, so there is a greater need for tailor-made solutions in this segment to help unlock frozen accounts,' Mr. Zhu said.

而目前,也越来越多的加密索赔平台将技术和自动化引入了这个受效率低下和信息不对称困扰的债权交易市场。旨在帮助用户解决 3 个核心问题:帮助债权人获得最优惠的价格、提供透明的结算文件以及构建可预测的结算流程。

In terms of mechanism design, in order for each creditor to claim and recover as much as possible, most platforms charge zero fees for creditors to register, list, sell or transfer claims, while small transaction fees for payment platforms are often provided by the buyer.

Buyers' offers, on the other hand, are generally non-binding and subject to a 48-hour due diligence period and standard contract terms. Once the buyer agrees to proceed with the claim purchase and offers any proposed contract modifications, the Platform will notify creditors of the proposed transaction terms. If the creditors accept the proposed terms, a binding transaction confirmation is created and the parties proceed to complete the transaction.

These platforms take the hassle out of transactions when users trade claims, allowing them to process the necessary paperwork so that users can quickly proceed with their business. Once the transaction closes, the platform submits all the necessary documents to the court, fully resolves the assignment of claims within a very short time after the parties sign the assignment agreement, and handles all the administrative work of notifying the court and updating the claim register through integration with the bankruptcy court and the claims agent.

Primary rival

With the disclosure of GTX financing documents, Su Zhu began to formally enter the bond trading market, first focusing on FTX's debt trading after the bankruptcy. He believes that FTX creditors, who are currently unable to propose assets from the platform, but the current debt market with cumbersome procedures and high fees, is very unfriendly to the experience of small creditors, and GTX will build an order book like BTC, full of depth of debt trading market. And the ability to use bonds as collateral for transactions to increase financial liquidity.

Prior to that, major crypto bankruptcies included Mt Gox in 2014 and QuadrigaCX, Canada's largest cryptocurrency exchange, collapsing in 2020, but capacity was still very limited. With Luna, Three Arrows Capital, FTX, and Celsius and many others going under in 2022, a crypto bond market has been created that is hard to ignore.

In addition to GTX, the core team of Three Arrows co-founders Su Zhu and Kyle Davies, and CoinFLEX co-founders Sudhu Arumugam and Mark Lamb, There are still two major players in this space, Xclaim and Claims-Market.

Xclaim

XclaimFounded in 2018, it offers transparent pricing and fast execution to every crypto claimant. It is made up of a diverse team of engineers, data scientists, financial and legal experts, and more. Matthew Sedigh, founder and CEO, has 15 years of experience in the corporate restructuring industry.

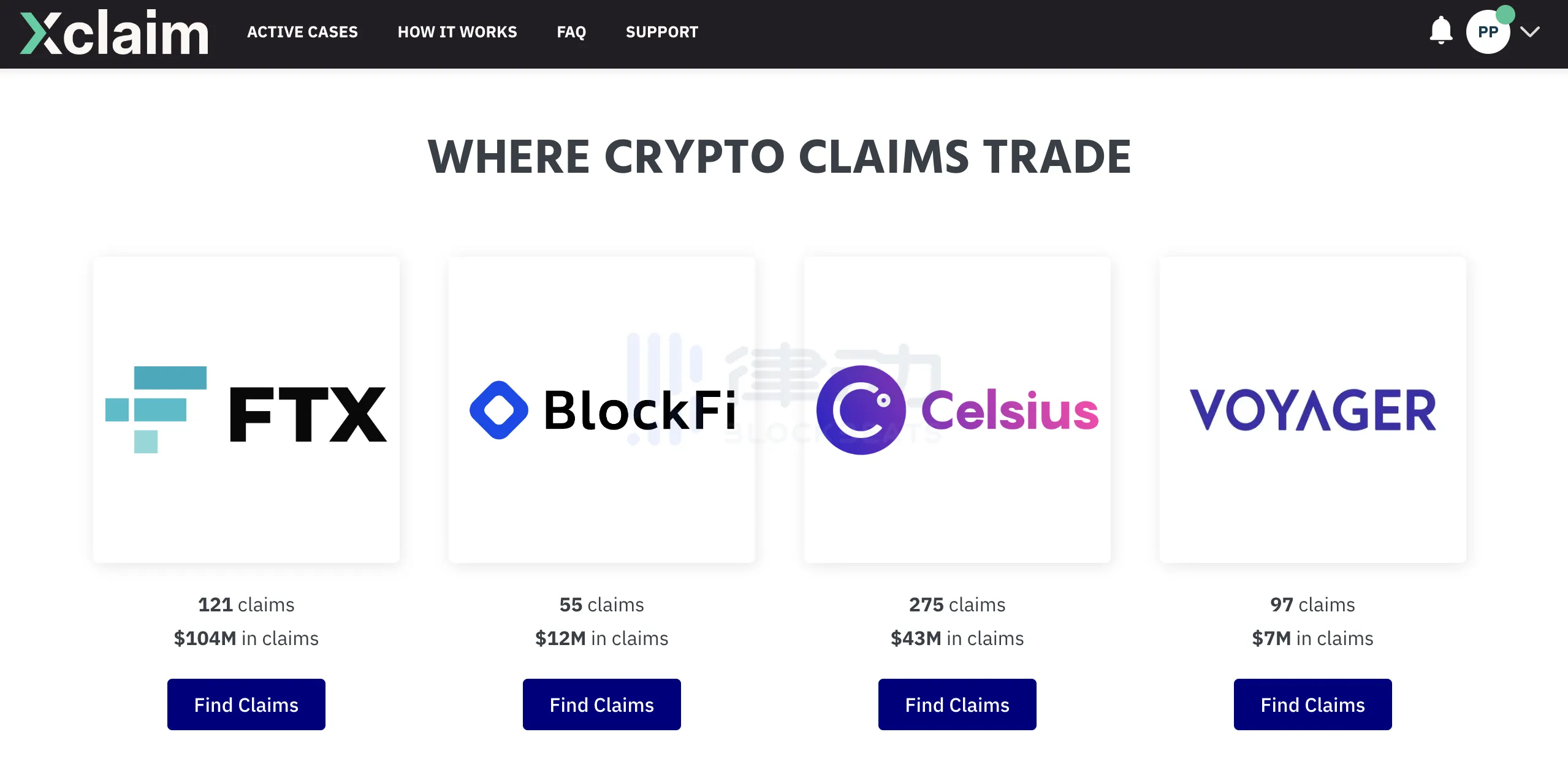

Xclaim is now available to trade claims on four insolvency platforms, FTX, BlockFi, Celsius, and Voyager, with more than 500 people listing tradable claims and $166 million in assets in the market.

On the other hand, the level of interest on a user's claim may vary depending on the asset attribute of the claim and the state and timeline of the bankruptcy case. Platform data shows that FTX claims are currently trading at 15.5% of the total value of the account, while BlockFi, Celsius and Voyager claims are trading at 30.5%, 19.5% and 38% of the total value of the account, respectively.

On the platform edge, although Xclaim Marketplace does not include secured claims, it has more than a million priority claims, Administration 503(b)(9) (Bankruptcy Code provides that creditors can file administrative expense claims against goods received by the debtor within 20 days), and general unsecured claims available for trading. The user's operations are mainly divided into the following four steps:

1) Sign up for an encrypted account and provide basic information to share with other users interested in purchasing bankruptcy claims

2) Get a deal and ensure fair market value by comparing multiple offers from the largest online buyer network

3) The platform will only trade at the price accepted by creditors, and support and handle all legal matters along the way. Nothing is final until the creditors sign

4) Make final payments to creditors' bank accounts

In addition, Xclaim offers a claim calculator tool and a phone call with a creditor's attorney. A claims calculator helps creditors estimate the value of claims in their accounts based on their expectations of the bankruptcy process, market conditions and timing, so they can make a more informed choice about whether to sell their claims today for cash or wait for the court process to play out.

Claims-Market

Claims-MarketIt's an investment bankCherokee AcquisitionThe market structure of its claims products is also designed for creditors. After the seller's price is accepted by the buyer and the transaction is confirmed, the buyer and the seller will introduce to each other and the transaction will take place directly between the buyer and the seller. Again, the management fee is paid by the buyer, and the seller does not pay any fee.

Vladimir Jelisavcic, Cherokee Acquisition's manager and founder, has said that clients holding about $1 billion in credit claims are interested in selling their claims through Cherokee, Cherokee matches creditors with debt buyers, mostly hedge funds, who sometimes own part of the debt. He was also struck by the bankruptcy of crypto organisations such as FTX, Voyager and Celsius. Many customers will only recover a small percentage of their total assets from these platforms, but rather than wait for the lengthy bankruptcy process to play out, many are choosing to get some money now.

Another frustrating aspect of bond trading is not knowing when the buyer will pay. There can be many reasons for this uncertainty: complex, unsubstantiated claims requiring extensive due diligence, legal counsel inexperienced in selling trade claims, and buyer delays in preparing closing documents, among others.

As a result, Claims-Market lists only intended marketable counterclaims on the platform and encourages buyers and sellers to use simple claims assignment. A simple Claims transfer agreement, called SAC, will balance the interests of buyers and sellers, with SAC providing buyers with the guarantees they need, such as representations and warranties, as well as the right to pay back prorated amounts if the allowable claims fall below the minimum. SAC gives the seller the right to collect additional payments from the buyer if the allowable claim amount is higher than the minimum claim amount.

Claims filed on the claims-market using SAC will be signed before the seller lists them, providing the buyer with a guaranteed settlement. Since all buyers agree to use SAC, transaction costs and delays are minimized if sellers also agree to use SAC. If a specific change to SAC is chosen, the friction of negotiating time and money will also be minimized because the buyer will only have to focus on the seller's specific redlining change to the SAC.

In addition, Claims-Market has developed the simple pass-through Distribution Protocol "SPTA" to facilitate secondary transactions of claims. In some cases, the middleman will act as a risk-free principal to satisfy the buyer's requirement to face the middleman. In other cases, where an investor may wish to sell a claim to a buyer without having to make representations and warranties that are customary for the original creditor, the SPTA allows intermediaries to make representations and warranties that relate only to their own conduct.

So far, creditors have sold $83,753,768.45 in 202 transactions through Claims-Market, according to platform data. The transaction amount of cryptoasset creditor's rights reached $32877101.8, and it mainly provided creditor's rights trading on 3 bankruptcy platforms Celsius, FTX and Voyager.

summarize

1) With the successive bankruptcies of Luna, Three Arrow Capital, FTX and many CeFi institutions in 2022, the bond trading market for crypto assets has gradually grown and may reach a scale of 100 billion dollars, but it has not received much attention at present. At the same time, the creditor's rights transaction on the bankruptcy platform is a market where the buyers and sellers are very unequal, and the buyers are much less than the sellers. In terms of matching transactions, the platform often charges higher transaction fees than the general spot trading platform, so this circuit is indeed a good business to make money.

2) At present, there are not many players in this field. It is still a blue ocean market, mainly consisting of Xclaim and Claims-Market. Although these two institutions have been established for four or five years, according to their official disclosure of cryptoasset creditor's rights transaction data, they are $166 million and nearly $33 million, each accounting for about one thousand of the total market size, there is still a great opportunity for late entry projects such as GTX to catch up.

3) The core team members of GTX include Su Zhu, two co-founders of Sanarrow Capital, Kyle Davies, Sudhu Arumugam, and Mark Lamb, two co-founders of CoinFLEX, as well as senior executives of many former crypto financial institutions. Compared with grassroots team entrepreneurship, GTX still has certain advantages. Along with the new narrative of crypto-debt trading, GTX could still gain some investor appetite.

4) However, based on Su Zhu and other GTX affiliates' previous bankruptcy experience, as well as their current reputation in the industry, it will not be easy for GTX to gain the recognition of investors and trust of users. For example, the founder of Wintermute has written a letter distancing himself from GTX and saying that he will not participate in the investment.

5) After several years of development, Xclaim and Claims-Market have their own characteristics in the products that provide Claims transactions, have captured a large number of users, and are more adept in handling administrative work related to courts in various countries. The specific products of GTX are planned to take 2-3 months to officially launch, and the future success of the GTX project, the most basic or back to the product release after the user experience, as well as long-term operation, remains to be further observed.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia