Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

InfinityPools: 1000 times leveraged non-clearing perpetual contract has come true?

Although in the field of encryption, "don't touch the contract" is a well-known old saying, we have to admit that leverage is the key to the current growth of the encryption market One of the biggest dynamics, more so in the past bull market. In fact, when all risks are effectively controlled, the use of leverage is not entirely a bad thing.

But right now, even in liquid markets like BTC and ETH, It is very difficult to achieve liquidation, especially in the case of large market fluctuations. In order to ensure the effective operation of the perpetual contract market, trading platforms often increase the amount of liquidation penalties, or set a stricter upper limit on the transaction size. When these measures fail, trades are forced to settle and traders do not get paid on their profitable positions. What's more frightening is that the main income of the trading platform also comes from liquidation, and when the interests of the two parties in the transaction are inconsistent, there are often embarrassing stories.

InfinityPools, developed by Lemma Labs, solves this liquidation risk of perpetual contracts. By allowing all positions in the protocol to be perfectly closed, traders can add unlimited leverage to any asset without counterparty risk.

Basic logic of InfinityPools

InfinityPools is a two-way market, with traders on one side and liquidity providers (LPs) on the other, by pre-assuring the spot liquidity needed to close positions sex to solve the liquidation problem. LP deposits its LP Token on Uniswap v3 or other AMMs into the agreement for traders to use, and obtains superior and more sustainable benefits than AMM transaction fees through the funding rate. Traders borrow LP's centralized liquidity range from the public liquidity pool and put it into the private trading pool for long or short operations.

Since the trader's operation is based on the private trading pool contract, there is no need to consider the rise and fall of the spot price of the asset when closing the position, and no liquidation will occur due to the fall of the spot price. When closing positions, traders are free to choose a private trading pool or other AMM agreement to exchange positions for cash to repay the loan, so the agreement does not need to use price oracles, and the agreement itself is completely permissionless.

We can use the following example to briefly understand the leverage logic of InfinityPools:

< p>We assume that the current market price of ETH is 1000 ETH/USDC, and the trader borrows ETH worth 1000 USDC on InfinityPools -USDC LP Token, the liquidity range of this LP Token is deployed within a narrow liquidity range with 900 ETH/USDC as the center price. If the trader wants to go long ETH, he can first redeem LP Token for 1000 USDC (because the market price is higher than the liquidity range, so the assets in LP Token are all USDC), and exchange it on other DEX for 1 ETH.

According to the rise and fall of ETH market price, this trader will face three situations:

p>

1. If the price of ETH rises and the value of 1 ETH is greater than 1000 ETH/USDC, the trader Part of 1 ETH can be exchanged back to 1000 USDC, and the borrowed LP Token can be repaid to close the position.

2. If the ETH price falls above 900 USDC and the value of 1 ETH is greater than 900 ETH/USDC but less than 1000 USDC, the trader needs to use 100 USDC or 0.11 ETH as collateral to repay the value of 1000 LP Token of USDC.

3. If the price of ETH falls below 900 USDC and the value of 1 ETH is less than 900 ETH/USDC, then the trader needs to add 0.11 ETH as collateral on the basis of the 1 ETH already held. Repay LP Token with a current value of 1.11 (because the price is lower than the liquidity range, the assets in LP Token are all ETH). At this time, the value of 0.11 ETH does not exceed 100 USDC at most.

It is not difficult to see that no matter how the price of ETH fluctuates, the collateral required by this trader to do long is 100 USDC, So in this case the trader achieved 10x leverage. When the borrowed liquidity range is closer to the current market price of ETH, the leverage ratio that traders can use will be greater. For example, when borrowing liquidity is deployed around 999 ETH/USDC, the required collateral is only 1 USDC, which corresponds to a leverage of 1000 times.

Basic Structure of Infinity Pools

Converter

In order to prevent market price fluctuations In order to avoid the impact of liquidation, InfinityPools has built an isolation mechanism called "Swapper", which is the private transaction pool mentioned above. The Tokens in the trading pool are exchanged at a predetermined price, such as converting ETH to USDC at a predetermined price, and vice versa, so that the market price of ETH can no longer affect the liquidation, and there is no risk of liquidation. Once liquidation risk is removed, protocols and traders can theoretically provide unlimited amounts of leverage on any asset.

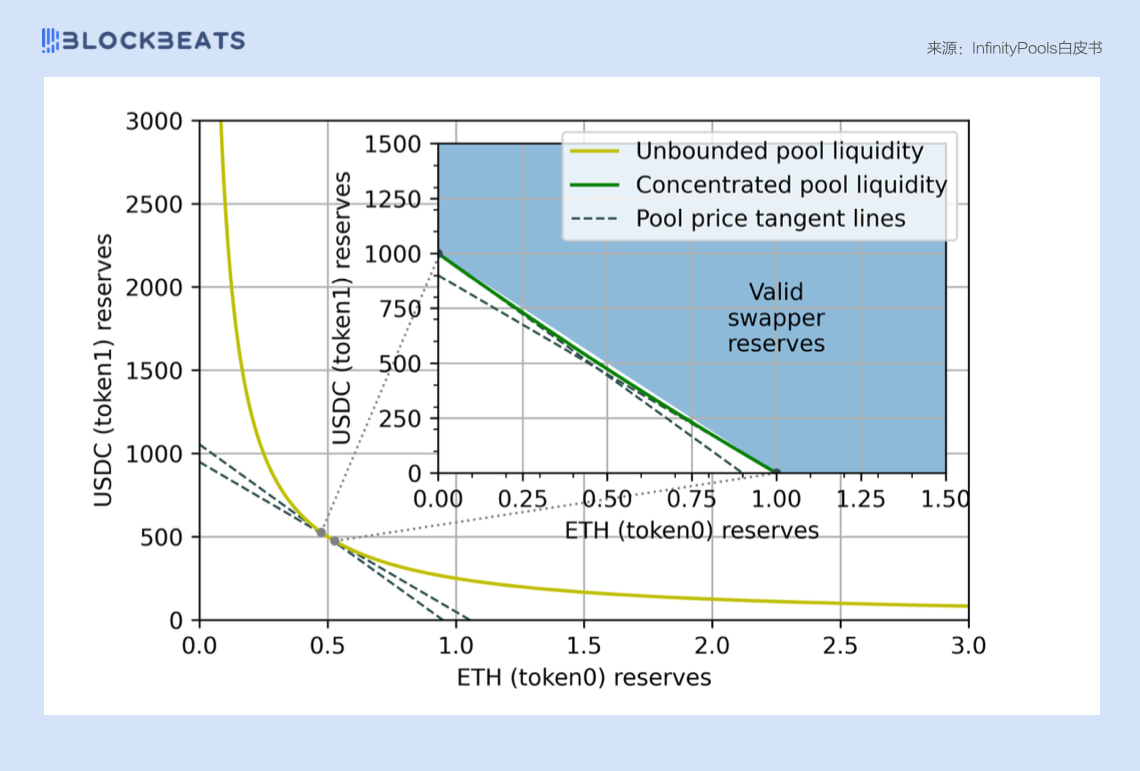

Traders can borrow LP Token at any price and in a wide and narrow liquidity range. Liquidity is aggregated into the exchanger, and the assets in LP Token are called "Reserves". Each converter has a separate predetermined or execution price (Strike Price), the execution price is located at the midpoint of the intervention liquidity (see the calculation formula below), at this price, traders can use the reserve without slippage to execute unlimited Number of Token exchange.

The "Token0" and "Token1" in the formula below represent the liquidity range Two Tokens, when the market price of assets exceeds the borrowed liquidity range, there will be "Max Reserves", that is, the above-mentioned situation where all LP Tokens are one asset. We still use the example just now, regard Token0 as ETH, regard Token1 as USDC, and deploy the borrowed liquidity range around 900 ETH/USDC. When the market price of ETH is higher than 900 USDC, LP Token is all ETH, and then USDC reaches its maximum reserve of 1,000 USDC. When the market price of ETH is lower than 900 ETH/USDC, all LP Token is USDC, and ETH reaches the maximum Reserve 1.11 ETH. At this time, the execution price of this liquidity range is 1000/1.11 = 900 ETH/USDC, and we can also calculate the leverage of this position based on the execution price.

When a trader borrows an LP with a liquidity range Token, that is, when a converter is created, it will always have a reserve fund to recreate the liquidity range. Although LP Token is lent, it is still limited to the reserve size that can be used to rebuild the original liquidity range. Therefore, in the liquidity LP also does not bear any risk within the scope. And the traders of the agreement do not have credit risk, because they only obtain the right to use LP Token, and the reserve of endorsement liquidity is always guaranteed.

As shown in the figure below, the centralized liquidity price curve of the Uniswap V3 model is concave downward , the slope gradually becomes steeper from right to left, while the straight line connecting the two ends of the price curve in any range (ie the execution price adopted by the converter) is always above the curve. That is to say, the reserves contained in the exchanger created based on a specific liquidity range (the blue Valid Swapper Reserves part in the figure) will always have enough funds to rebuild the original liquidity range.

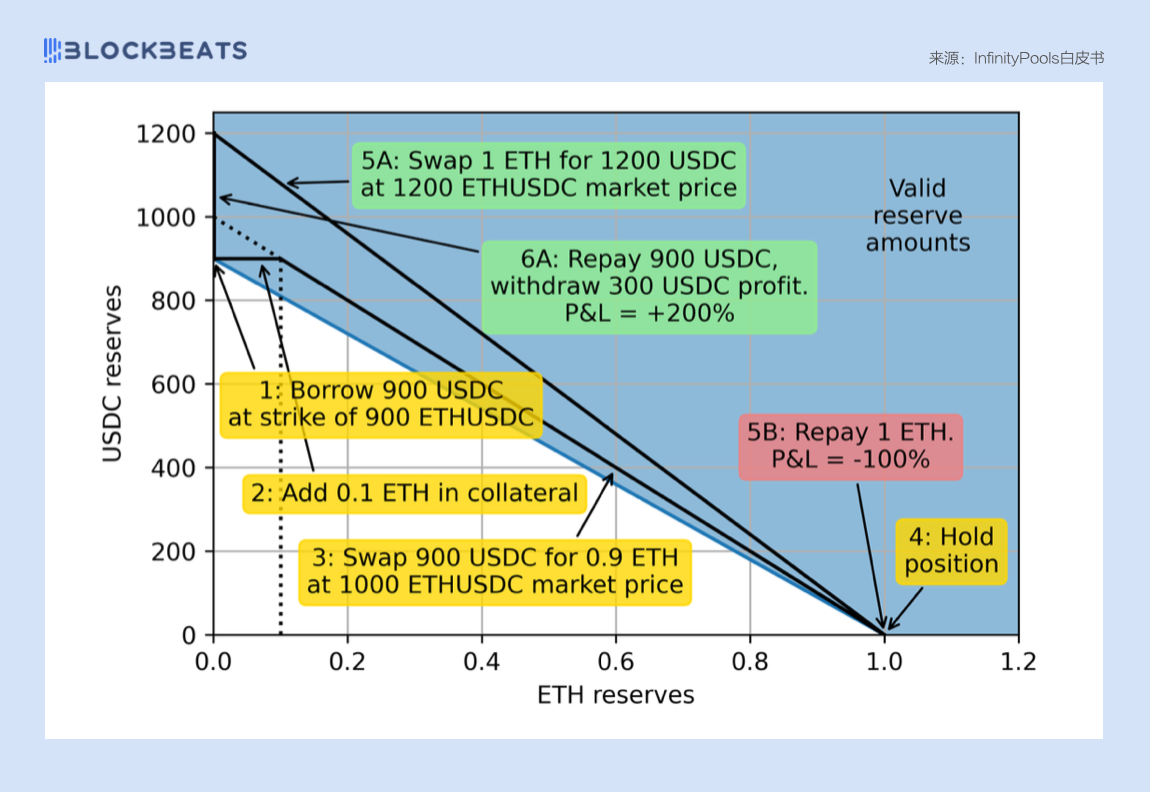

According to the effective reserve range of the converter, we can visualize the operation behavior of the trader. Still using the previous case, in order to obtain the maximum ETH exposure, the trader needs to borrow 900 USDC according to the execution price of the converter 900ETH/USDC, and provide 0.1 ETH as collateral at this price.

After the trader converted 900 USDC to 0.9 ETH at the market price of 1000 ETH/USDC on other DEX, the trader held a total of 1 ETH. At this time, if the trader directly uses 1 ETH to close the position, he will lose 0.1 ETH of his own assets, and if the market price of ETH rises to 1200 ETH/USDC, the trader can exchange ETH back to USDC to close the position and realize 300 USDC by himself profit.

At a higher leverage ratio, the numbers on the horizontal and vertical axes will be proportional Increase. For example, at a leverage ratio of 20 times, the number of USDC on the vertical axis will be doubled, and a trader can borrow 1900 USDC by adding 0.1 ETH as collateral (at this time, the execution price is 950 ETH/USDC).

< p >

The "liquidity futures contracts" borrowed by InfinityPools traders will expire on a continuous basis, and traders can choose to close their positions or replenish them at the current interest rate Holdings that have decayed. This supplement to the position is actually the basic principle of the perpetual contract to keep the position unchanged. In order to recover their position, a long trader must sell the asset at the spot price and buy more futures at the mark price. The difference between the mark price and the spot price is exactly proportional to the funding rate paid by the perpetual long positions. In addition, InfinityPools allows traders to set their own "fee tolerance", continuously closing positions without slippage when the fee rate is above a certain threshold, and refilling the position when it falls below that threshold.

Term Loan & Revolving Loan

InfinityPools mainly has two types of loans, which are divided into Fixed Term Loan and Revolving Loan. Among them, term loans are used for transactions with low leverage (generally 1 to 40 times), and the borrowing cost (fair value rate) is lower. The borrower is required to prepay the interest due during the term of the term loan, and the agreement will pay the funds to the LP according to the maturity schedule. Although the loan has a pre-determined term, the borrower (i.e. the trader) can realize a profit at any time by exchanging the borrowed assets back to the original LP assets.

Revolving loans are more like flash loans, used for shorter reception periods and higher levels of leverage The transaction (generally 40 to 2000 times), this type of loan has more options, but the cost of borrowing is higher. Revolving loans mature on the same schedule as term loans, but the borrower can close the position at any time, so the maturity is effectively immediate. Interest on a revolving loan is not paid upfront, and the borrower can increment the collateral to cover future interest payments and can get back the remaining collateral after the loan is closed.

Floating Fund Pool & LP Income

The floating fund pool (Float pool) is established for LP. When the liquidity range of LP is not lent out, the agreement will keep it in the floating fund pool, and is used to perform spot transactions on common AMMs. Compared with independent liquidity pools, floating pools can achieve lower fee levels while providing higher LP yields.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia