Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Understanding MEV in the Ethereum Dark Forest MEV, or Miner/Maximal Extractable Value, refers to the value that miners can extract from the reordering and inclusion of transactions in a block. In the Ethereum Dark Forest, MEV is a prominent phenomenon where bots and traders compete for advantageous positioning in the transaction inclusion order to maximize their profits. MEV is a complex and ever-evolving concept that has significant implications for the security and integrity of the Ethereum

原文标题:《 【投研导航】一文读懂以太坊黑暗森林中的 MEV|科普向汇总|对 DeFi 影响|机遇 & 挑战 》

原文来源: ChainFeeds

The concept of the Dark Forest Law comes from the Three-Body Problem, which means that if one civilization is discovered, it will inevitably be attacked by other civilizations.

The Ethereum mempool is like a dark forest, closely monitored by programs of unknown origin that can jump start or bid if there is money to be made. This behavior Maximal Extractable Value was a MEV (meV extractable value).

MEV is the total amount of ether that miners can withdraw from trading manipulation. This manipulation can take many forms, but most are through reordering trades within blocks and preempting trades. How does the MEV work? What is MEV-Boost? Why is it so important for today's POS Ethereum? What is the MEV market landscape? What are the opportunities and challenges of MEVs?

Flashbots Strategy Lead, A& T Capital, IOSG, Galaxy Digital, Protocol Labs researchers and other Kols take you to find out.

A selection of information sources for MEV research

Popular science direction

1 MEV Narrative History: From 5 years ago (2022/12/27)

Mevs' roots are as old as cryptocurrencies, but their terminology, frameworks, and tools are still evolving. This article gives an overview of the 5-year history of MEV's pre-birth, post-birth, prevalence and specialization.

1) Before birth: the origin of MEV can be traced back to the study on "fee sniping" of Bitcoin in early 2010. However, if the consensus mechanism is not directly attacked, bitcoin miners can withdraw very little MEV, so Bitcoin is a unique boring MEV research chain; 2) Birth of MEV (2018-2019) : Mevs require two things, scramble and commitment. The launch of DAI in 2017 introduced clearing for DeFi and introduced a large but infrequent number of MEVs (spike MeVs). In mid-to-late 2018, the first wave of AMMs began to build liquidity on their ordering books and the corresponding number of MEVs began to increase. Caused people to pay attention to it; [original in English]

3) Formation of Flashbots (2019-2020) : MEV ship was founded in the middle of 2020, then the founders and managers of Flashbots joined ship, and eventually ship was officially founded and renamed Flashbots; 4) Specialization (2021 to present) : The Flashbots auction was launched in January 2021. Simplicity has driven adoption of MEVs, and today we have a relatively mature supply chain of MEVs, where searchers mine transaction flows for MeVs, and builders take bundles from searchers and build them into blocks. [original in English]

2 In-depth understanding of miner extractable value MEV(2022/08/31)

Ethereum's complexity is made possible by the smart contracts developed at its core. Smart contracts give developers easy access to decentralized finance. But the new system brings new risks, one of which is miners' extractable value (MEV). Cryptocurrency researcher Vaish Puri spoke at length about MEVs in terms of their strategy and how the MEVs will change after the Ethereum merger.

Mevs pose risks to ongoing efforts to decentralize consensus networks, and MEVs complicate decentralized pools because there will still be an entity building and proposing blocks. This will enable them to easily draw MEVs without sharing revenue with the mine pool. PBS addresses this problem by separating the roles of proposer and builder. Instead of generating revenue-maximizing blocks themselves, the block proposer works with a third-party marketplace called a block builder. The block builder generates bundles that contain the block content and proposer fees, and the proposer chooses the bundle with the highest cost. [original in English]

MEV production exploded in 2021, leading to several months of extremely high gas prices. The emergence of a research and development organization called Flashbots led to the creation of a permit-free, transparent, and fair ecosystem for MEV extraction. They introduced MeV-Geth, a proof-of-concept for unlicensed MEV extraction, designed to alleviate network congestion caused by front-end and back-end robots. [original in English]

MEV's three strategies: DEX arbitrage, clearing, and sandwich trading. Sandwich uses the memory pool to scan large DEX transactions. The two main components of the sandwich attack, the AMM and the price slip point, buy assets immediately before the trade is executed and sell them immediately after. To get a risk-free arbitrage. [original in English]

3 To explore the generation and operation mechanism of MEV(2022/10/19)

Introduction: Most people can understand the operation mode of Ethereum transaction from the perspective of users. This paper aims to analyze the concepts of MEV, repeater, block building, Flashbots and so on through the simplest and most frequent token transaction, and to make popular science on the generation process of MEV and its operation mechanism in Ethereum.

How does MEV come about? The AMM creates a slip point on every trade, where every dollar sold of an asset lowers its price, meaning that if I sell a lot of a single asset, the new price of that asset may be lower than the current market price. In this case, it makes sense for MEV searchers to buy assets at the new price and sell them at the market price. But a lot of the time, MEV searchers buy assets before users do, and then sell them to them at a marked price. [original in English]

MEV searchers rely on a specific order of transactions in Ethereum blocks to make a profit. For example, when I sell my assets, MEV searchers need to be the first trade after I buy to arbitrage. In general, most of the profits go to the web participants, not the MEV searchers themselves. But there is an incentive pattern where MEV searchers can directly build a block to gain an advantage over other searchers, which leads to MEVs being licensed and a poor user experience. This is where Flashbots comes in. Flashbots is how MEV searchers bid for slots in block space, and a successful bid can submit a bundle deal, which is then submitted to the block builder and then to the relay station, where the repeater shows all the blocks and bids to the verifier, who picks the block to propose, and after the verifier completes the proposal, The repeater passes everything to the verifier, which then passes it to the network. At this point, the MEV arbitrage is complete. [original in English]

4 The PBS mechanism: How does it affect the Ethereum protocol and MEV ecology?

Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS) Proposer-Builder Separation (PBS)

PBS eases the burden on a Proposer, and a Proposer node does not need to hold the Ethereum complete state. This lowers the barrier to becoming a Proposer and makes the network more decentralised. In the future Dank-Sharding or Sharding will allow block capacity to become larger, and in PBS these burdens are carried by the Builder, so Proposer's degree of centralisation is not affected.

When you give all transaction sequencing rights to Builder, you have to worry about Censorship. There are several censor-resistant designs that include Proposer's own sorted portion of the deal, but the consensus is for a Forward Inclusion List.

Two Slot PBS and Single Slot PBS are two designs of the current PBS architecture, each with its own advantages and disadvantages. Single Slot PBS is simpler but also more centralized, relying on a single Committee member to be online and honest. The Two Slot PBS is more decentralized. It integrates with PoS Fork Choice Rule and relies on multiple committees to increase security. However, the Committee does not need to be online.

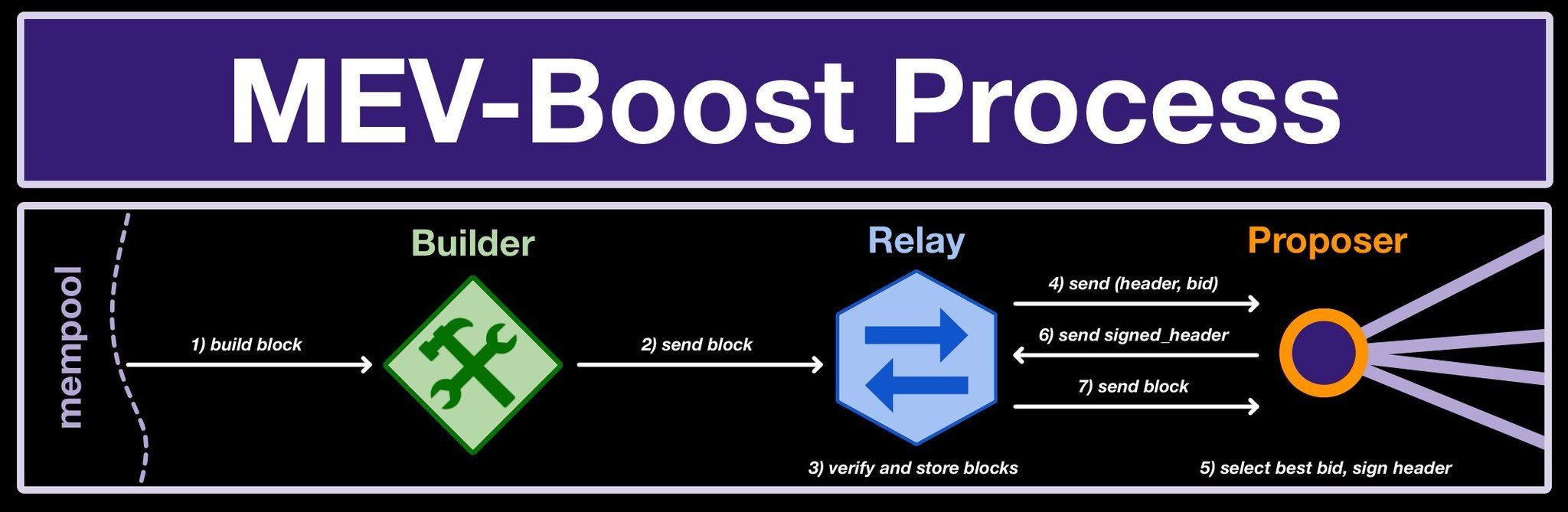

5 Introduces block proposal and MEV-boost processing

What is a block proposer? What is MEV-Boost and why is it so important to Ethereum today? Why do we need long-term solutions and what do they look like? This article provides a brief answer to these questions by introducing block proposal and the general process of MEV-Boost processing blocks.

The purpose of MEV-Boost is to separate the difficulties and knowledge/capital/experience of building blocks from the financial rewards of the proposed blocks. When a proposer is selected for a proposed block in a slot, the return provided by the MEV is shared simply by selecting the highest bid block.

6 Why run "mev-boost"?

As MEVs become more and more important in PoS Ethereum, Flashbots is about to release "mev-boost", allowing any builder to openly compete to make the best blocks. Hasu, head of strategy at Flashbots, explained the benefits of mev-boost for networks as well as for validators, node operators, and pledge pools.

To ensure a high level of data availability, mev-boost introduces a trusted relay between the builder and the verifier that simulates blocks, filters out bad blocks, and manages blocks. Relay activity is publicly auditable, allowing the entire network to monitor its performance. To reduce the risk of censorship, mev-boost allows verifiers to connect to any relay they trust. [original in English]

The more block builders compete to buy block space from the verifier, the more they must bid. As a result, the verifier can get a higher return than using any other method. This difference is even more important for independent validators, who are too small to participate in Phase 1 PBS and do not receive any MEV revenue. mev-boost allows small or independent verifiers to sell their block space to the builder with the best bid. [original in English]

Impact of MEV on DeFi

1 EigenPhi: Influence of MEV on Uniswap

AMM is one of the most relevant components of MEV extraction. How much impact has MEV had on the Uniswap community and its users? Which Uniswap users and liquidity pools are more likely to be involved? EigenPhi researcher playerYixin wrote a report analyzing three MEV robot activities targeting Uniswap V3 mobility pools.

MEV robots, which include arbitrage, sandwich and JIT robots, have drawn at least US $138 million from Uniswap V3 pools between January 1 and October 31, 2022. This represents more than a quarter of the revenue generated by LP swap fees. Arbitrage robots extract the most value from these three types of MEV robots. [original in English]

Revenue: Arbitrage bots have extracted at least $85 million from market price asymmetries involving Uniswap V3 pools. Sandwich bots took at least $47 million from exchange users in the form of slip-point losses. JIT robots have already extracted $6 million from Uniswap V3's interchange fee revenue. Robots accounted for 25% of LP's total revenue. However, there is no apparent conflict of interest between arbitrage bots, sandwich bots, and LP. [original in English]

Pools: More than 80% of sandwich Bot profits come from the top 10 pools sorted by volume. However, only 20 percent of sandwich activity took place in these pools. JIT bots seem to be more focused on the top 10 pools, ranked by transaction volume, where 84% of profits come from and where 56% of JIT bot activity takes place. [original in English]

2EigenPhi: An exploration of the influence of MEV activities on Curve

EigenPhi, a MEV research tool, explored the activities of MEV arbitrage and MEV sandwich attack on Curve, including profiles of benefits, costs, frequency, trading volume, participants, etc., hoping to enlighten stakeholders on protocol design and trading decisions.

1) Income: The arbitrage robot has earned more than $10 million from Curve capital pool transactions, and the total number of arbitrage transactions is 40,419. The Sandwich attack bot drew $980,000 in revenue from the Curve money pool trade. The single transaction income of the sandwich attacking robot was higher than that of the arbitrage robot, but the monthly total income of the arbitrage robot was higher than that of the sandwich robot.

2) Trading volume: the trading volume of MEV accounts for 20% of the total trading volume, and the median trading volume of sandwich attack exceeds the arbitrage trading volume by one order of magnitude; [original in English]

3) Frequency: the activity frequency of sandwich attacking robot is lower than that of arbitrage robot, and the occurrence of arbitrage trading opportunities is strongly correlated with market price fluctuations;

4) Profit: the maximum profit of sandwich attack robot is two orders of magnitude smaller than that of arbitrage robot, and not all MEV robots can generate positive profit;

5) Cost: The arbitrage cost is relatively stable and low, and the average cost of sandwich attack robot is high;

6) Participants: The number of victims who have suffered losses has gradually increased since June, with an increase rate of 300%; [original in English]

7) Capital pool: The capital pool including USDT, WBTC and WETH provides the most arbitrage opportunities, and the pool with the largest trading volume is the stablecoin pool; 8) There is a positive correlation between the total profit and the total number of activities of the arbitrage robot contract, and the common arbitrage mode is spatial arbitrage; 9) Only 19 Sandwich attack bot contracts have attacked the Curve pool. The most profitable Sandwich attack bot took just two trades to make a total profit of over $46,000. The Sandwich attack was more challenging to execute in the Curve pool than Uniswap. [original in English]

3[English] MEV maximization strategy: Potential impact of Ethereum Shanghai Upgrade on LSD

The Ethereum Shanghai upgrade will enable verifiers to extract pledged ETH on the Ethereum main network, which will lead to a significant increase in the volume of liquid pledged derivatives on Ethereum, creating more MEV opportunities. EigenPhi discusses the potential impact of LSD and the maximization strategy of MEV in terms of revenue, market size and future expectations.

Between May 2022 and February 2023, total MEVs involving LSD totaled more than $4.84 million, most of which came from arbitrage. The rise in the frequency of carry trades and the fall in average carry revenues suggest that markets are becoming more efficient. In addition, the revenue-cost ratio decreased in all three categories of MEVs, indicating increased competition in the LSD MEV market. The increasing size of the LSD MEV market, but the decreasing benefit-cost ratio, indicates that participants need to continuously improve their strategies to remain competitive. [original in English]

Future Opportunities for LSD MEVs:

1) In the short term, the Shanghai upgrade allows users to withdraw ETH, which may cause a sharp change in ETH price in the market and bring many arbitrage and liquidation options. Therefore, users planning to sell ETH in bulk in the DeFi market are advised to be prepared against sandwich attacks;

2) In the long run, the market size of LSD MEVs will expand further, and it is predicted that LSD will replace some of WETH's liquidity on Ethereum;

3) Most of the LSD rewards come from the MEV rewards of the market, and higher MEV rewards will also lead to higher LSD rewards, creating an increase in LSD price. Some new trading strategies will also emerge. [original in English]

Research report

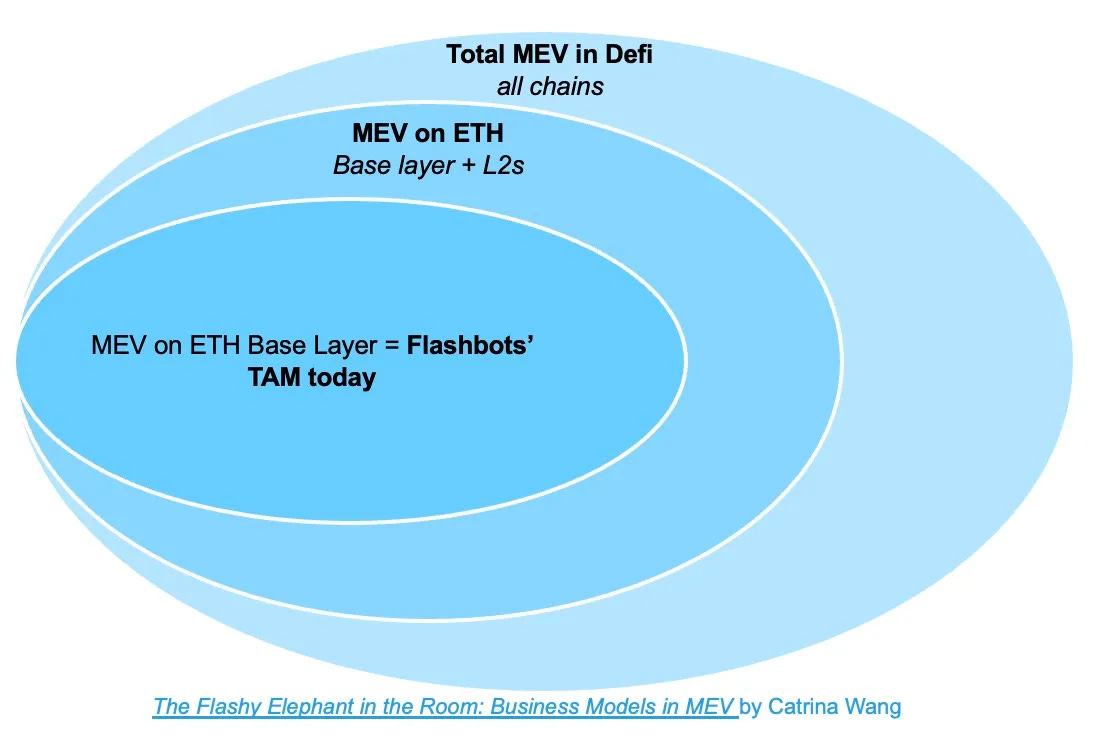

1【 English 】 Discussion on MEV business Model: The Way of Flashbots commercialization

Catrina Wang, a researcher at Protocol Labs, discussed the current development status and future trends of the MEV market. She also took Flashbots as an example to analyze its current competitive advantages in the MEV field and imagined several possible monetization strategies.

Mevs are a promising market, but whether Flashbots can maintain its market leadership depends on three factors: 1.Flashbots' current potential market is being squeezed by the upcoming ETH native MEV features and L2 Rollups; 2. 2.MEV products are often not sticky, and Flashbots is constantly giving up its competitive advantage for the public good; 3. Lots of new entrants and alternative solutions to MEVs. [original in English]

Summary prediction for the future of MEV: 1.Flashbots will tokify SUAVE and monetize it through brand equity; 2. 2.SUAVE will play an important role in cross-chain MEVs; 3. Surge of cross-chain MEVs; 4.EIP 4337 will create a new class of MEV actors; 5. MEV startups will seek monetization from Private Order Flow; 6. Mevs could be one of the few monetization levers for wallets; 7. The equilibrium price of the block space will appear. [original in English]

2 [English] MEV Elastic Framework Exploration: How to make Ethereum more MEV resilient?

Since the rise of DeFi, MEVs have been one of the major threats to blockchain security and equity. Ethereum researcher Davide Crapis provided an analysis of the current state of the MEV ecosystem and ongoing solutions, and presented a general framework for MEV resilience that can be used to evaluate any mechanisms designed to make Ethereum more MEV resilient.

If the blockchain is designed in a way that mitigates the adverse effects of MEVs, including the impact of MEV-induced rewards on probator incentives, the impact of losses due to MEV extraction on honest users, and the attractiveness of MEV extraction benefits to attack users. To do this, we need to do three things:

1) Infrastructure that can effectively extract MEVs;

2) Capture most protocols for extracting MEVs;

3) Captured MEV allocation rules are encoded into the capture protocol. [original in English]

Solution:

1) Limit value loss for users at the transaction stage: three types of solutions currently under development are CowSwap which restricts extraction at the application level, mempool which avoids extraction through full encryption, and rebate mechanism which indirectly restricts extraction through more expressive transactions;

2) Increasing competition between searchers and builders to limit MEV losses: the more competitive the market, the higher the percentage of revenue that needs to be passed down (i.e. extracted MEVs). By increasing competition we can further reduce MEV losses, for example by developing open source strategies for building algorithms for each searcher category and block; [original in English]

3) Adjusting proposer incentives through PBS and reallocation: MEVs alter proposer incentives and introduce risk and inefficiency. And there is a trunk trust problem in the current setup.

4) Avoid exclusive contracts and supply chain segmentation problems: Exclusive order agreements and lack of untrusted interfaces create exclusive contracts and supply chain segmentation problems. A broader solution that is currently being investigated is decentralized block building. [original in English]

3 The Double-Edged Sword of MEV: How to deal with its negative Effects?

Mevs pose a huge threat to blockchain technology and decentralization. Some forms of MEV can make the user experience worse, and more extreme forms of MEV can rearrange blocks, cause network congestion, and drive up Gas prices. But are MEVs all bad? What are the solutions to avoid its negative effects?

Mevs are a double-edged sword. Beneficial MEVs:

1) DEX arbitrage: Searchers scramble to act on price differences between Dexes. The result is that these price differences are minimized;

2) Liquidation: MEV is the main method of DeFi loan liquidation, where searchers process blockchain data to liquidate debt positions.

Harmful MEVs:

1) Frontrunning in a broad sense;

2) Back-running;

3) Sandwich attack;

4) Time-bandit attack.

The negative side effects of MEVs include poor user experience, high Gas bills, and consensus attacks. Its solutions include Chainlink's Fair Sorting service (FSS), private mining pools, and Flashbots. Mevs are not going away anytime soon, a censorship resistant framework is being proposed to help mitigate MEV exploitation on PoS ETH, the Block proposer/Builder Separation (PBS) scheme, but it is currently just an idea and has not yet been implemented on Ethereum.

4 The Power Machine behind Ethereum: MEV and PBS

Introduction: This paper shows the role of MEV robots and Flashbots in Ethereum from the perspective of underlying principles. The impact of PBS architecture on subsequent crypto ecology and the evolution prediction of each role in the future.

There is a special feature in the block building client that allows the builder to exclude certain addresses from the block by setting up a blacklist. This means that the future builder has the ability to review transactions, and if some user initiates a transaction that does not meet its specifications, his transaction will be in pending state and never reach the real network.

As more users and project parties become involved, the impact of this type of review will be mitigated by future block building becoming more decentralized. However, the potential harm caused by the centralization of block building is still significant. For example: enforcer block, enterprise block, falsifying history or destroying reality, etc.

The subsequent rollout of the suave architecture and the influx of participants will mitigate the effects of private order flow abuse and builder centralization, provided there is sufficient free market competition and protection for pioneering innovators. A truly open and fair mev marketplace should allow all searchers and builders to participate, with users free to choose where their transactions go. Searchers and builders are able to compete and give back to the protocol layer users to the greatest extent possible. Protocols use order flow to maximize efficiency and block resources.

5【 English 】 Through the Dark Forest: Demystifying the MEV market landscape

Encryption researcher Ali has studied about 100 MeV-related projects to map the MEV market landscape into three general categories: MEV infrastructure, MEV Solutions, and MEV applications. Based on this, each category is further divided into sub-categories and described in detail.

The MEV infrastructure is anchored by "verifier and pledge" participants. The advent of MPSVs (MEV Profit Sharing Validators) has changed the market, with many validators offering MEV rewards in addition to traditional pledge revenue. At the core of this subclass are block builders and relay participants. In the block builder category, there is the Skip Protocol (Cosmos), which provides sovereign MEV infrastructure, and the MPSV project Jito, which has its own liquidity pledge derivative jSOL. We expect that the blockchain ecosystem will continue to develop its unique vendors of block builders. Where economies of scale are increasing, category leaders may emerge. The need for cross-chain MEV solutions may lead to collaboration with existing block builders. [original in English]

MEV solutions include a range of tools and protocols designed to help the entire ecosystem extract, prevent, or democratize MEVs. One of the most notable is MEV cross-chain coordination, led by Skip Protocol, Suave, and Anoma, among others. The increasing prevalence of bridging, composability, and modularity paves the way for cross-chain and inter-chain MEV solutions. The Shared Collator section focuses on L2 scaling solutions that mitigate MEV-related risks by promoting fair and consistent transaction ordering, thereby limiting jump start and robot arbitrage. Other emerging areas include NFT-related MEV solutions, such as Pikapool, designed to create NFT-specific memory pools and reduce any negative externalities of MEVs. The order flow auction portion is designed to return the value created by the user through their order to the user. Finally, we think the market for gaming MEV tools will start to grow. [original in English]

The application layer includes end-user products across the MEV ecosystem. Many DEXs and aggregators emphasize MEV prevention, and other markets and trading platforms often encounter MEV arbitrage and clearing, which can partly explain how MEVs penetrate (indirectly or directly) into the application layer. On the other hand, there are niche specific markets regarding block space and order flow payments, such as Alkimiya and DFLOW. We expect two important categories to emerge in this tier: the NFT and the gaming market, which provide MEV protection, and the MEV Wallet. [original in English]

Current situation, opportunities and future prospects

1 [English] "Dark Forest" journey Notes: Brief analysis of MEV concept, current state and market characteristics

Introduction: This post is a summary of the Bell Curve hosted by Hasu, Head of Strategy at Flashbots, and Mippo, Blockworks. The main contents include what MEVs are, the status quo of MEVs in L1 and modularization, the role of delay, and the characteristics of Solana ecology and Cosmos Ecology MEVs.

1) The perfect MEV solution should include the following characteristics: avoid centralization, minimize undesirable MEVs, return MEVs to the protocol, be competitive and private, and redistribute MEVs to users; 2) The MEV of L1 is mainly extracted by verifiers, MEV searchers and other participants, while the MEV in the modular world is included in the executive level, and when L2 switches to a decentralized sorter, it will face the problem of low MEV extraction efficiency. [original in English]

3) Trading firms require microsecond latency and may become block builders. If we minimize the impact of delay, competition will shift to price; 4) Sorting transactions in the order they are received is fairer; 5) The MEV of Solana ecology is too centralized and has low delay, so the verifier has great advantages, but it is disadvantageous to users. Cosmos Eco-MEVs are interesting and very innovative, with Osmosis and Skip Protocol capturing MEVs through block building and searching, and protorev modules. [original in English]

2 A& T Capital: Ethereum MEV extraction mechanism status, problems and improvements

In this article, MEV is defined as the economic benefit to the entity that designed the sequence by executing N transactions in a specific order. Liam, an analyst at AnT Capital, analyzed how existing solutions prevent harmful MEV extraction and equitably distribute favorable and neutral MEVs by analyzing stakeholders of MEVs and the flow of MEVs under the MEV-Boost system, and suggested directions for improvement.

After the merger of Ethereum, MEV extraction and distribution are dominated by MeV-Boost system proposed by Flashbots. This goes to searchers, Block builders, Block proposers and the Ethereum network itself. The transaction to extract the MEV is executed to generate revenue for the searcher who created the transaction at the cost of the Gas Fee paid by the searcher; Part of the Gas Fee is burned according to IP-1559, and the other part flows to the block builder in the form of a Tip; The block builder passes most of the tips to the block proposer in the form of MEV Rewards.

From the perspective of the consequences MEV brings to the whole system, it can be divided into three categories: beneficial, neutral and harmful. How to avoid harmful MEV extraction and distribute favorable and neutral MEV profits is the core problem to be solved. The MEV profit distribution scheme of MEV-Boost system does not consider the interests of users. As the role of the user creating the MEV withdrawal opportunity, the protection of their reasonable interests is only the most basic. They should not only protect their transactions from being spurned, but also return a portion of the MEV profits.

Existing private RPC solutions are based on the assumption of trust, user transactions can still be compromised, preempted, or even censored, and the monopoly of some block builders over private order flows can make MEV extraction more opaque and centralized. To solve the "jump start" problem, encryption should be used. Based on "Encryption-Sort-Decryption-execute", the user's transaction is encrypted locally, the sorting consensus is completed without anyone reading the transaction content, then the content is decrypted, and finally the transaction is executed according to the agreed ordering.

3 IOSG Weekly: A New Decade of MEV scale Growth

Mevs have had their fair share of controversies over the past few years, but they haven't been hindered by their rapid expansion. Jiawei, a member of IOSG Ventures, will explain how SUAVE solves the problems of EOF and cross-domain MEV, sort out the development trend and narrative logic of blockchain, and put forward the outlook for the new decade of MEV.

SUAVE is an EVM-compatible blockchain proposed by Flashbots. As a Mempool and block builder network common to all blockchains, as well as a decentralized ordering layer, SUAVE aims to solve the builder centralization problem, namely the EOF and cross-domain MEV problems. The preference environment of SUAVE corresponds to cross-domain MEV, which makes the advantage caused by poor information no longer exist. The executive market corresponds to EOF, and puts the preference in an open market, so that all the executors can realize the user's preference through bidding. Finally, a network of builders collaborates to build the complete block.

Through the development trend and narrative logic of blockchain, we can see the gradual evolution of infrastructure from a centralized general-purpose layer to a refined professional layer. The increased degree of functional modularity and specialization makes it possible to "make the whole greater than the sum of the parts". For example, we can achieve better composability on the common settlement layer; More MEVs can be represented and captured at the generic sorting layer.

Existing MEV solutions cover a variety of aspects, with the basic topics surrounding "minimizing/preventing MEVs" and "democratizing MEV/MEV benefits redistribution". The inherent nature of MEVs as blockchains represents a tradeoff point in the current "triangle of Impossibility," which may extend to a "fourth corner" in the implementation of SUAVE. The trend we can see from PBS to SUAVE is to constantly introduce the diversity of competition and ensure that the conditions of competition are balanced. The community is always moving towards the goal of decentralization. We describe the new decade of MEV: competition, not monopoly; Sharing, not sharing; Co-rule, not dictatorship.

4EigenPhi: Opportunities and challenges for understanding MEV at the micro level

With MEVs being the new blue ocean of financial engineering and quantification for individuals and regulators, EigenPhi is taking a micro-level look at the 2022 MEV market and revealing key trends and new opportunities based on data analysis, hoping to draw attention to the value and risk of existing liquidity data.

After nearly two years of exploration, we found that:

1) Liquidity is a scarce resource and needs to be more proactive in tracking market fluctuations and adjusting liquidity ranges;

2) Arbitrageurs are good at exploiting and finding information differences in liquidity to earn income, while attackers create differences to gain value;

3) There are advantages and disadvantages of liquidity, and distinguishing liquidity value will provide another important reference index for asset valuation;

4) Due to flash lending and unlicensed lending platforms, the cost of obtaining liquidity in DeFi is reduced in terms of time and amount of capital. [original in English]

2022 MEV market:

1) Arbitrage robots trade more frequently than sandwich robots and clearing robots. Compared with traditional arbitrage opportunities, clearing opportunities are more dependent on intense market fluctuations;

2) Mainstream MEVs generated at least $307 million in revenue in 2022, with arbitrage robots accounting for more than 47.5%;

3) The most profitable MEV robot made a total profit of $9.2 million from carry trades, but nearly half of the liquidators reported losses; [original in English]

4) After the merger of Ethereum PoS, although the off-chain auction market changes in the block space affected the MEV allocation, the oligopoly pattern remained unchanged;

5) Sandwich robots participated in $287 billion of MEVs in 2022, with Uniswap V3 being the most popular for arbitrage bots and sandwich bots;

6) The MEV opportunity on BSC is more cost-effective than Ethereum, and its arbitrage bots have a lower average cost-to-income ratio than Ethereum, so the total profit is relatively large. [original in English]

Most people have a negative impression of MEVs, and they could threaten the security and decentralization of blockchain itself. However, from the perspective of DeFi protocol, MEV robots can also provide some value. The most common arbitrage robot's calculation of the price deviation of the liquidity pool enhances the efficiency of market price discovery. Clearing robots monitor the health of mortgage ratios. On the other hand, the interaction between MEV robots and other participants of the DeFi protocol has also become more complex and important, and the interchange users will not necessarily bear more slip point losses due to the existence of sandwich robots. [original in English]

5 [English] MEV Research Report: MeV-Boost Architecture, Centralization issues, and Potential Solutions

Introduction: The report was written by Christine Kim, a researcher at Galaxy Digital, This includes an overview of the MEV-Boost architecture and its key stakeholders, a discussion of relay censorship and builder centralization concerns raised by MEV-Boost, and potential solutions being discussed by the Ethereum core developers and the Flashbots team to address this issue.

Mev-boost has implemented an earlier, more decentralized MEV supply chain where several different entities can participate as searchers, builders, validators, and Repeaters. Since the merger, Ethereum MEV data suggests that competition among builders has intensified, with a diversity of unknowable and censor-resistant relays slowly undermining the dominance of Flashbots relays. [original in English]

Core Ethereum developers and researchers are working on how to remove the trusted relay Settings required by connection builders and verifiers, but several issues related to the implementation of PBS remain unresolved, and core Ethereum developers may have limited consideration for several other major upgrades to the Ethereum protocol, including proto-danksharding. So the Flashbots team and other new entities are working to further optimize relay technology to improve resilience and efficiency. [original in English]

While concerns around builder-centralization have not materialized, there are several solutions to ease them, such as SUAVE and auctions of some blocks through smart contract protocols such as EigenLayer. In addition, the open source of the MEV infrastructure will diversify the number of stakeholders involved, which may increase the amount of innovation in the future, and DeFi on Ethereum will provide more opportunities for fair trading than traditional finance. [original in English]

6[English long tweet] Analysis of Ethereum MEV related statistics

MEV-Boost payments hit a record high yesterday, totalling 7,691 ETH, almost double the previous record high of 3,928 ETH during the FTX crash. Flashbots product lead bertcmiller analyzed Ethereum MEV statistics, including historical MEVs, and recent market share changes in Builder and Relay market shares.

An interesting thing is that we have a big MEV day once a year: 5th June 2021:6397 ETH; 13 June 2022:6313 ETH; 11 March 2023: Payment of ETH 7691 to the mev-boost proposer. Looking at it another way, about 95% of the blocks in the last 24 hours have been MEV-Boost blocks. [original in English]

Builder market share yesterday and last week: builder0x69 soared, especially during high MEV periods; Flashbots /rsync is very stable; beaverbuild and bloXroute Labs halved; Manta dropped out of the top 10 entirely. builder0x69 appears to be subsidizing the median blocks and profiting from the most profitable blocks, and given the number of ultra-high MEV blocks, their proliferation is well documented. [original in English]

Relay market share: ultra sound money and GnosisDAO's Repeaters have collectively surged about 10% in the last 24 hours, seemingly at the expense of BloxRoute and Blocknative. [original in English]

Original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia