Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Dragonfly partner: Is VC coin really the culprit of this round of "bull market without mutual support"?

Original title: "Why are all these low float / high FDV coins down bad?"

Original author: Haseeb, partner of cryptocurrency venture fund Dragonfly

Original translation: Elvin, ChainCatcher

Editor's note: The discussion about "high FDV low circulation tokens" has been hot these days. Many people believe that VC coins have become the culprit of this round of "mutual bull market". Haseeb, partner of cryptocurrency venture fund Dragonfly, refuted some views with data, and he believes that for VC, project valuations have reached astronomical figures, and VC will also face unlocking difficulties. This makes LP think that this asset class is fake. Although it looks good on paper, it is actually bad, and VC does not want this. Asset prices gradually rise steadily over time, which is what most people want.

Is the market structure broken? Are VCs too greedy? Is this a rigged game for the secondary market?

Almost all the theories I’ve seen on this subject seem wrong. But I’ll let the data speak for itself.

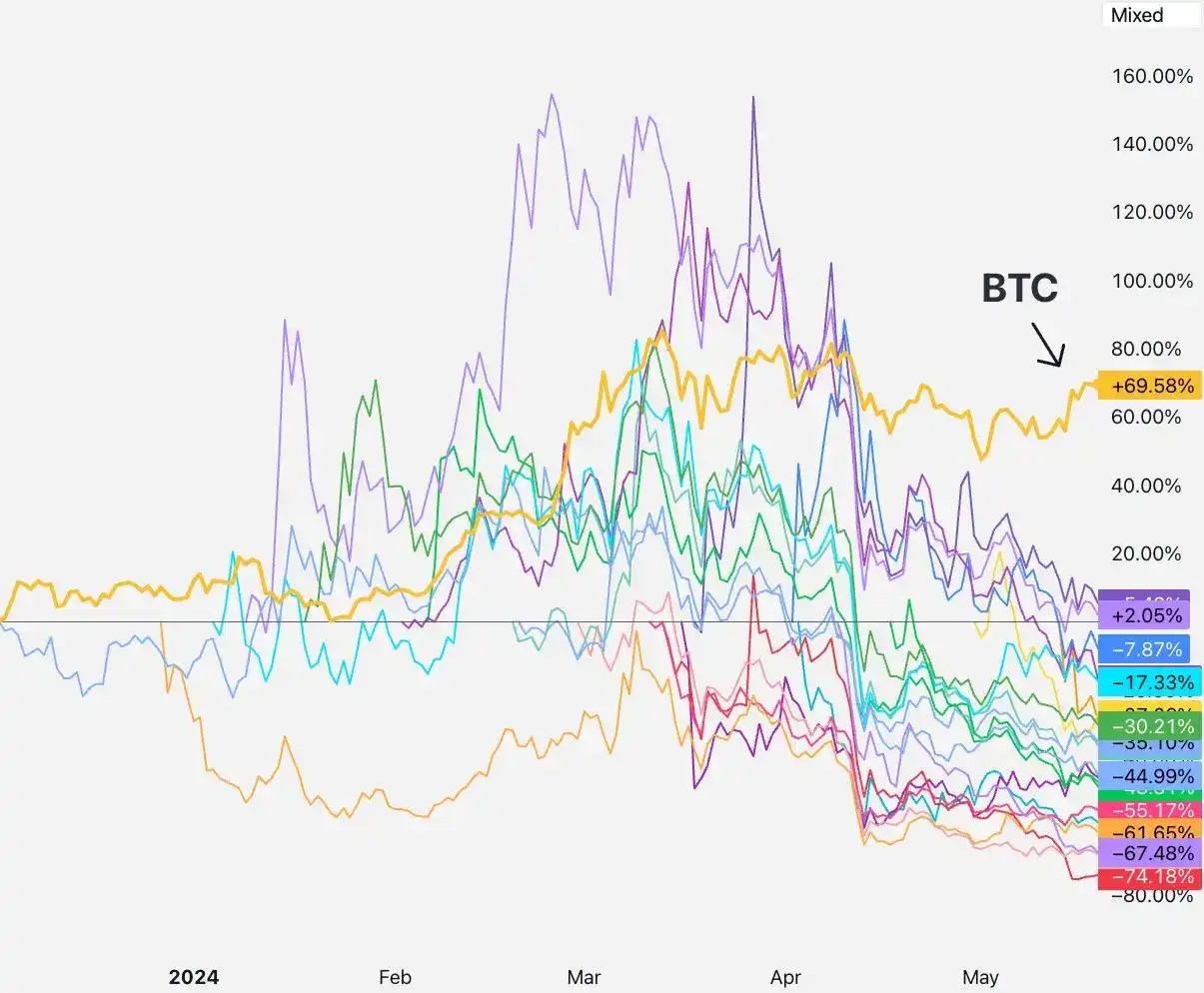

Here’s the infamous chart that’s been making the rounds, from @tradetheflow _, showing a bunch of recent Binance listings going down. Most of them are derided as “high FDV (fully diluted value), low circulation” tokens, meaning they have pretty high FDV valuations but a small day one circulating supply.

I charted all of these and removed the labels. Excluded any related MEME coins, as well as tokens that TGE’d long before Binance, like RON and AXL. Here’s what it looks like, with BTC (beta) in yellow:

I charted all of these and removed the labels. Excluded any related MEME coins, as well as tokens that TGE’d long before Binance, like RON and AXL. Here’s what it looks like, with BTC (beta) in yellow:

Almost all of these “low circulation, high FDV” Binance listings are down. What could explain this? Everyone has a favorite theory about the disruption to market structure. The three most popular theories right now are:

1) VCs/KOLs are dumping into the secondary market

2) The secondary market is angrily dumping these tokens and only buying meme coins

3) Supply is too small for meaningful price discovery

All make sense! Let’s see if they are true. But to keep things scientific, we need a null hypothesis to disprove. Our null hypothesis should be: these assets all repriced, but there is no deeper market structure problem. (The classic “in the end, there are always more sellers than buyers.”)

We will discuss each theory one by one.

1) VCs/KOLs are dumping into the secondary market

If there is a story here, what should it look like?

We should see tokens with shorter lockup periods sell off faster than others, while projects with longer lockup periods or no KOLs should do well. (Highly liquid perpetual contracts could also be another vector for this dumping.)

So what do we see in the data?

As you can see from the data in the above chart, the tokens actually performed well from listing to early April - some were above the listing price, some were below the listing price, but most were concentrated around the zero axis. Before that, it seemed that no VC or KOL had sold.

Then in mid-April, everything started to fall. Despite these projects listing on many different dates and having many different VCs and KOLs, did all of these projects unlock in mid-April and start selling to the secondary market?

Let me share my perspective here. I am a VC. There are definitely VCs dumping in the secondary market space - there are also VCs that do not lock up, hedge over the counter, and even break lock up, but these are low-tier VC firms, and most of the teams working with these VCs are not selling on the first-tier exchanges. Every top VC firm you think of has at least a one-year cliff and multiple years of vest before acquiring tokens. In fact, the 1 year cliff period is mandatory for anyone regulated by the SEC under Rule 144a. Additionally, for large VC firms like us, our positions are too large to hedge outside of exchanges, and we are often contractually obligated to unlock early.

So here’s why this story doesn’t make sense: every single one of these tokens is less than a year away from the TGE, which means the VCs with the 1 year cliff period are still locked up!

Maybe some of these lower tier VC projects sold their tokens early, but all projects went down, even the top tier VC funded projects that are still locked up.

So it may be true that for some tokens, there are investors/KOLs dumping - there are always some projects with bad behavior. But if all tokens fall at the same time, this theory cannot explain that.

On to the next theory.

2) Secondaries dump these tokens in anger and only buy meme coins

If this is true, then what we should see is: the price of these new token issuances falls, and the secondary market turns to meme coins.

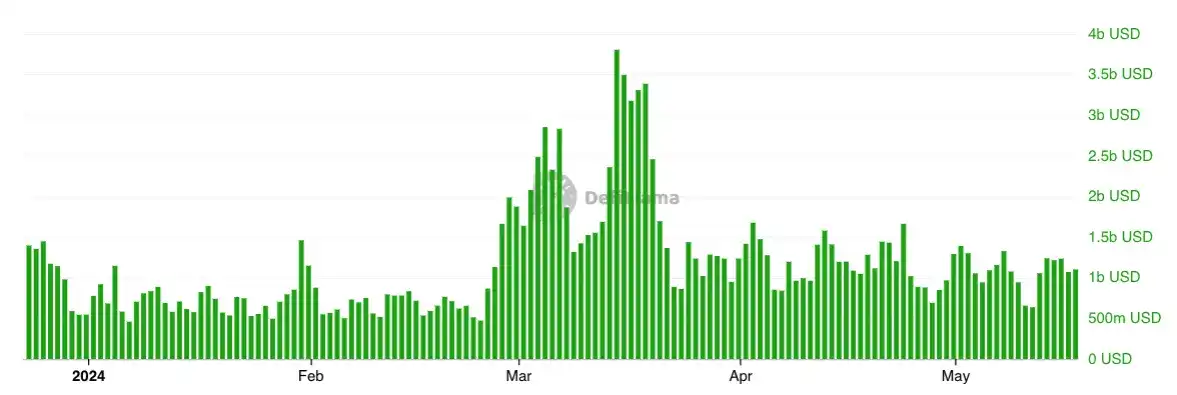

Instead, what we see is this:

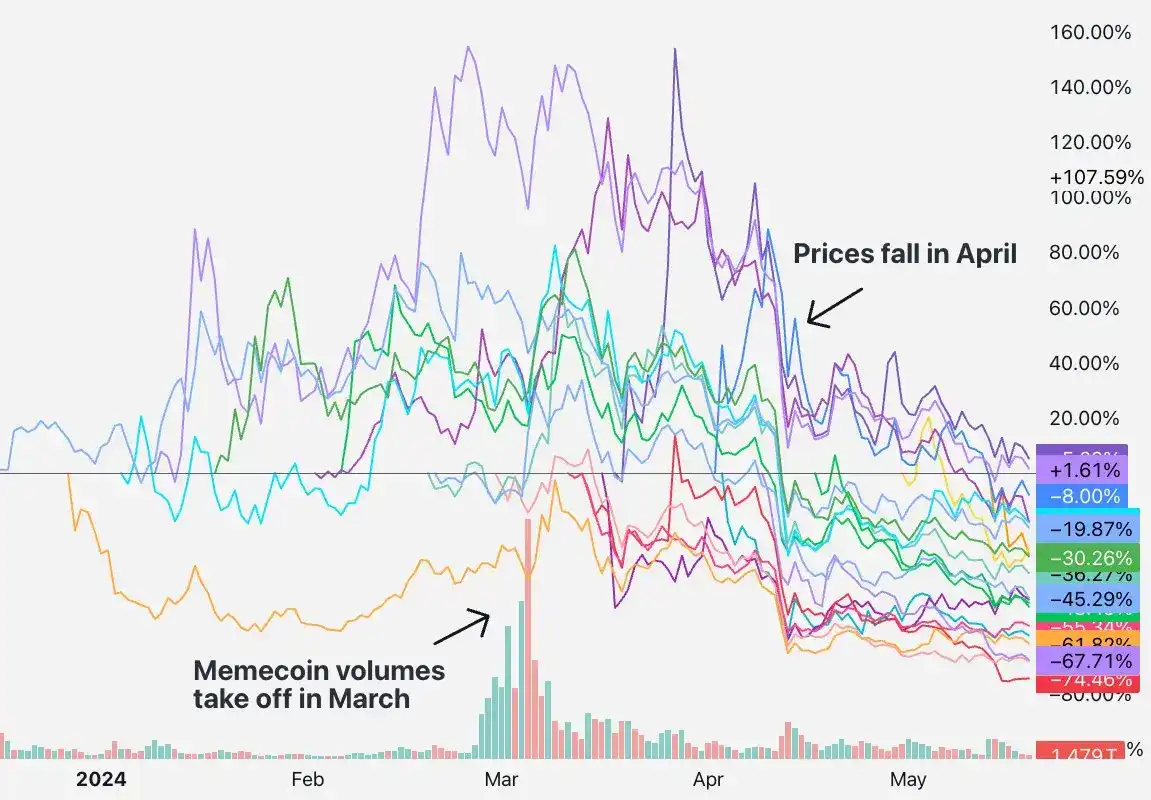

I charted SHIB volume based on this basket of tokens. But the timing is wrong. By March, the craze for Memecoin had reached a crazy level, but a month and a half later in April, the entire basket was sold off.

This is the volume on Solana DEX, and it tells the same story - meme coins exploded by early March, mid-April.

So this doesn't match the data either. There hasn't been a massive shift to memecoin trading after this basket of tokens devalued. People are trading meme coins, they're trading new coins, and the volume doesn't tell any clear change.

The problem isn't the volume, it's the price of the asset.

That is, many are trying to sell the story that the secondary market is disillusioned with real projects and is now primarily interested in meme coins. I went to Binance's Coingecko page and looked at the top 50 tokens by volume, and about 14.3% of Binance's volume today is meme coin trading pairs. Meme coin trading is just a small part of what's happening in the crypto space. Financial nihilism is indeed a phenomenon, and it is very prominent in the crypto market, but most people in the world are still buying tokens because they believe in some technical story, whether it is right or wrong.

So, okay, maybe the retail movement from VC tokens to meme coins is not literal, but here is a sub-theory: VCs own too many of these project tokens, and this is why retail rage-exited. They realized (suddenly in mid-April?) that these were all scams, and the VC tokens, team + VC owned ~30-50% of the token supply of these projects. This must have been the last straw that broke the camel's back. It seems like a satisfying story.

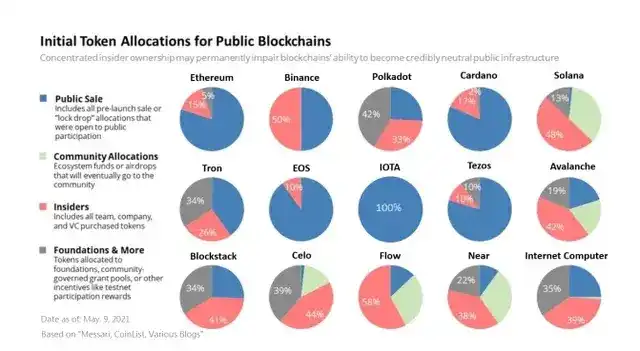

But I’ve been doing crypto VC for a while. Here’s a snapshot of token distribution from 2017-2020:

Look at the red shaded area — that’s the percentage of insiders (team + investors). SOL 48%, AVAX 42%, BNB 50%, STX 41%, NEAR 38%, etc. It’s pretty much the same story today. So if the theory is “these tokens weren’t VC coins in the past, but are now”, that doesn’t fit the data either. Regardless of the cycle, capital-intensive projects always face overhang from teams and investors when they launch. These “VC coins” have been successful even after the tokens were fully unlocked.

In general, if what you’re referring to also happened in the last cycle, it doesn’t explain the unique phenomenon happening now.

So this story of “secondary markets getting angry and trading meme coins” sounds true and is a nice satire, but it doesn’t explain the data very well.

On to the next theory.

3) Too little supply for price discovery

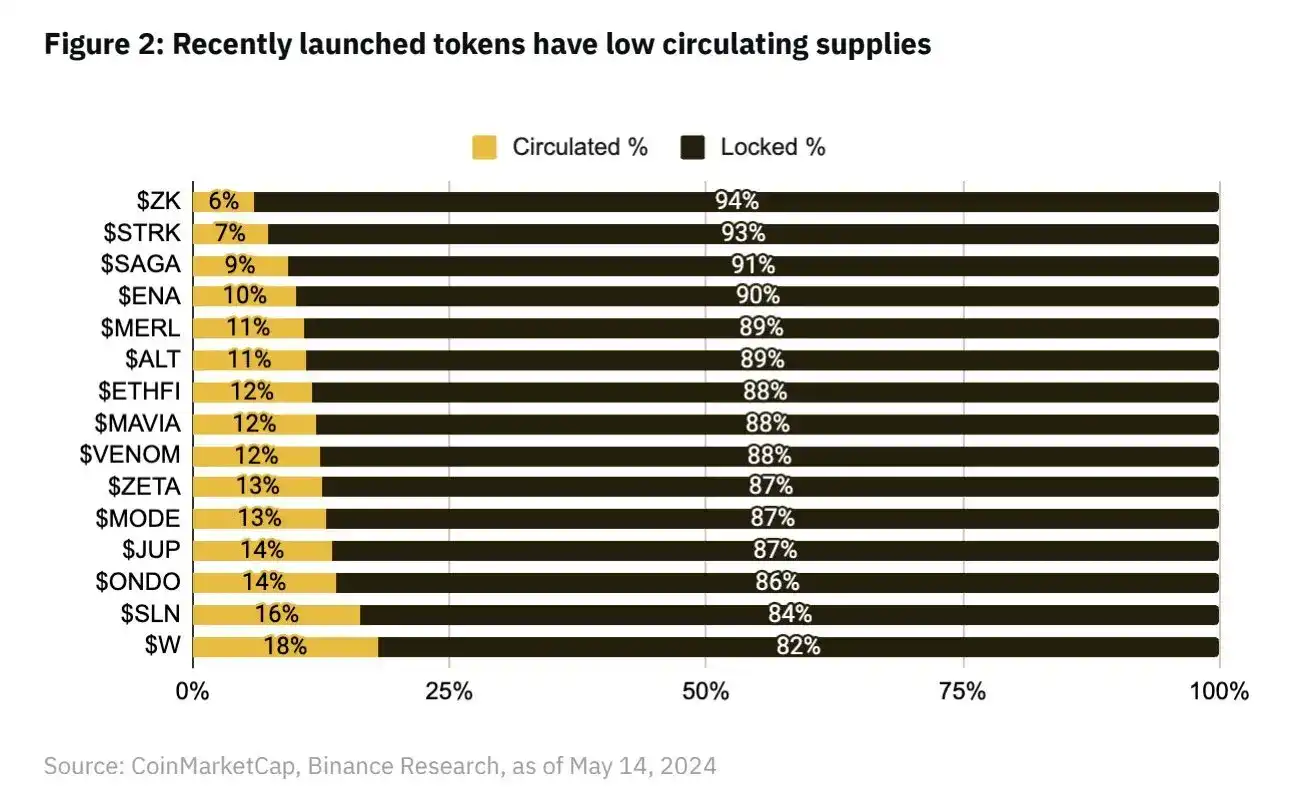

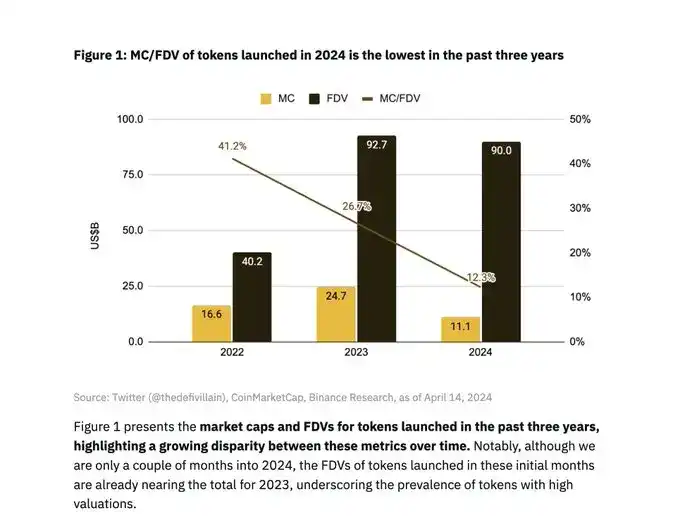

This is the most common approach I’ve seen. Sounds good! It’s not as sensational, which is its advantage. Binance Research even published a nice report on this:

It looks like the average is about 13%. That’s super low, and significantly lower than past tokens, right?

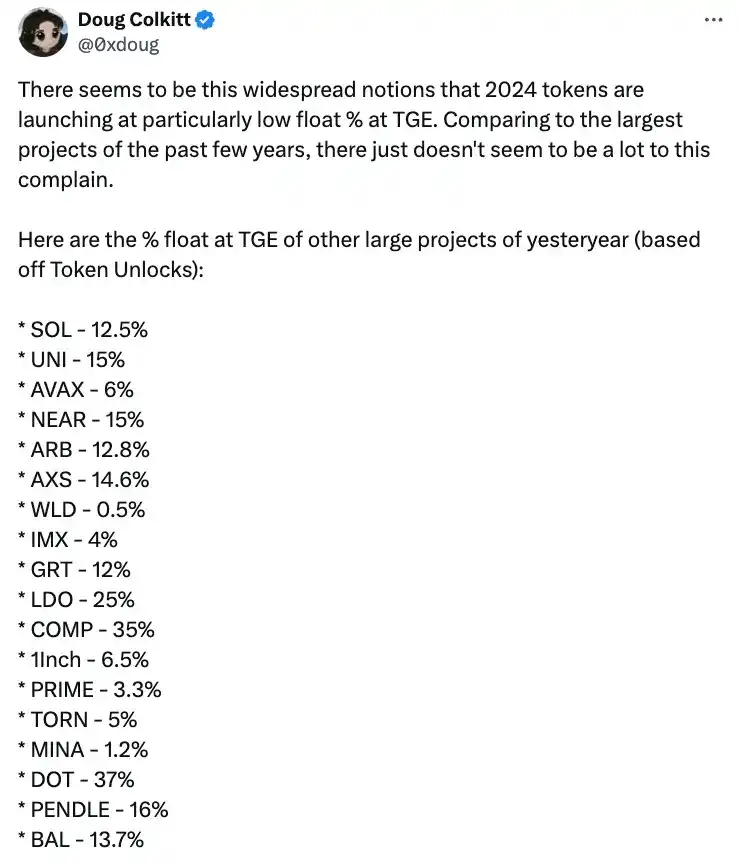

Is this the correct number?

Credit to @0xdoug for pulling this data. You guessed it, the average circulation of these tokens in the TGE last cycle was 13%.

PS: There is another picture in the same article from Binance Research that has also been widely circulated, claiming that the average circulation of tokens launched in 2022 is 41% at launch.

I’m sorry—WHAT? I’m around 2022, the project hasn’t even launched yet, and the circulating supply is already 41%.

I extracted Binance’s 2022 list: OSMO, MAGIC, APT, GMX, STG, OP, LDO, MOB, NEXO, GAL, BSW, APE, KDA, GMT, ASTR, ALPINE, WOO, ANC, ACA, API3, LOKA, GLMR, ACH, IMX.

Spot-checking a few of these, as they don’t all have data from TokenUnlocks: IMX, OP, and APE are similar to the latest batch of tokens we’re comparing, with IMX at 10% on day one, APE at 27% on day one (but 10% of that is APE treasury, so I rounded it up to 17% on day one), and OP at 5% on day one.

On the other hand, you have LDO (55% unlocked) and OSMO (46% unlocked), but they were listed over a year before Binance listed, so it’s silly to compare those lists to the latest day one list. If I had to guess, these non-day one listings plus random company tokens like NEXO or ALPINE are why they get such high numbers. I don’t think they’re describing the true trend of real TGEs — they’re describing the trend of tokens listed on Binance every year.

Okay, maybe you’ll admit that 13% of circulating supply is similar to past cycles. But that’s still too little for price discovery, right? And the stock market doesn’t have that problem.

After all, just look at the median first-day circulating supply of 2023 IPOs.

But seriously, too low a circulating supply is definitely a problem. WLD is a particularly egregious example, with just 2% circulating supply. FIL and ICP also had extremely low circulating supplies at launch, which resulted in very ugly price charts. But most of the tokens in the Binance group had day one floats that were within historically normal ranges.

Also, if this theory is correct, you should see the coins with the lowest circulating supply get penalized, while the coins with higher circulating supply should do well. But we don’t see a strong correlation. They all fell.

So this lack of price discovery story sounds compelling, but after looking at the data, I’m not convinced.

Solutions, Solutions

While everyone is complaining, a few are proposing actual solutions. Let’s review them before we discuss the null hypothesis.

A lot of people are suggesting bringing back ICOs. Sorry — have we forgotten how ICOs were sold off after the listing and secondary markets collapsed? And ICOs are illegal almost everywhere, so I don’t think this is a serious suggestion.

@KyleSamani thinks investors and teams should unlock 100% immediately — which is impossible for US investors under Rule 144a (and would also fuel the “VC dumping” story). Also, I think we learned in 2017 why team vesting is a good idea.

@arca thinks tokens should have book runners like traditional IPOs. I mean, maybe that would work? Token issuance is more akin to direct listings, where you list on an exchange with some market makers and that's it. I think that's fine, but I prefer simple market structures with fewer intermediaries.

@reganbozman suggests projects should list their tokens at lower prices so retail investors can buy in earlier and win some upside. I get the idea, but I don't think it works. Artificially lowering the price below the market clearing price means whoever trades in the first minute of trading on Binance will capture the false underpricing. We've seen this multiple times with NFT mints and IDOs. Artificially lowering your listing price only benefits the few traders who fill their orders in the first 10 minutes. If the market thinks you're worth X, then in a free market you'll be worth X by the end of the day.

Some suggest we go back to fair launches. Fair launches sound good in theory, but don’t work well in practice because teams will simply pivot quickly. Trust me, everyone tried this during the DeFi summer. There aren’t a lot of success stories here — what other non-meme coins have had successful fair launches in the past few years besides Yearn?

Many people have suggested that teams do larger airdrops. I think there’s a lot of truth to this argument! We generally encourage teams to try to get more supply on day one to improve decentralization and price discovery. That said, I don’t think doing ridiculously large airdrops just for float is a smart move — a protocol needs to do a lot to do with its tokens to be successful after day one, and it’s not smart to hype yourself up on launch day to get huge float gains because you’re going to have to compete with token gains later. You don’t want to be one of those tokens that has to re-increase its token supply a few years later because your token coffers are empty.

So what do we as VCs want to see happen here? Believe it or not, token prices in year one reflect reality. We are not paid by price profit (paper profit), but by DPI, which means we have to convert tokens into cash eventually. We can't eat the paper markup, and we don't mark unvested tokens to market (anyone who does this is crazy in my opinion). It is actually a bad scheme for VC funds to reach astronomical valuations and then get stuck after we unlock. This makes LPs think that this asset class is a sham - while it looks good on paper, it is actually terrible. We don't want this. We want asset prices to rise gradually and steadily over time, which is what most people want.

So, are these high FDVs sustainable? I don’t know. These numbers are obviously eye-popping compared to what they were when projects like ETH, SOL, NEAR, and AVAX first launched. But crypto is definitely much bigger now, and the market potential for successful crypto protocols is clearly larger than it was in the past.

@0xdoug mentioned that it’s important to note that if you normalize last year’s altcoin FDVs to today’s ETH price, you get numbers very close to the FDVs we’re currently seeing. @Cobie echoed this in his recent post. We’re not going back to $40m L1 FDVs because everyone sees how big the market is now. But at the time of SOL and AVAX launch, the secondary market was paying comparable prices based on ETH-adjusted prices.

A lot of this frustration can be attributed to this: crypto has risen dramatically over the past 5 years. Startups are priced based on comparables, so the numbers are all going to be larger. That’s it.

Okay, so it’s easy for me to criticize other people’s solutions. But what’s my clever solution?

The honest answer?

Nothing. Leave it all to the market.

The free market will sort this out on its own. If the token goes down, then other tokens will re-price lower, exchanges will push back teams to launch new projects at lower FDVs, traders who were hurt by this cycle will just buy at lower prices, and VCs will pass this information on to new founders. Series B will be priced lower due to public market comparisons, which will punish Series A investors and eventually seed investors. Price signals always get sent that way in the end.

When there’s a true market failure, you may need some kind of clever market intervention. But the free market knows how to fix pricing errors — just change the price. Those who lose money, whether VC firms or retail investors, don’t need people like me to voice their thoughts or debate on Twitter. They have internalized this lesson and are only willing to pay less for these tokens. That is why all of these tokens are trading at a lower FDV and future token transactions will be priced accordingly.

This has happened many times before. It may only take a minute for the market to adapt.

4) Null Hypothesis

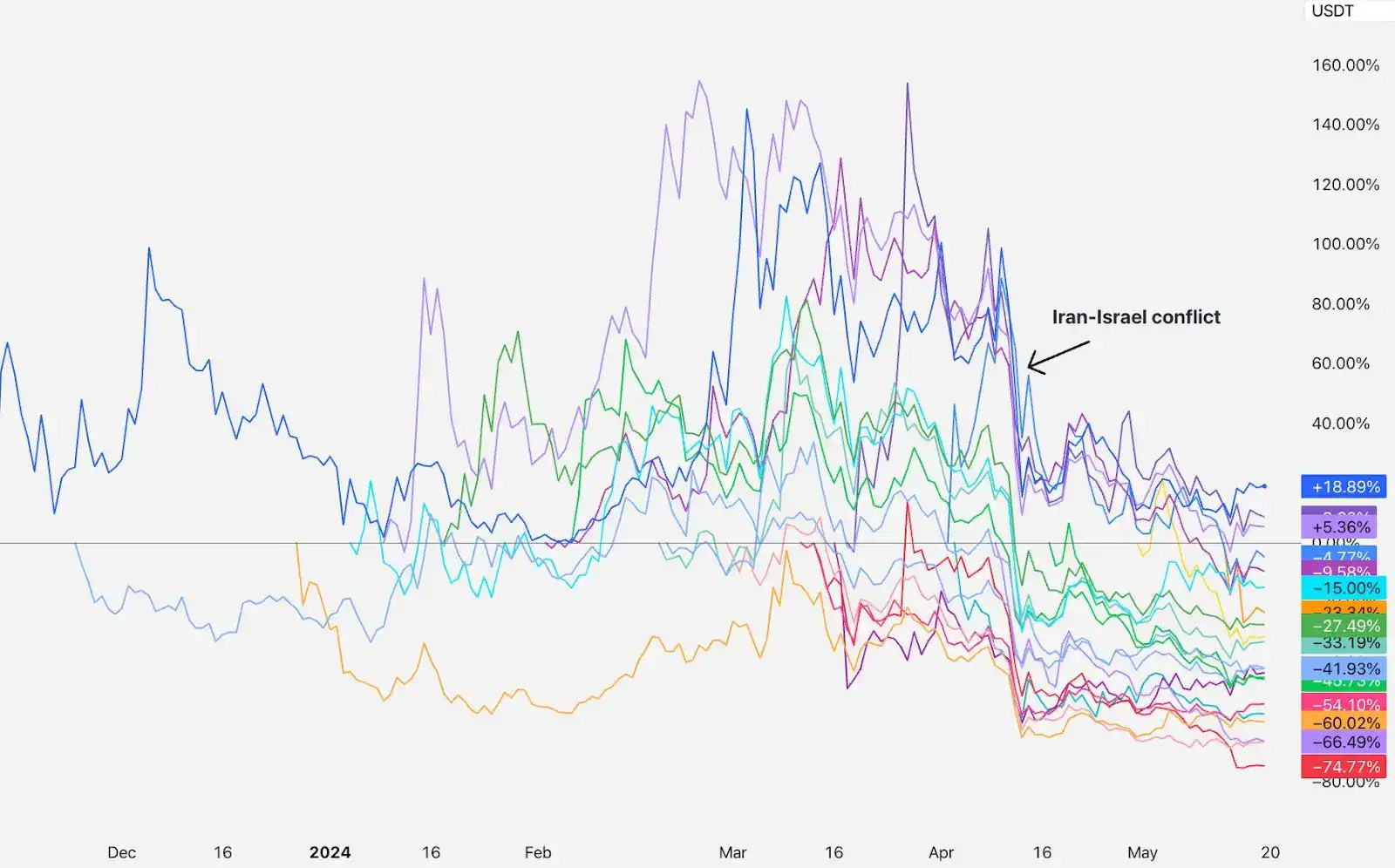

Now let’s unpack Scooby Doo. What happened to cause all of the tokens to drop in April?

The culprit: the Middle East.

For the first few months, these tokens traded mostly flat since listing, until mid-April. Iran and Israel suddenly started threatening World War III, and the market plummeted. Bitcoin prices recovered, but these tokens did not.

So what’s the best explanation for why these tokens are still down? My explanation is this: These new projects are all psychologically categorized as “risky new coins.” Interest in the “risky new coin basket” dropped in April and has not recovered. The market doesn’t want to buy them back now.

Why?

I don’t know. Markets are fickle at times. But if this basket of “risky new coins” had risen 50% during this period, instead of falling 50%, would you still argue how the token market structure was broken? It would also be a mispricing, just in the opposite direction.

A mispricing is a mispricing, and the market will eventually fix it. If you want to help — sell things at crazy prices, and buy things at better prices. If the market is wrong, it will fix itself. No need to do anything else.

What to do?

When people lose money, everyone wants to know who to blame. Is it the founders? VCs? KOLs? Dealers? Market makers? Traders?

I think the best answer is no one or everyone. But thinking about market mispricing in terms of blame is not a productive framework. So I’ll frame it in terms of how people can do better in this new market regime.

VCs: Listen to the market and slow down. Show pricing discipline. Encourage founders to be realistic about valuations. Don’t peg your lockup to the market (almost all the top VC firms I know hold lockups at a significant discount to the market price). If you find yourself thinking “I can’t lose money on this trade”, you’re probably going to regret this trade.

Exchanges: List new coins at lower prices. But you already knew this. Consider using public auctions to price day one tokens instead of pricing based on last VC round valuations. Don’t list new coins unless all investors/teams have a contractual obligation not to hedge, and unless everyone (including KOLs) has a market standard lockup period. Better show retail investors the FDV burndown chart we all know and love, and educate them more about unlocking.

Teams: Try to have more tokens in circulation on day one! Token supply below 10% is too low.

Of course, have healthy airdrops and don’t be too scared of a low FDV on day one. The best price chart to build a healthy community is a gradual upward trend.

If your team’s token has fallen, don’t worry. You have good precedent to follow. Remember:

AVAX fell ~24% 2 months after listing;

SOL fell ~35% 2 months after listing;

NEAR fell ~47% 2 months after listing.

You will be fine. Focus on building something you are proud of and keep delivering. The market will eventually figure it out.

For you, be careful of single cause and effect explanations, which are often not very accurate. Markets are complex and sometimes they go down. Be suspicious of anyone who claims to confidently know why. DYOR and don't invest anything you are not willing to lose.

Finally:

Thank you @EvgenyGaevoy for reviewing a draft of this post.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia