Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

SignalPlus Macro Analysis: US Economic Data Strong and Inflation Expected to Continue Rebound

Original title: "SignalPlus Macro Analysis (20240417): US economic data is strong and inflation will continue to rebound"

Original source: SignalPlus

Although the intraday price trend was volatile and the thin order liquidity made the profit and loss situation still quite tight, the market was able to take a temporary breather yesterday. Yesterday’s Chinese economic data got off to a relatively positive start, with second quarter GDP up 5.3% year-on-year, well above consensus expectations of 4.8%, however, optimism quickly faded as investors remained skeptical of fundamental strength, especially given much weaker industrial production and retail sales data, with industrial production up just 4.5% in March, well below expectations of 6.0% and last year’s 7%, while manufacturing capacity utilization plummeted to 73.8%, the lowest level outside of the pandemic since 2015, with the decline in utilization evident even in state-supported sectors such as automobiles, chips, solar panels and other electrical equipment, fueling investor concerns about looming overcapacity problems.

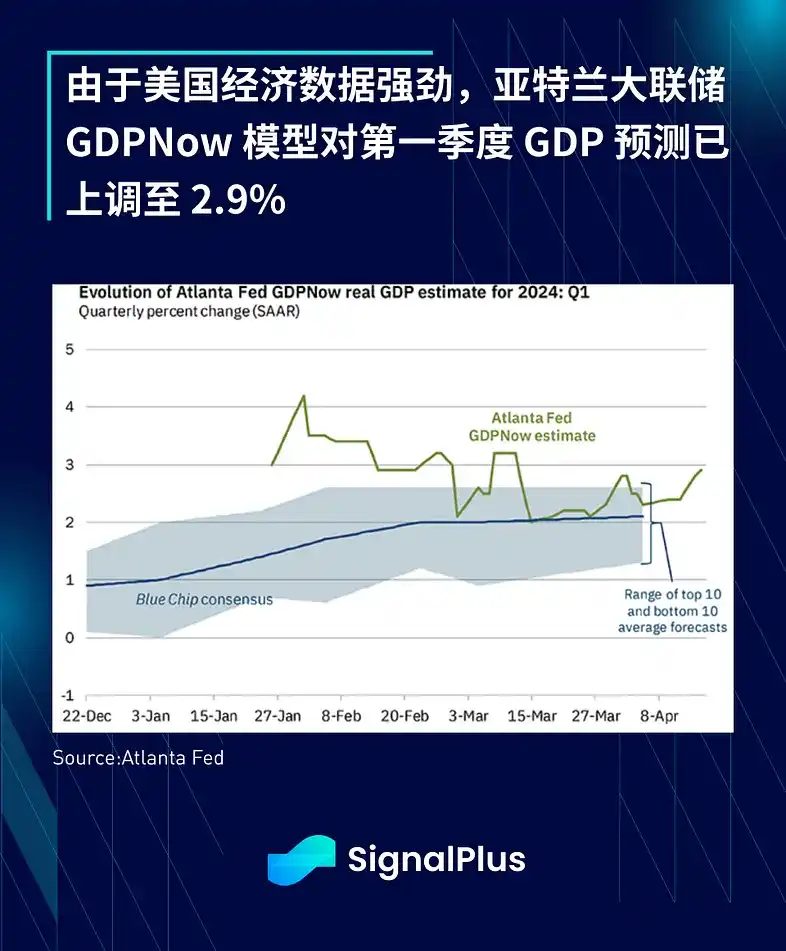

In the US, recent strong data has led to an upward revision of the Atlanta Fed GDPNow model’s GDP forecast to 2.9%, still well above Wall Street’s forecasts. As inflation concerns mount, the 10-year real yield (adjusted for inflation) has risen back to 2.2%, and the 2/10s real yield curve has steepened to its steepest level since October 2022. Does anyone remember that some macro observers "guaranteed" a recession in 2022-2023 due to an inverted yield curve?

As the reality of stubborn inflation and strong economic conditions cannot be ignored, the entire Fed, even the Chairman himself, has been forced to withdraw their dovish rhetoric, leaving the Fed in an isolated position regarding the future policy trajectory:

· Fed Chairman Powell: "Recent data has clearly not given us greater confidence, but rather suggests that it may take longer than expected to reach this level of confidence"

· Fed Vice Chairman Jefferson: If "inflation is more persistent than I currently expect", US interest rates may have to remain higher for longer.

· Boston Fed Collins: "It may take more time than previously thought" and "the CPI data in the first quarter was higher than I hoped"

· Richmond Fed Barkin: Hope to see more "broader signs of slowing inflation, not just commodity inflation"

· New York Fed Williams: "Rate cuts don't seem imminent", suggesting that "we certainly need higher interest rates in some cases, but this is not the basic situation I think"

Compared with the statements of other developed market central banks:

· ECB Lagarde: Unless there are major surprises, the ECB will start cutting interest rates soon; "We are watching the process of slowing inflation, and its progress is in line with our expectations"

· Bank of England Lombardelli: Rate cuts "are the way forward"

· Bank of Canada Macklem: "We don't have to follow the Fed's actions, we have to take the actions that Canada needs"

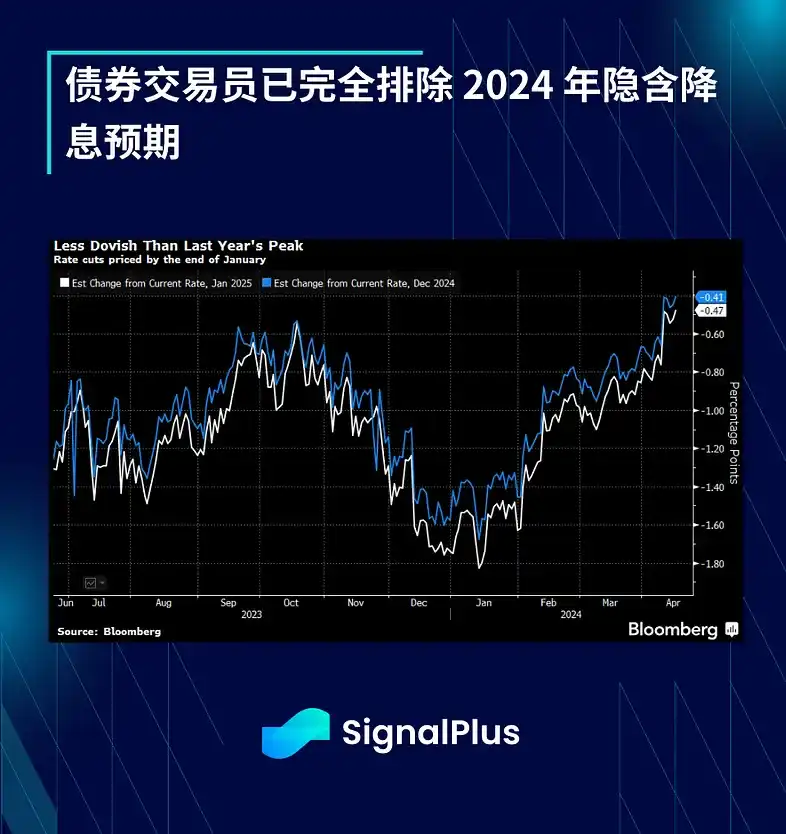

Against the backdrop of the Fed's U-turn in attitude, the interest rate market has ruled out 2024 Most of the rate cut expectations for the year have been eliminated, and the dovish sentiment in the first quarter has disappeared completely, even breaking through the hawkish high in October last year. In addition, the policy divergence between the Fed and other central banks has brought strong buying to the US dollar, with USD/JPY above 155 and USD/CNY above 7.10, and the overall DXY index is back to its strongest level since 2022.

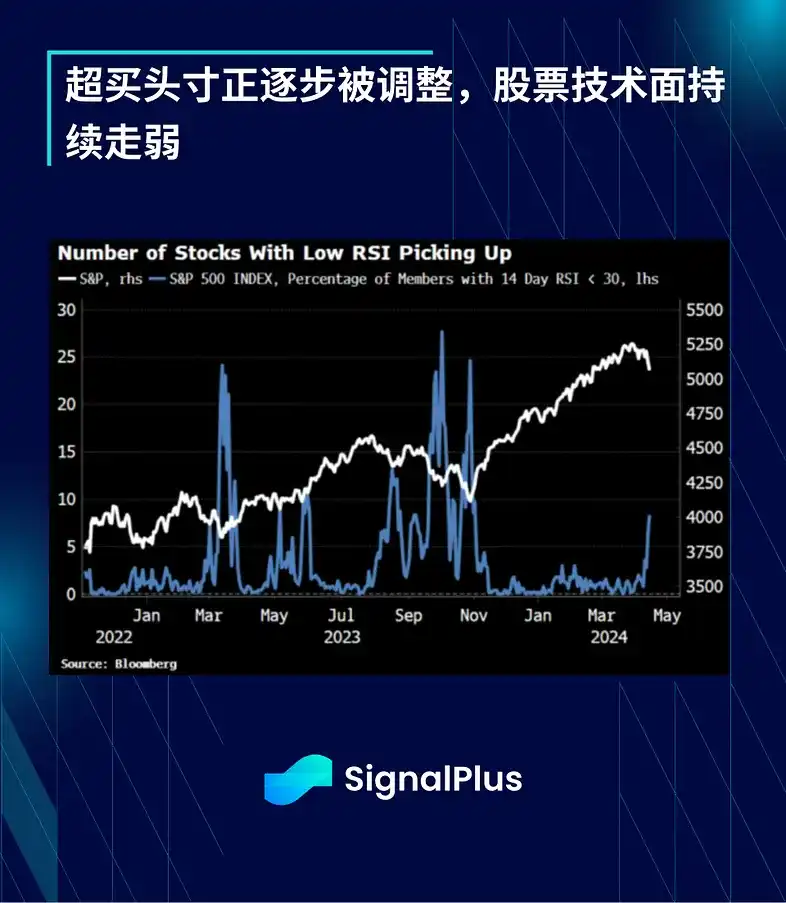

In addition, the spillover effect of rising real yields is more serious this time, and the stock market has finally succumbed to the "higher interest rates for longer" interest rate outlook, although this is more caused by overbought positions rather than changes in fundamentals. The negative correlation between US stocks and yields has increased, causing the SPX index to fall 1% for the first time since October last year. In addition, the stock VIX closed above 19 for the first time since Halloween. The stock implied correlation has jumped to 23, compared to only 12 at the end of March. The ongoing tensions in the Middle East may keep implied volatility at a high level in the short term.

In terms of cryptocurrencies, BTC prices have not broken further downwards and are hovering at $64,000 as of this writing. However, other tokens have performed much worse than BTC. As the SEC's chances of approving an ETH ETF in this round are getting lower and lower, the ETH/BTC ratio has continued to fall to a near 4-year low, while altcoins have lost 30% to 40% of their value in the past month, much higher than BTC's -5%. The market has seen severe losses over the past 1.5 weeks and it will take quite some time to recover.

ETF inflows also continue to slow as retail “buy the dip” interest is low, with Blackrock’s IBIT being the only ETF to show net inflows since last Friday. ETF inflows are expected to be less significant in the short term as the current FOMO narrative is largely over, and we expect BTC price action to once again resemble the more volatile Nasdaq, reverting to the behavior patterns of the past 4 years.

That said, Bitcoin is less like digital gold and more like a leveraged beta instrument, and hopefully fellow tech stocks can hold their ground with strong earnings results in the upcoming earnings season, good luck to everyone!

Original link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia