Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Correct approach to participating in Binance IEOs based on valuation logic and historical data.

MAV IEO has attracted a new batch of losing investors, and there have been many cases of being trapped after the opening of Binance Launchpad/Launchpool recently. Although there has been a recent surge, many people have not yet successfully recovered their losses.

This article will help you understand the basic valuation logic of various projects, avoid blindly rushing in at the highest point, and review and compare the historical performance of Launchpool and Launchpad, sharply evaluate the similarities and differences between these two platforms and their speculative strategies.

A. Valuation Logic

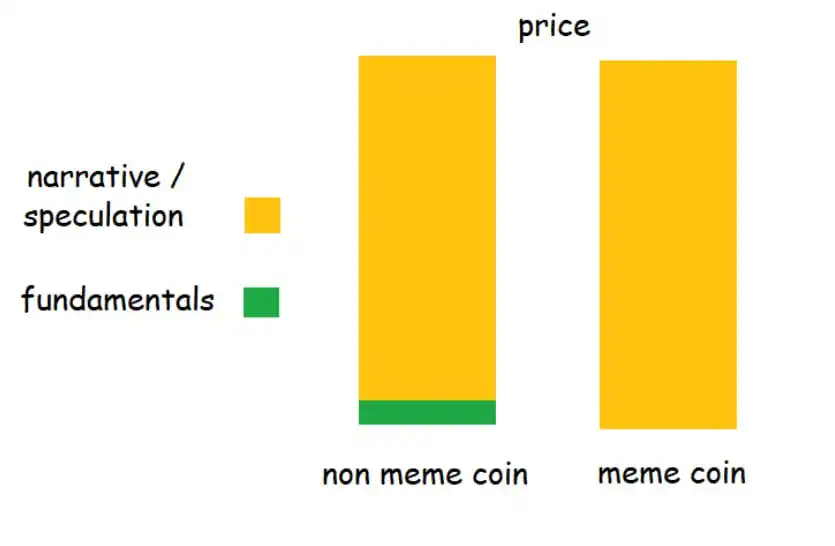

If it is not a "meaningless governance token" or a memecoin, theoretically it can be compared on a relatively large scale by giving benefits to token holders. However, cryptocurrency is a game of attention after all, and the so-called fundamentals are too small in the narrative, so valuation is generally based on benchmarking within similar projects.

For example, MAV belongs to the DEX track in the DeFi category. The common indicator for DeFi is TVL, which is commonly used to evaluate the scale, as well as the total fee income and protocol income, which are less commonly used to evaluate profitability. Specifically for DEX, there is an additional indicator of trading volume (Vol) to evaluate business scale.

As for the token itself, there are two indicators: the current market capitalization (mcap) and the fully diluted valuation (FDV), which correspond to short-term and long-term liquidity, respectively.

See the valuation benchmark chart made by @BiteyeCN, which uses TVL or revenue as business evaluation indicators, and provides valuation opinions under mcap/FDV respectively.

Of course, there are often some tricks behind the data. For example, the problem with using one-week transaction fees to evaluate MAV is that MAV has a clear airdrop and is listed on Binance, so there are naturally many people who manipulate the trading volume, which inevitably leads to an overestimation.

Using more refined logic and common sense to judge is also a good method. The price of MAV at $0.5+ will lead to its FDV being close to Pancake. Even if MAV has a closer relationship with Binance, it is still not as close as Cake. Therefore, it is not very realistic to expect Binance to support the price to exceed $0.5.

Previously, the DEX Hashflow, which also launched through Binance Launchpool, currently has an FDV of around 400M, corresponding to an MAV price of less than $0.2.

So if someone really wants to invest based on "trusting Binance's vision", $0.5 is obviously beyond the scope that the launchpool can support. Currently, the market price of around 0.45 is already a relatively high position.

DeFi projects are relatively easy to evaluate due to their practical earning capabilities and application focus. On the other hand, user activity data for public chain projects is often inflated by fake users, making it less reliable as a reference. Only TVL data can be used as a rough indicator. Therefore, compared to data, public chain projects seem to value background more, which is one of the reasons why VCs dominate in this field. Projects with good backgrounds seem to receive funding without much scrutiny, sometimes up to 10 billion.

See our valuation of ARB that we talked about back then, based on TVL and ecosystem, giving a valuation of 2 times OP FDV. However, after ARB issued coins, there was a huge price difference and it suffered a major setback. Instead, after a period of time, with the continuous decline in OP prices, ARB successfully achieved 2 times OP FDV.

As for projects like EDU/HOOK that have no well-known counterparts in the same industry, they are born as leaders in their respective fields and cannot be compared to anything else. The advantage is that the sky is the limit for their potential, but the downside is that everyone starts from scratch.

B. FDV is not just a number

FDV = Total Circulation of Tokens * Token Price.

When evaluating projects, market capitalization (mcap) is often preferred over fully diluted valuation (FDV) for comparison. However, this is mostly because newly issued projects with high popularity have low circulation, making it advantageous to use mcap for comparison. But FDV is not just a number.

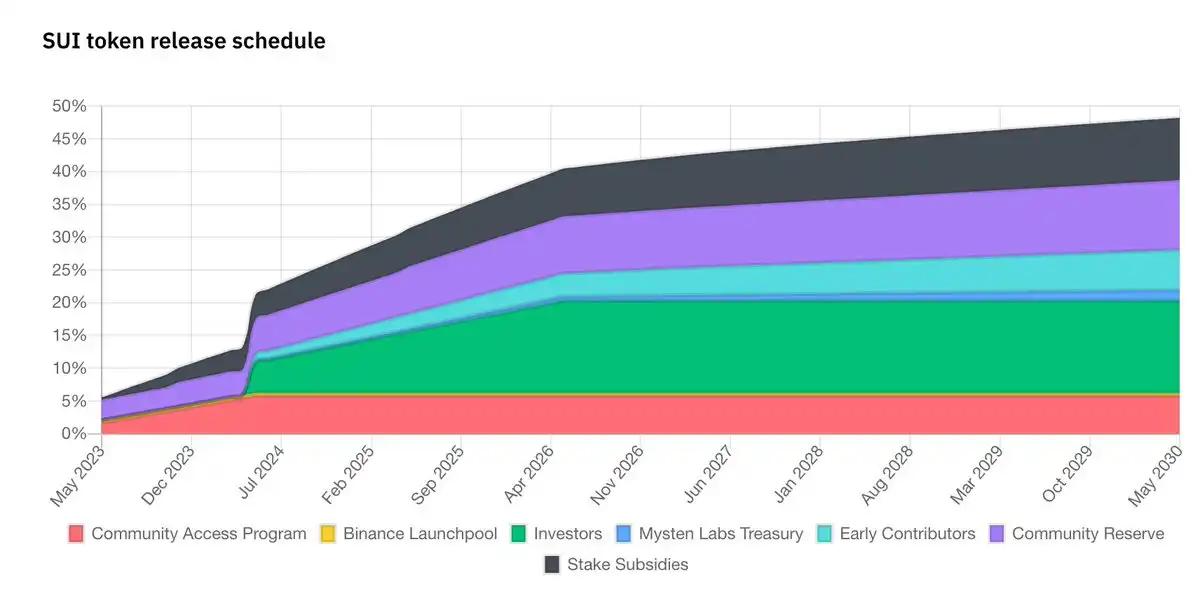

Using the example of SUI, which experienced a price decline since its launch, despite being listed on OKX/Bybit/Bitget and receiving a boost from a 40M token airdrop on Binance Launchpool.

Recently, it was exposed that the project party was secretly unlocking and selling coins ahead of time, claiming to have flexible tokenomics. This is the painful process of mcap gradually approaching FDV, and the increment will become selling pressure.

However, even if SUI follows the token unlocking plan honestly, its growth rate is still very fast. Due to benchmarking and short-term speculation, SUI had a FDV of over 10B at the opening, while the mcap was less than 1B, which could barely be supported by market enthusiasm. However, in the long run, if the fundamentals do not improve much, it is natural for the price to decrease as the FDV of 10B slowly turns into mcap.

C. Launchpool & Launchpad Differences and Speculation

Many people refer to MAV as the XX phase of the Launchpad project in the encryption industry, but in fact it is part of the Launchpool project. What is the difference between Launchpool and Launchpad? Launchpool is free, while Launchpad requires BNB holders to pay for it, which implies Binance's attitude towards it.

Especially for projects launched through Binance, it can be said that the implicit support of Launchpad projects is one level stronger than Launchpool.

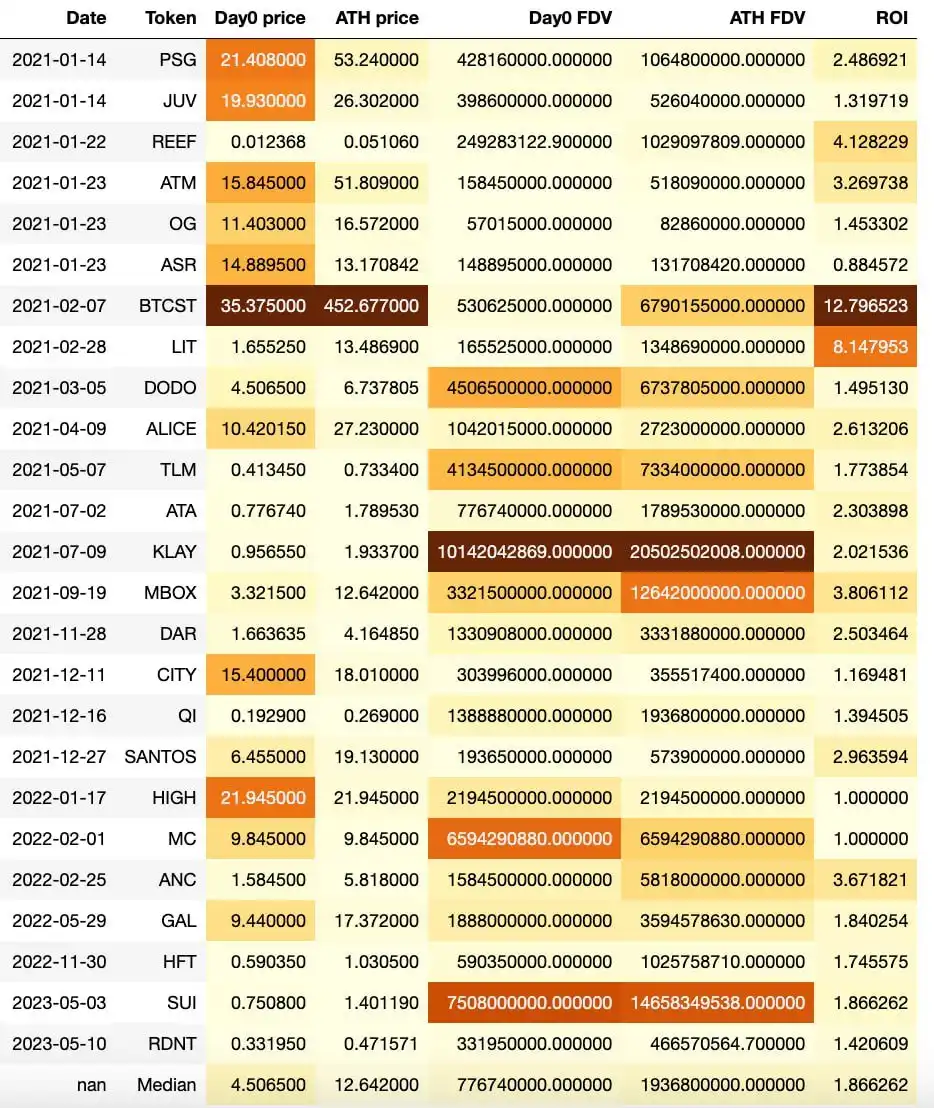

Previously, as mentioned in the tweet below, we have already discussed the overall return data of Launchpad.

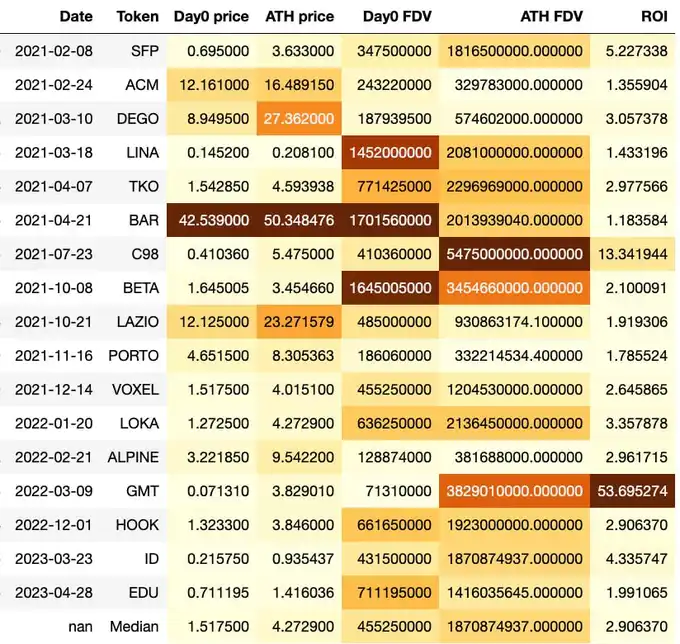

We will analyze from the perspective of opening account users this time, analyzing the opening price (first-day average price), historical highest price (closing price), corresponding FDV, and the ROI of buying ATH at the opening and selling it.

The left chart shows Launchpool data, and the right chart shows Launchpad data. The median value in the last row is the key point to focus on.

From historical data, the performance of the previous Lauchpool project is far inferior to the Launchpad project. Assuming buying at the average price on the first day and selling at ATH, the median return rate for Launchpad is 2.9 times, while for Launchpool it is only 1.9 times.

And Launchpool has two projects that have reached their peak since opening, and I have been holding onto them until now. Launchpad has not experienced this situation yet (of course, the opening day average price is a convenient data for horizontal comparison, but it cannot reflect the whole picture. EDU is currently likely to be in a trapped state if bought on the opening day).

As for the reason, we can observe that the actual FDV ATH of Launchpad and Launchpool are close to each other, both around 1.9B. However, Launchpool's median FDV on the first day, 780M, is significantly higher than Launchpad's 460M.

This is mainly due to the liquidity issue of Launchpool. Launchpad usually gives around 5% of the share, while Launchpool, as a free coin distribution platform, generally gives less, usually below 2%.

Although the Launchpool opening price was artificially high, due to the majority of BNB holders selling at the opening, a higher opening price was more advantageous for BNB holders. Therefore, Binance had no strong incentive to differentiate this point.

For investors, the long-term game value of Launchpool is obviously lower than that of Launchpad, so it is more important to do a good job of valuation analysis and be more conservative in preparation for Launchpool projects. Blindly rushing in and holding for the long term can easily lead to being trapped.

If you are too lazy to estimate the valuation, refer to the median first-day FDV of Launchpad 460M. Once the FDV of Launchpool's application projects exceeds this value, the probability of high returns in the future is not very high.

Summary Using similar projects' valuations as benchmarks is the most common valuation method. Launchpool's project performance is not as good as Launchpad's, and the coin price often opens at a high level due to liquidity issues, so caution is needed. Launchpool has a small number of projects that have been stuck since the opening, while Launchpad has almost no projects that have been completely stuck.

Original Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia