Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

From obscurity to DeFi rising star—Pendle’s path to success

Original Title: "From Obscurity to DeFi Rising Star - The Journey of Pendle"

Original Authors: Luke, Jane

Introduction

We see the attempts, failures, and price drops that Pendle went through from v1 to v2, and now it has become a rising star. This has piqued our curiosity. Throughout the entire journey of Pendle, what did v1 do wrong, what did v2 do right, and how did they stand out in fierce competition? We hope to use Pendle as an example of a DeFi startup project and entrepreneurial team from the perspective of entrepreneurship rather than investment, to explain the innovation of Crypto Native products, how to build protocols, how to operate businesses, and how to maintain the correct entrepreneurial spirit, providing some reference for builders who hope to contribute to the industry. - Luke & Jane · Decompose interest-bearing assets (i.e. underlying assets that provide yield) into YT and PT. For the same interest-bearing asset, Pendle will decompose it into independent YT and PT based on different maturity dates. ·YT represents the yield rights of income-generating assets. Holding YT will continuously receive floating income from income-generating assets until maturity, so holding YT represents obtaining floating income; PT represents the residual value of income-generating assets after the yield rights are stripped, with no income during the holding period, but can be exchanged back to the corresponding underlying assets at a 1:1 ratio after maturity. Holding PT represents obtaining fixed income. Next, the design of AMM allows these two types of returns (PT and YT) to be swapped: ·Pendle packages interest-bearing assets as SY, standardizes the three common types of interest-bearing assets (Rebase, Accumulate, Distribute) into one type of token. Then, a specialized AMM was designed for trading between SY and PT. Through a mechanism called FlashSwap, YT transactions can also be conducted through this AMM without the need for an additional secondary market. · Different PTs with different maturities will have independent PT-SY liquidity pools. Due to the different duration risks faced by PTs, there will be different prices, which represent different implied yields under different maturities. Regarding token value capture, Pendle has taken inspiration from Curve and implemented the veToken design. Pendle token holders can stake their tokens to earn vePendle, with the amount of vePendle increasing the longer the tokens are staked. Holding vePendle allows for protocol revenue sharing, voting on weekly liquidity incentives distribution, and enhancing LP earnings. ·Basic Asset: Base Asset, the principal of interest-bearing assets, without a yield, such as ETH or DAI. ·Interest-Bearing Assets, also known as Underlying Assets, refer to assets that generate income, such as stETH for ETH and sDAI for DAI, obtained by investing basic assets in other DeFi protocols. a. Rebase Class: Holds Rebase Class Token, the number of tokens will automatically change, and the income will be reflected through the change in the number of tokens. The exchange rate between the interest-bearing asset token and the underlying asset token is always 1:1, such as stETH and aToken. b. Accumulate Class: Holds accumulate class Tokens, the number of Tokens does not change, and the income is reflected by the intrinsic value of the Tokens. The exchange rate between the interest-bearing asset Tokens and the underlying asset Tokens will increase as the income accumulates, such as wstETH and cToken. c. Distribute Class: Holds Distribute Class Token, the quantity of which does not change. Profits are reflected through additional distribution and require users to manually claim, such as the liquidity incentive portion of GLP and LP Token. Pendle team's Co-Founder TN got involved in Crypto when he was still a student in 2014. After graduation, he joined Kyber Network as a member of the Funding Team and served as the BD lead. After leaving Kyber, he attempted some other unsuccessful startups before starting to build Pendle. The other Co-Founder and whitepaper author, Vu Gaba Vineb, previously served as Tech lead at Digix. During an interview in May, TN revealed that their team size is around 20 people, with a structure of 8+8+4. 8 people are in charge of growth, 8 people are in charge of research and development, and 4 people are in charge of product design. The Pendle team also has a high level of transparency, with many core members of Pendle being doxxed on Twitter. In the DeFi industry, which is primarily built on anonymity, this behavior increases user confidence. The team members who are verified on Twitter include institutional leader Ken Chia, who was previously the Asia-Pacific head of Abra and worked at J.P. Morgan before that; growth leader Dan; ecology leader Anton Buenavista (三, 三), who previously served as a senior engineer at Kyber; and Engineering Lead Long Vuong Hoang, who is also a Paradigm Fellow. Pendle conducted seed round financing and IDO in April 2021, selling about 10% of its seed shares and raising 3.7 million USD. The tokens will begin to unlock three months after the IDO and will be fully unlocked after one year. Early investors in Pendle have now received approximately 10 times return on their investment :) After the Pendle fire this year, Binxin Venture announced its investment in Pendle in the form of OTC. After the token was launched on Binance, Binance Labs also announced its investment in Pendle. Recently (11.9), Pendle's early supporter Spartan Group made additional investments through OTC, demonstrating their confidence and recognition in Pendle. Pendle's initial funding background is somewhat dim compared to competitors such as Element Finance (which received seed funding from a16z and a total funding amount of 36.4m), but they still raised enough money to help the team weather the ups and downs. The main difference among everyone is the design of YT, which represents the right to obtain floating income of productive assets. The design can be broadly divided into two types: Collect YT: ·YT's price during trading only represents the pricing of future returns on the interest-bearing asset. However, after maturity, since YT cannot obtain any returns in the future, its fair price should be 0. ·Pendle v1/v2, Swivel, and Sense all use this design. Drag YT: ·Therefore, the value of YT = the value of accumulated past earnings + the value of future earnings. Before maturity, the value of future earnings cannot be determined, which causes fluctuations in the price of YT. However, after maturity, the value of YT will become a fixed value. ·Element, AP Wine, and Tempus have adopted this design. Meanwhile, the design of Collect YT is more ingenious: · From the user's perspective, leaving the realized profits in YT without being able to withdraw them for other investments is a waste. From a trading perspective, if the pricing of YT mixes past profits with future expectations, calculating a fair price becomes more complex. · From the perspective of protocol design, the final price of YT will be equal to a fixed value, which is a feature of YT. And the final price of YT is 0, which makes it easier to design the corresponding AMM. This is the design concept of Pendle v1 AMM. When using the Drag YT protocol, the AMM design related to YT becomes somewhat ugly. YT ultimately equals a constant value, which is the accumulation of past profits. However, how much profit has been accumulated in the past varies depending on the asset and pool, and there is no universal value. Therefore, it is necessary to introduce a contract that records the accumulation of profits and design the AMM based on this dynamic value. There are two design approaches for transactions: · Shuangchi: ·It is necessary to establish liquidity pools for PT and YT respectively. Generally, protocols will design special AMMs for one of the tokens, while the other token will be traded using a universal AMM. · Pendle v1, Element, and AP Wine all use this design. Although Tempus trades PT/YT in the same pool, if the two assets can only trade with each other and cannot form LP with external assets, they still cannot be truly priced and traded, so it is essentially a dual-pool design. · Single Pool ·Use the same liquidity pool to meet the trading needs of both PT and YT. This design is called FlashSwap, which utilizes the relationship between interest-bearing assets = PT + YT to virtually create tokens during the swap process, allowing the dual-currency pool to trade three types of tokens. · Taking the process of selling 10 YT to the LP pool of SY-PT as an example: first, 10 PT is virtually created and combined with 10 YT to form 10 SY, then 9 SY is swapped for 10 PT and destroyed (assuming PT=0.9 SY at this time), and the remaining 1 SY is the result of selling 10 YT. ·Compared to dual-pool design, single-pool design is more ingenious, and the benefits are obvious, solving the problems of transaction friction brought by dual-pool. Pendle v2, Swivel, and Sense all adopt this design. The design of AMM is crucial in protocol design. The design of AMM needs to conform to the characteristics of asset trading. PT and YT assets have three characteristics: ·As maturity approaches, volatility will become smaller: Because the closer it gets to the expiration date, the duration risk becomes lower. Therefore, AMM also needs to reflect this characteristic of decreasing volatility, that is, liquidity becomes more concentrated over time. ·Near Maturity and the price of PT or YT will converge to a fixed value: PT = underlying asset, YT = 0 or the accumulated income during this period, and AMM also needs to reflect this price change over time. Most interest rate swaps AMMs are based on the Balancer, Yield, and Notional curves for innovation: Balancer v2: ·The curve of Balancer v2 is basically the same as the constant product curve of Uniswap, except that the constant product curve of Uniswap v2 only supports two assets, and the value of the two assets is 50/50, while Balancer v2 can control the weight of each asset value using the parameter w, such as the classic 80/20 pool, and supports assets greater than or equal to two. · Pendle v1 and AP Wine have innovated on the Balancer v2 curve. Taking Pendle v1 as an example, Pendle has designed a unique AMM for YT and SY. The YT in Pendle v1 belongs to Collect YT, and its value will return to 0 after Maturity. Therefore, Pendle v1 uses the time parameter t to affect the weight parameter w. When the liquidity pool is initialized, the value ratio of YT and SY is 50/50. As Maturity approaches, the w of YT decreases, and its value proportion also decreases: 40/60, 30/70... until Maturity: 0/100. This is in line with the characteristic of Collect YT where the value returns to 0 after Maturity. ·AP Wine also used a similar logic to transform the Balancer v2 curve, but AP Wine is designed for PT and SY AMMs, so there are slight differences in implementation details compared to Pendle v1, which will not be elaborated in this article. Yield Protocol: ·Yield Protocol is a fixed-rate protocol that uses AMM to achieve fixed rates by selling zero-coupon bond-like tokens at a discount. The trading scenario is consistent with PT-like token. Therefore, some interest rate swap projects will directly transplant Yield Protocol to their own projects for PT trading. ·Both Element and Sense follow the same principle. Taking Element as an example, it establishes a liquidity pool with PT for underlying assets. At the beginning of the liquidity pool establishment, the curve is a constant product curve of x*y. As it approaches Maturity, the curve changes to x+y, which means that the exchange rate between PT and underlying assets is 1:1. Yield Protocol's curve satisfies the characteristics of "PT Maturity will be worth 1:1 with underlying assets" and "the volatility will decrease as it approaches Maturity". ·Sense and Element are basically the same, with not much change to the Yield Protocol curve. Tempus, on the other hand, is designed for PT and YT with an AMM curve. The Tempus code is based on Curve, but the specific approach is similar to Yield Protocol. Notional v2: ·Notional v2 is a fixed-rate lending protocol that operates on the same track and idea as Yield Protocol - achieving fixed rates using the principle of zero-coupon bonds. However, the difference with Notional v2 is that they use a flatter Logic Curve, which has lower volatility and higher capital efficiency when the pool is first established. Therefore, Notional v2's curve is an improved version of Yield Protocol's. We provide detailed formulas in the appendix. For Pendle, if it wants to achieve sustained growth, on the one hand, it needs to continuously understand the ecosystem, just like in the LSD ecosystem. On the other hand, it needs to seek out more valuable ecosystems. • Prioritize rooting in the field (public chain) with abundant water and grass. The expansion of the chain is an important source of Pendle TVL. In addition to Ethereum and Arbitrum, Pendle has recently settled in BSC and Optimism. In terms of the logic of chain selection, for Pendle, the chain itself needs to have a relatively mature asset ecosystem and a sufficient volume (hundreds of millions of dollars +). Because there is a conversion rate from the original asset to Pendle, only when the volume of the chain is large enough, Pendle's investment makes sense. Based on this standard, there are not many chains that Pendle can choose. TN mentioned in an interview that they may consider joining Polygon in the future, but it is not a high priority at the moment. Why is there a priority? It is speculated that on the one hand, there are limited resources for operation and promotion, and on the other hand, Pendle has not yet been able to list assets without permission. The team needs to research the listing protocol and write contracts themselves, which takes at least a week, making the team's energy one of the bottlenecks for expansion. Pendle's operations on BSC and OP are not doing well, so it is necessary to carefully evaluate priorities and guide the team's energy towards the most productive areas and pick the low-hanging fruits first. Token incentives are commonly used in the DeFi ecosystem, but different project teams have different views on when to implement token incentives. For example, Kenton, the founder of Sense Protocol, which is similar in principle to Pendle, believes that DeFi protocols should avoid token incentives before reaching PMF, as token incentives can make it difficult for DeFi products to obtain real feedback. However, from the example of Pendle, token incentives may lead to a certain "false prosperity", but it also helped Pendle attract a group of users when the product usability and PMF were not very good, and obtained earlier product feedback, such as what kind of assets are suitable for Pendle's trading form. At the same time, the TVL pushed up by token incentives is not meaningless. High TVL will bring low slippage and make it easier to attract whales and institutional users. It also verifies its security with large amounts of money. These are network effects for a DeFi protocol, and the cost of these attempts is borne by the token, without excessive consumption of current cash reserves, which is still a good choice for teams with insufficient early funds. Currently, Pendle's core goal is to increase the protocol's trading volume and TVL. To achieve this goal, promoting PT is the most effective means. Firstly, the PT scenario is simple, clear, and easy to promote. Secondly, the PT trading experience is indeed better. Considering the relationship between PT and YT, when the PT trading volume increases, the YT trading volume will also increase, killing two birds with one stone. Another aspect is to expand the audience. Given that the interest rate trading is still a relatively niche market, how to reduce the understanding threshold and achieve a wider acceptance is also a top priority for the next step. The user group can be simply divided into retail users and institutional clients. Different groups require different breakthrough strategies. 机构是 Pendle 的又一拓展重心。要实现机构端的大规模采纳,除了有效的 BD 策略,产品端也有许多要完善的地方来适配大资金体量,比如足够深的池子深度来实现较小的无常损失,资金效率高,可实现多元化的策略等。值得一提的是,Pendle 上不同 stETH 池子之间已经形成了利率结构。如果这类池子的深度继续加深,则机构可以利用 PT 构建自己的跨期“无风险”投资策略。 Organizations are another focus of expansion for Pendle. In order to achieve large-scale adoption on the institutional side, in addition to effective BD strategies, there are also many areas on the product side that need to be improved to adapt to large capital volumes, such as deep enough pool depth to achieve smaller impermanent losses, high capital efficiency, and the ability to implement diversified strategies. It is worth mentioning that a rate structure has already been formed between different stETH pools on Pendle. If the depth of these pools continues to deepen, institutions can use PT to build their own cross-term "risk-free" investment strategies. Organizational users are the main players in the traditional interest rate market in the financial industry. Pendle attaches great importance to this and has a dedicated institutional manager (@imkenchia). In the early days of Pendle, TN would contact institutions and schedule 1-on-1 meetings to introduce them to the profit opportunities of Pendle. This is also a side of TN's entrepreneurial spirit: willing to get hands dirty, the founder is the biggest salesperson. TN actively participates in various interviews, also for this purpose. At a community meeting at the end of August, Pendle revealed that the current institutional TVL ratio has reached 20%. As the main platform for reaching deep Web3 users, Twitter is a natural choice for Pendle. However, while content strategy is a standard feature for every DeFi protocol, Pendle has still managed to make its own mark in this area. Pendle's current ambassadors include @crypto_linn, @ViNc2453 (Chinese region), and @Neoo_Nav (Vietnam). What is particularly noteworthy is that each ambassador has a deep understanding and appreciation for Pendle, rather than simply being there for the paycheck :) Taking crypto linn as an example, she has repeatedly expressed her admiration for Pendle and its team in her writing without any reservation: This appreciation comes partly from the solid business capabilities of the Pendle team, and partly from their thoughtful and in-depth communication with influencers. @2lambro once mentioned that Pendle is one of the few teams that truly reads the content written by different influencers, understands their audience, builds connections as friends, and helps promote them as professionals. They schedule one-on-one meetings with influencers to seek feedback and share Pendle's future plans. Respect and sincerity will bring heartfelt recognition, True~ TN, as a founder, is also highly recognized. When building a brand for the C-end, the founder's positive image and reputation are also a key factor, and may even drive the product to become popular. Building user trust in DeFi new protocols is a long-term project, in addition to standardized strategies such as audits, trust transfer of the founder/team is also a way. Choose a promising track, design suitable curves, and explore assets in the wind. Pendle's TVL and Volume have been growing, especially this year when we are in a bear market in the crypto industry, which makes it even more rare. · The token inflation used for liquidity incentives in Pendle can be seen as the protocol's expenditure. Currently, Pendle spends about 34k Pendle per day, while daily revenue is about $1.5k. From this perspective, Pendle has not yet achieved product-market fit and is far from profitable. However, the fee structure of Pendle is currently not finalized, and when the protocol develops into a mature stage, new and more reasonable fee structures may be established. ·Volume represents the usage of trading functions, which can also be represented by Volume/TVL. The question is whether the protocol has real demand or is just a castle in the air stacked with TVL. Pendle's number is 0.79%, which to some extent indicates that the current users of Pendle are mainly liquidity providers, and the proportion of "real demand" - PT/YT buyers is still relatively low. · In addition to Pendle, another well-known DeFi project, Curve, is also often criticized for its low volume/TVL (usually from Uni supporters lol). However, Curve is actually very similar to Pendle: an AMM optimized for specific trading scenarios, with liquidity incentives in addition to trading. This feature has created a thriving Curve ecosystem, but it also exacerbates the low volume/TVL performance. Therefore, we will compare the data of Pendle and Curve to evaluate the current state of the business. Welcome to join the official BlockBeats community: Telegram Subscription Group: https://t.me/theblockbeats Telegram Discussion Group: https://t.me/BlockBeats_App Official Twitter Account: https://twitter.com/BlockBeatsAsia

Pendle 是什么?

translates to What is Pendle?

in English.Product Introduction

Pendle is a DeFi protocol designed for the fixed income/interest rate swap market. Interest rate swaps are a very large track in traditional finance, referring to the exchange of fixed income and floating income with the same principal: for example, for the same US dollar-denominated income, person Y gives up fixed income in exchange for current income, and person X gives up current income in exchange for fixed income.

Pendle has implemented similar things on-chain, first splitting the profits into two categories:

Noun Explanation

Team Introduction

Funding Information

Users & Scenarios

Trading YT/PT

AMM Curve Design

For Pendle, assets with such features are ideal and suitable for absorption, especially those that are currently popular and have sufficient volume. Large volume also means that the depth of the pool may be sufficient, providing a better trading experience. In addition, the volatility of GLP's weekly returns is attractive to swing traders, which has led to more speculation and trading activities.

https://stats.gmx.io/arbitrum

https://stats.gmx.io/arbitrum

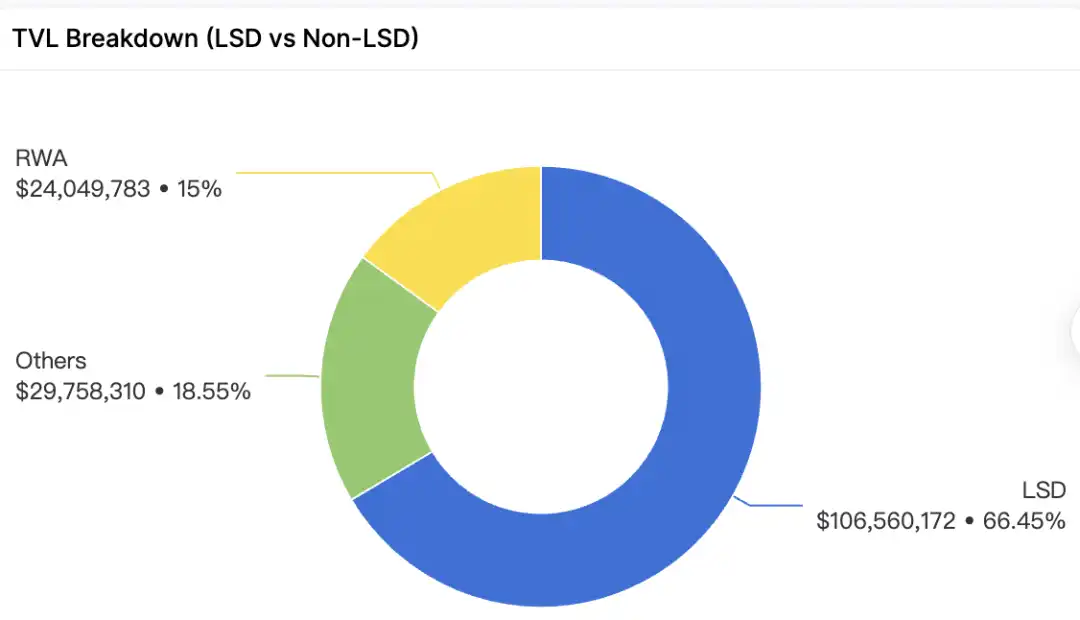

Currently, Arbitrum is the second largest chain on Pendle, contributing nearly 30% of TVL.

https://defillama.com/protocol/pendle

• Proper use of token incentive mechanisms用户增长&教育

User Growth & Education

• Pendle Earn: Integrating third-party layouts into as many channels as possible.

In July 23rd, Pendle launched Pendle Earn, which replaced the narrative of discounted assets with APY. Its front-end looks like a financial product on a centralized exchange, but it is built on-chain. The interest rates and terms of the fixed-income products it provides are determined by smart contracts, which are relatively transparent and a differentiated supplement. Users do not need to understand the complex concepts of interest rate trading, they only need to choose products that meet their expected returns.

• Provide institutional-level interest rate products.

20231009 Data

20231009 Data

• Work closely with Influencers to build trust and educate users. https://twitter.com/crypto_linn/status/1691032585739087873

https://twitter.com/crypto_linn/status/1691032585739087873 https://twitter.com/defi_mochi/status/1690231302577061888

https://twitter.com/defi_mochi/status/1690231302577061888Interpreting the Current State of Pendle through Numbers

Qualitatively, Pendle is an excellent protocol, but it is not without risks. Only by observing it from a quantitative perspective can we determine at which stage Pendle's product development is, whether it has found PMF, and what the next development direction is.

Qualitatively, Pendle is an excellent protocol, but it is not without risks. Only by observing it from a quantitative perspective can we determine at which stage Pendle's product development is, whether it has found PMF, and what the next development direction is.Latest Data Performance

Source: DefiLlama/Coingecko/Sentio/Pendle docs

Pendle VS Curve

Source: DefiLlama/Coingecko/twitter@smyyguy