Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

What are the features and advantages of Blur's new lending agreement Blend?

Original title: "In-depth Analysis of Blur's New Lending Protocol Blend"

Original author: Capitalismlab

Blur has recently launched Blend with Paradigm A P2P NFT lending agreement, and the function of buying NFT with loans based on it.

What are the core features of Blend? What are the product advantages? And how? This article will give you an in-depth understanding of Blend, a next-generation NFT lending protocol.

The core features of Blend are:

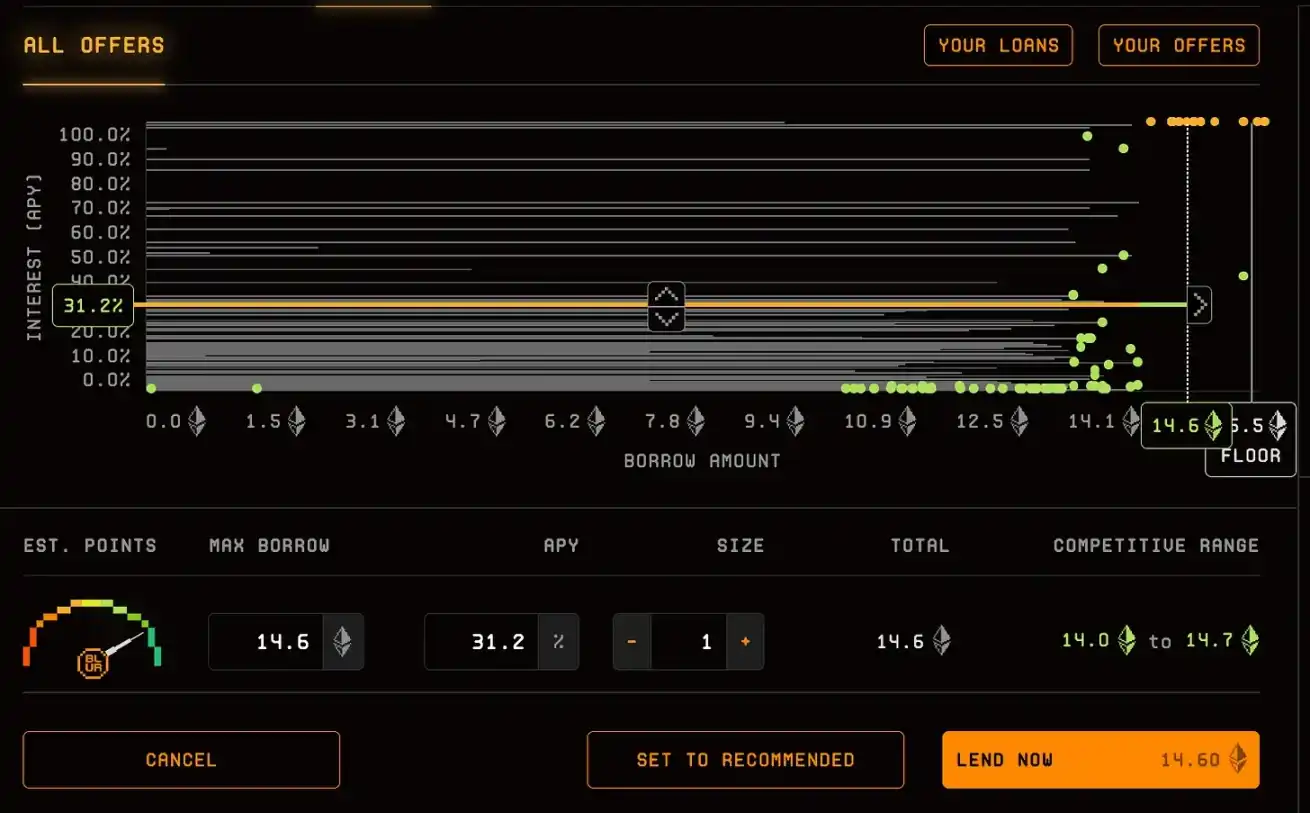

Peer-to-peer, perpetual lending, no expiration date, no need for oracles. The lender decides the loanable amount and APY to issue an offer. The borrower chooses the offer and the lender withdraws. The borrower needs to repay the loan within 30 hours or borrow new ones. Otherwise, the liquidated borrower can repay at any time to support the purchase first and pay later, that is, down payment + loan to buy NFT

Product Advantages

< br>

The core advantage of Blend is to unify non-essential elements, reduce the complexity of the system, realize the flexible migration of loan relationships within the system, price risks and benefits through market games, and maximize user needs. Yes, in a sense, Blend is quite like Qin Shihuang's "cars on the same track, books on the same text".

Compared with traditional point-to-point models such as X2Y2, Blend unifies the three elements of borrowing, mortgage rate, interest rate, and mid-term period, into a sustainable and flexible model, which greatly improves To solve the liquidity problem of the lender, Blend unifies the exit and liquidation of the lender. After all, the essence of liquidation is that no one is willing to take over the project.

< /p>

Blend has fixed terms (mortgage rate and interest rate) on the surface. In fact, due to the extremely flexible exit mechanism, the terms in effect will basically follow the market average . Because if the terms are significantly worse than the market level, the borrower has the motivation to repay the loan and then borrow other offers. If the terms are significantly better than the market level, the lender will have the motivation to withdraw and issue a new offer to lend money to others.

For borrowers, the higher the mortgage rate, the better, the lower the interest rate, the better, and the more flexible the term, the better. Regarding the first two points, on the one hand, the effective terms will follow the market level as mentioned above, and on the other hand, Blend operates by allocating incentive points to lenders. The higher the loanable amount and the lower the interest rate, the more points will be awarded. For the third point, Blend uses the setting of perpetual + repayment at any time, which realizes the complete flexibility of the borrower's term.

For the lender, the mortgage rate and interest rate also follow the market level and Blur incentives, and there is no risk of losing money. The term is also very flexible, you can exit if you want, which is equivalent to having the self-defined advantages of the peer-to-peer model on the one hand, and enjoying the liquidity advantage close to the peer-to-pool model, and you can also formulate your own risk control standards to exit flexibly.

Loan to buy NFT

Buying an NFT with a loan is similar to buying a house with a loan. It is equivalent to initiating a mortgage loan while buying an NFT, so that you can get the house after paying the down payment, which is the so-called improvement of capital efficiency. Although this is no different from flash loan ETH mortgage NFT to borrow ETH part of the repayment, but the integration of this function at the first launch will help bring a large number of new users to Blend to help it grow. In addition, this also reflects the possibility of Blur integrating a unified ecosystem to achieve 1+ 1>2 effect.

Other

In addition In Paradigm’s design document, when the lender exits, the Dutch auction will be initiated, which means that the interest rate will gradually increase from 0% to 1000% over time, and the new lender in the middle can offer at any time. If no one accepts it at 1000%, the borrower will be liquidated , give the mortgaged NFT to the current lender.

However, on Blur’s page, we can see that the borrower needs to repay the loan or borrow new money to repay the old one. There are two variables of interest rate, while only one variable of interest rate is considered in the design of Paragidm. In fact, there is not much difference between the two, both of which strive to transition to the new terms that are most beneficial to the borrower, but one does not require the borrower to operate and the other needs it.

However, it is worth noting that Blend has not yet given too much power to $Blur. $Blur has the governance right to set various parameters and after half a year The power to turn on the fee switch, but everything is still uncertain.

Summary

Blend Unify the non-essential elements in the traditional peer-to-peer lending model, realize the efficiency improvement of "cars on the same track, books on the same text", and fully integrate with the Blur transaction module, which has greatly improved the product level and token empowerment more common.

Original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia