Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

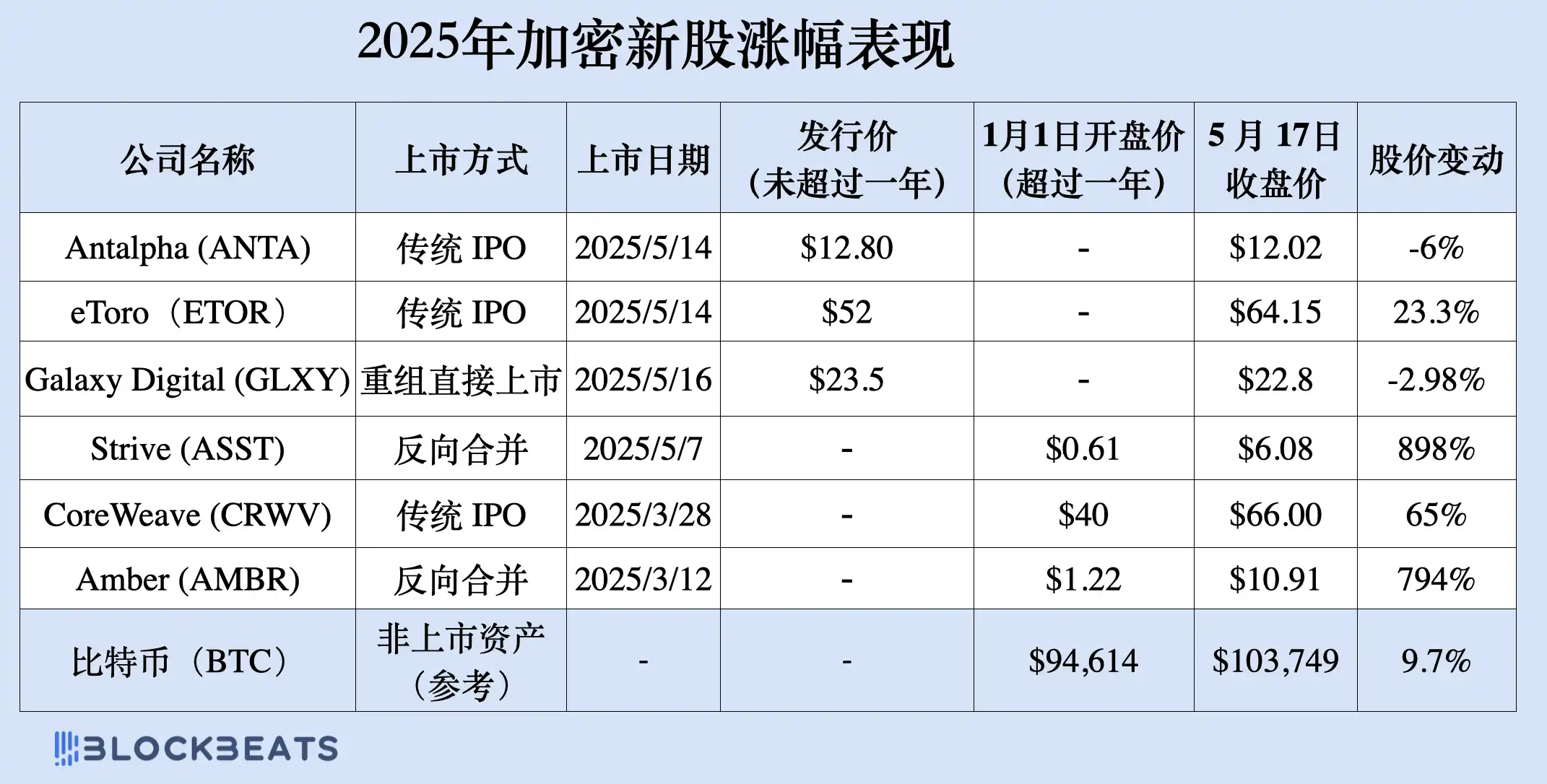

Outperforming Shitcoins in Price Surge, Can You 10x in Crypto's New Wall Street?

The cryptocurrency stocks that went public this year have seen a significant increase, far surpassing 90% of meme coins and dog coins.

After a lackluster performance in the first quarter of the year, the cryptocurrency market finally saw some gains in May. While Bitcoin saw a modest rise of about 9.7% amidst the volatility, what many don't know is that it's the batch of "crypto newcomers" that landed on Nasdaq this year that has outperformed Bitcoin and even most meme coins over these past few months. Antalpha triggered a circuit breaker on its listing day, eToro closed up 23%, Amber Premium surged nearly 8x in the first quarter, and Strive, which completed a reverse merger, skyrocketed over 10x in just five months.

In this article, BlockBeats will dissect these 2025's most representative publicly traded crypto companies based on financial report data, stock performance, and business models.

Antalpha

On May 14, 2025, Antalpha officially landed on the Nasdaq Global Market through an Initial Public Offering (IPO) with the stock code "ANTA." The IPO price was set at $12.80 per share, with a total of 3,850,000 common shares issued. On its first day of trading, the stock price surged by 73.59%, triggering a circuit breaker and making it one of the most eye-catching new listings on the market recently.

Antalpha is a crypto fintech company focusing on Bitcoin mining financial services. Its core mission is to provide structured financing and risk management solutions for the global Bitcoin industry chain. The company primarily serves miners, mining hardware manufacturers, and their upstream and downstream ecosystem. Its business ecosystem includes supply chain financing, settlement networks, risk control platforms, and technology service outputs. Specifically, Antalpha provides Bitcoin miners with equipment procurement and operational funding, and through its Antalpha Prime technology platform, it achieves real-time monitoring of collateral positions, strengthening asset security and liquidity management. In terms of industry collaboration, Antalpha is also Bitmain's key lending partner, deeply integrated into the mining ecosystem. Additionally, the company has partnered with Mantle to launch FBTC, an EVM-compatible Bitcoin-pegged asset, and collaborated with Cobo in 2023 to establish standardized solutions in custody and asset security.

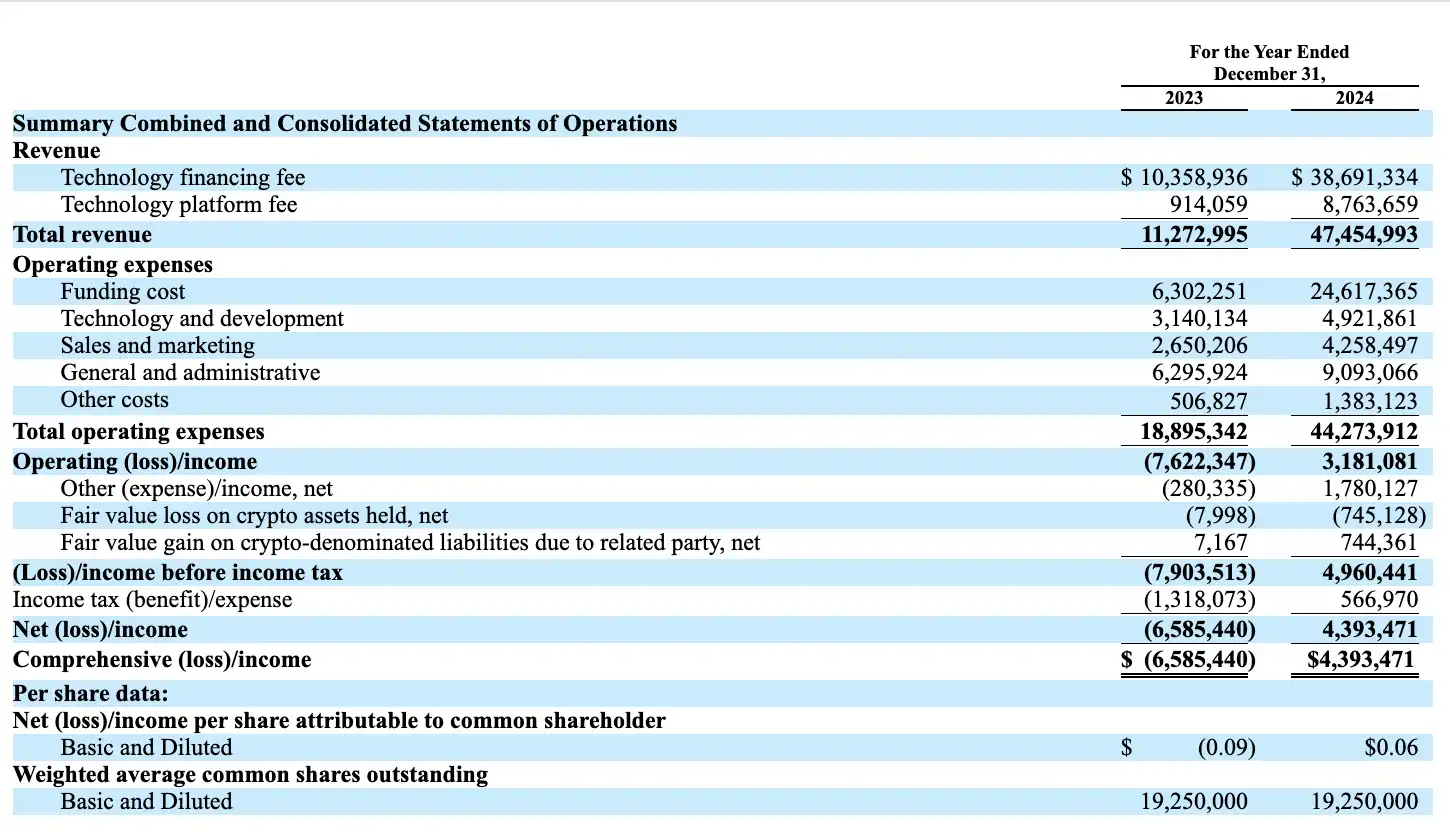

In 2024, Antalpha achieved a total revenue of $47.45 million, showing a 321% growth compared to $11.27 million in 2023, demonstrating its strong business expansion capabilities. Its revenue structure also exhibits an increasingly clear dual-engine model feature:

On one hand, Technology Financing Fee revenue surged from $10.35 million to $38.69 million, nearly tripling. This growth was mainly driven by the company's participation as an institutional funder in structured financing, collateralized lending, and settlement services, reflecting its increasing market acceptance as a "Bitcoin financial plumbing" role.

On the other hand, Technology Platform Fee revenue also saw a significant leap, increasing from $0.91 million to $8.76 million, a staggering 859% year-over-year growth. This growth primarily came from Antalpha packaging its fund routing system, risk monitoring API, SaaS platform, and other core capabilities for external offerings, demonstrating not only its financial execution capability but also its gradual development of a scalable replicable technology service business.

These two revenue streams together form the fundamental business loop of Antalpha as a compliant crypto infrastructure service provider: on one hand, providing liquidity to the industry through structured financing, being seen as the "plumber" of Bitcoin finance; on the other hand, platformizing its technological capabilities to create a programmable, integrable "infrastructure as a service" toolchain.

Alongside the rapid growth in revenue scale, the company's operating expenses have also significantly increased. The full-year operating costs for 2024 reached $44.27 million, a growth of approximately 135% from $18.89 million in 2023. Among them, financing costs increased from $6.3 million to $24.62 million, in high alignment with the platform's asset scale expansion; technology R&D expenses reached $4.92 million, a 57% year-over-year growth, showing the company's continuous investment in its technology stack; and marketing and administrative expenses totaled around $13.35 million, primarily used for business expansion, compliance architecture development, and IPO-related preparations.

Despite the rapid cost escalation, thanks to the release of scale effects, the company achieved an operating-level turnaround in 2024, with a full-year operating profit of $3.18 million, compared to a loss of $7.62 million in the same period the previous year.

Built on the operating profit, considering other income and expenses, the company achieved a net profit of $4.39 million, successfully making a key turning point from loss to positive profitability. In addition, the performance of non-core business segments played a supportive role: other net income amounted to $1.78 million, mainly including interest income and valuation gains on coin-based liabilities; meanwhile, due to some crypto asset price fluctuations, the company recognized a fair value loss of $0.74 million but also received an equivalent valuation hedge gain from related-party coin-based liabilities. Overall, these non-operating items did not substantially suppress profits but instead provided some financial cushioning amid fluctuations.

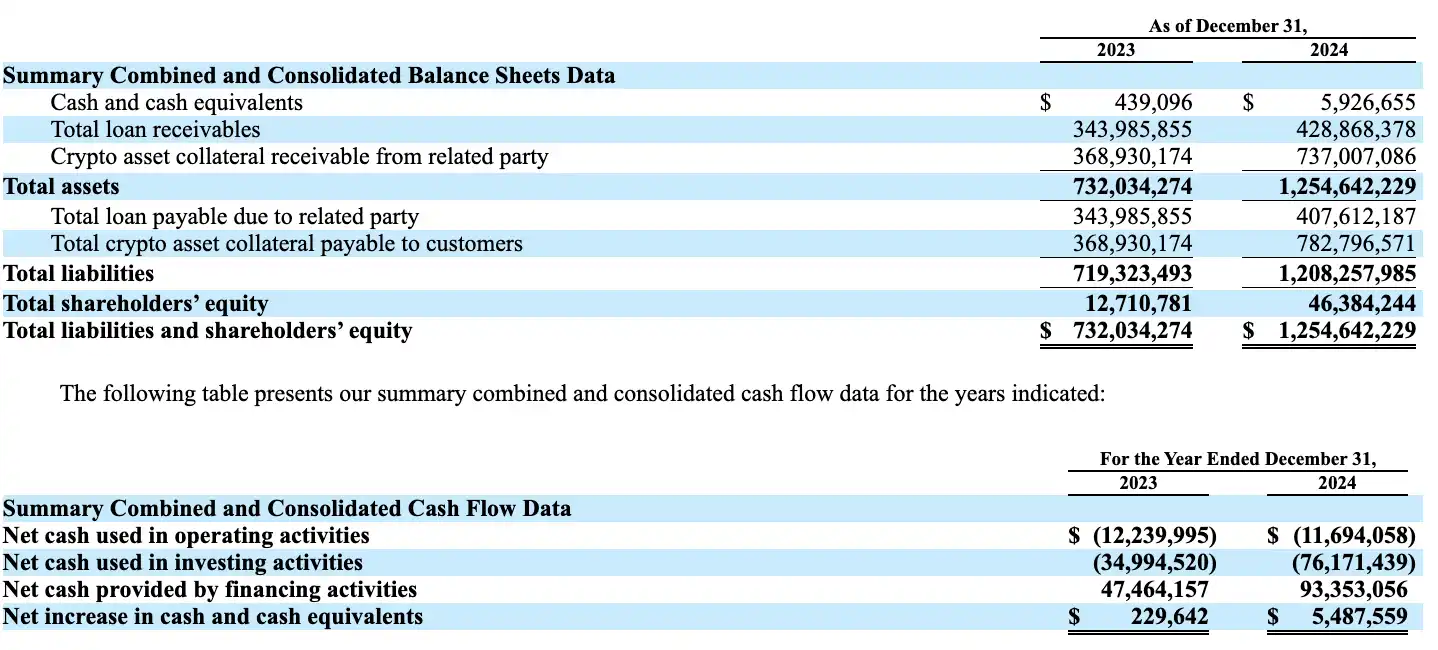

From an asset-liability perspective, as of the end of 2024, Antalpha's total assets had reached $1.25 billion, a 71% increase from $730 million in 2023. The crypto asset collateral receivables had soared from $370 million to $737 million, reflecting the rapid expansion of on-chain collateral assets held by the platform as a lending matchmaker. At the same time, loan receivables also rose to $429 million, indicating a significant enhancement in the activity level of the funding supply side.

On the liability side, total liabilities increased from $719 million to $1.208 billion, mainly driven by platform customer coin-based borrowings and collateral obligations. This growth was in basic alignment with the asset side, with no significant liquidity mismatch risk observed. Meanwhile, shareholder equity rose from $12.71 million to $46.38 million, reflecting the steady accumulation of net assets driven by business growth and ongoing profitability, laying a solid foundation for future financing and capital operations.

In terms of cash flow, Antalpha's operating cash flow in 2024 showed a net outflow of $11.69 million, investment cash flow outflow of $76.17 million, indicating that the company is still in a high-input, high-growth stage. However, through active financing activities, the company obtained a net financing fund of $93.35 million for the year, with a net cash increase of $5.48 million for the year, ending the year with a cash and cash equivalents balance of $5.92 million, maintaining a robust liquidity position.

To further demonstrate operational efficiency and true profit-making ability, Antalpha disclosed a non-GAAP financial metric—Adjusted EBITDA. After excluding income tax, depreciation, amortization, and equity incentives, this indicator improved significantly from -$7.57 million in 2023 to +$5.91 million in 2024, showing that the company's core operating model has been continuously optimized and has successfully entered the profit realization stage.

Galaxy Digital

Galaxy Digital is a comprehensive digital asset service company spanning the cryptocurrency financial and traditional capital markets, founded by former Goldman Sachs partner Mike Novogratz in 2018. Since its inception, Galaxy has sought to build a "next-generation Morgan Stanley," with core businesses covering asset management, cryptocurrency trading, market making and lending, investment banking services, structured products, and emerging sectors such as rapidly growing data centers and AI high-performance computing leasing.

The listing path of Galaxy is quite representative. Back in 2018, Galaxy went public through a reverse takeover with a Canadian shell company Bradmer Pharmaceuticals, listing on the TSX Venture Exchange in Toronto with the stock symbol GLXY. As the regulatory environment matured and compliance framework was established, starting in 2022, Galaxy began a structural reorganization, initiating a complex Up-C structure design. It moved its domicile from the Cayman Islands to Delaware, USA, and set up a new holding entity, Galaxy Digital Inc., as a publicly traded company soon to be listed on Nasdaq.

This Up-C model allows the company to retain the flexibility of its existing partnership structure while achieving transparency for public shareholders and optimizing the voting rights structure. It is a standard restructuring path adopted by U.S. new economy companies like Coinbase and Robinhood before their IPOs. It reflects how companies in the cryptocurrency industry have navigated past traditional regulatory barriers over the past few years to gradually move towards the mainstream capital market.

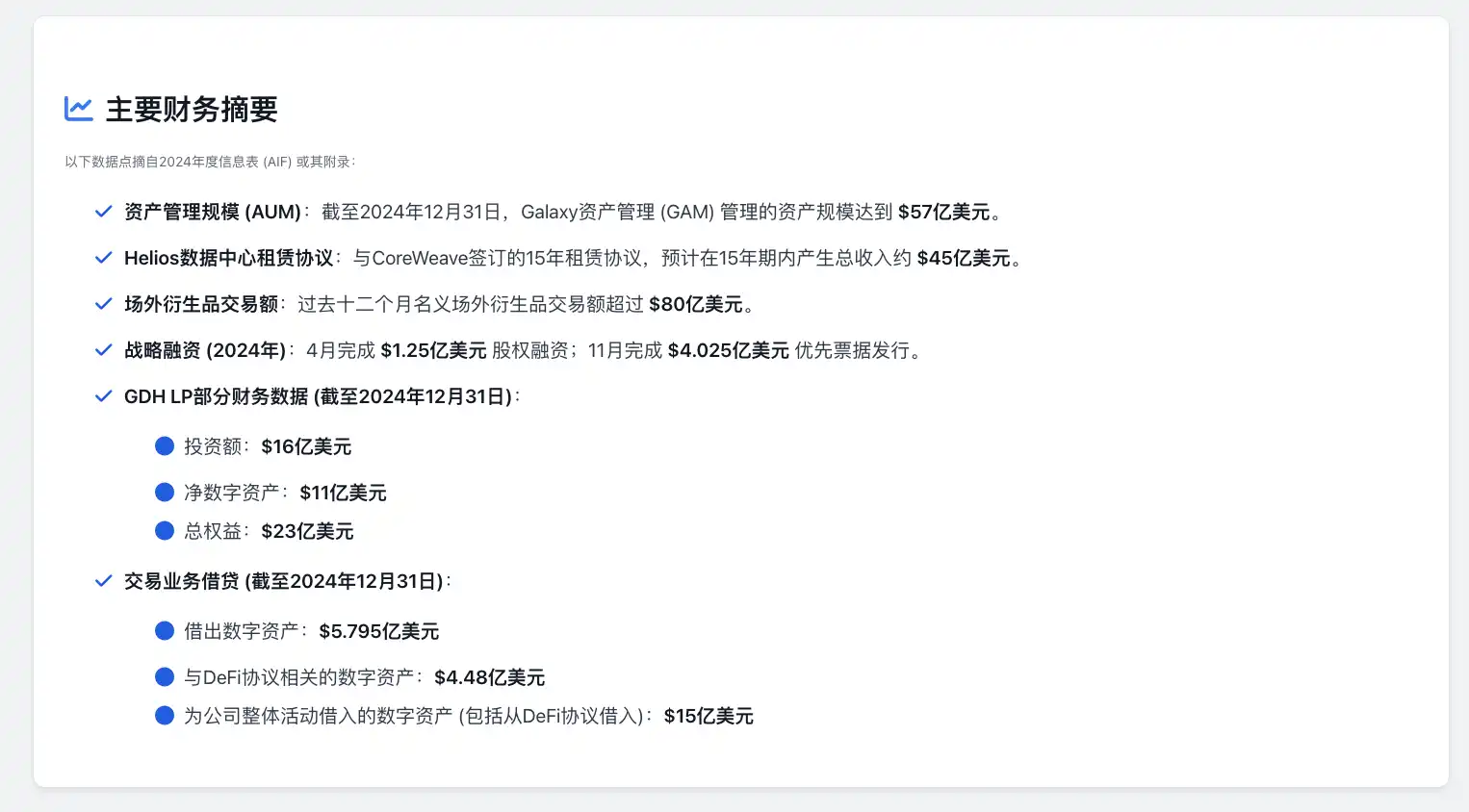

Asset management was one of Galaxy's standout sectors in 2024. The full-year assets under management (AUM) grew to $5.7 billion, reaching a historical high. Of this, $3.5 billion came from ETF products issued in collaboration with global traditional financial giants such as Invesco and State Street, while $2.2 billion consisted of alternative investment portfolios like hedge funds and venture capital funds under Galaxy. Galaxy launched the Bitcoin Spot ETF (BTCO) and Ethereum Spot ETF (QETH) in collaboration with Invesco early in the year, swiftly penetrating the U.S. mainstream market. At the same time, Galaxy also partnered with State Street to launch three crypto ecosystem-themed ETFs, covering indices related to decentralized technology and Web3.

Furthermore, Galaxy launched the multi-asset hedge fund product Galaxy Absolute Return Fund during the year. It is a fund portfolio designed for institutional investors, emphasizing a non-coin exposure strategy. Regarding trading and derivatives business, detailed annual trading revenue data was not disclosed in the annual report. However, Galaxy highlighted its continuous investment in product diversity, institutional service depth, and compliance capabilities. It introduced several new cryptocurrencies and leveraged trading products, enriching the derivatives platform's trading tools.

Additionally, Galaxy has been continuously expanding its presence in blockchain infrastructure services, including node custody services, RPC interface products, multi-chain validation services, etc. It is gradually building a product system of "Financial Infrastructure as a Service" and exploring the opening of these services to projects and developers in a Software as a Service (SaaS) model. By the end of 2024, Galaxy's organizational scale continued to expand. Apart from its headquarters in New York, the company has local teams in London, Tokyo, Hong Kong, Singapore, and other locations, with a total workforce of hundreds of employees, with recruitment focused on asset management, infrastructure operations, and compliance teams.

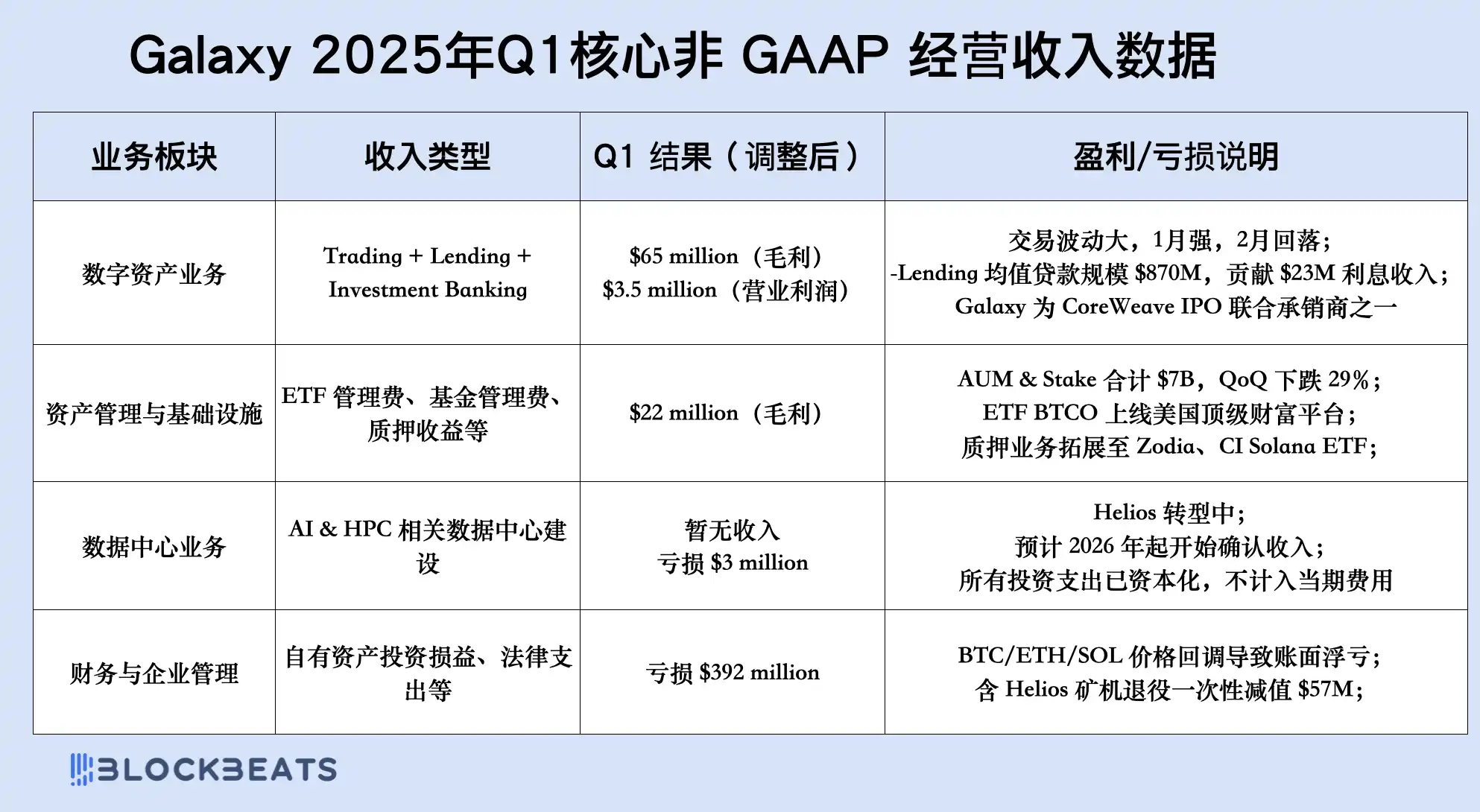

Starting from Q1 2025, Galaxy also completed a restructuring of its financial report structure, consolidating the original three major business lines into two operating segments and one corporate segment to better align with its strategic focus. The "Digital Assets" segment brings together all services related to native cryptocurrency businesses, such as trading, investment banking, asset management, and infrastructure development (including staking, tokenization, and custody technology); the "Data Centers" segment independently presents the long-term value and transformation progress of the Helios project, with revenue expected to be recognized starting in early 2026; the "Treasury and Corporate" segment mainly includes the impact of investment holdings on the balance sheet and the remaining mining operations and other non-operating projects.

In Galaxy Digital's Q1 2025 financial report, the company disclosed its total revenue under GAAP of $12.98 million. This figure stems from the U.S. Generally Accepted Accounting Principles (GAAP) treatment of digital asset transactions with a "gross-up" approach, which requires the total amount traded between customers to be separately recorded as revenue and expenses, rather than just recording the actual price difference or fees earned. Although this accounting method complies with regulatory requirements, it does not accurately reflect the company's profitability and can instead magnify revenue figures, especially in a company like Galaxy that combines asset management, financial services, and digital infrastructure.

To more accurately present its operational performance, Galaxy concurrently disclosed non-GAAP metrics—Adjusted Gross Profit—as its primary internal management and external communication reference.

In Q1 2025, Galaxy's total non-GAAP operating revenue reached $87 million, including $65 million from digital asset-related businesses and $22 million from asset management. This revenue mainly comes from proprietary trading, Prime brokerage, structured credit, ETF management fees, and fund income, constituting a stable and sustainable source of cash flow for the company, further demonstrating the ongoing effectiveness of its "Trading-Investment Management-Infrastructure" integrated operating system.

After deducting the corresponding costs, Galaxy recorded a net operating profit of $3.5 million, mainly contributed by the digital asset business. This achievement, amidst the overall turbulence and adjustment period in the crypto market, showcases the resilience and scalability of its core business.

However, the GAAP financial statements show a net loss attributable to shareholders of $295 million for this quarter, which was not due to a decline in core business performance, but rather was caused by two non-recurring items: first, a temporary pullback in the prices of core holding assets such as BTC and ETH in Q1, resulting in unrealized losses on the balance sheet; second, Galaxy retired and restructured old mining rigs for the Helios project, booking a one-time substantial asset impairment charge. While these non-operating losses depressed the profit performance on the financial statements, they did not impact Galaxy's cash flow or the quality of its core operations.

Galaxy Digital's revenue structure in the first quarter of 2025 demonstrates its increasingly mature and diversified operational framework. The Trading and Lending businesses continue to play the core roles in cash flow generation. In January, with a strong market rebound, Galaxy's proprietary trading and client matching businesses saw significant returns, but as February began, cryptocurrency prices stabilized, volatility decreased, and trading volumes subsequently declined, exerting some restraint on the trading business. Nevertheless, its Lending segment continued to experience steady growth, with a total loan balance reaching $870 million, a 25% increase from the previous quarter, driven mainly by institutional clients' growing demand for structured financing and liquidity. The Lending business contributed $23 million in interest income this quarter, reflecting Galaxy's significant achievements in the deployment of stable yield assets.

On the asset management front, although the market downturn reduced the total assets under management and staking to $7 billion, a nearly 30% decrease from the previous quarter, management fee income remained robust, demonstrating strong client stickiness and product moat. The Bitcoin spot ETF—BTCO, jointly issued with Invesco, successfully onboarded multiple top-tier wealth management platforms in the first quarter, covering a cumulative asset base of over $2 trillion. This marks the true integration of Galaxy's ETF products into mainstream compliant funds. Additionally, its Galaxy Crypto Venture Fund II, a crypto venture capital fund, raised over $160 million in this quarter, indicating that it still possesses significant capital appeal in the primary market.

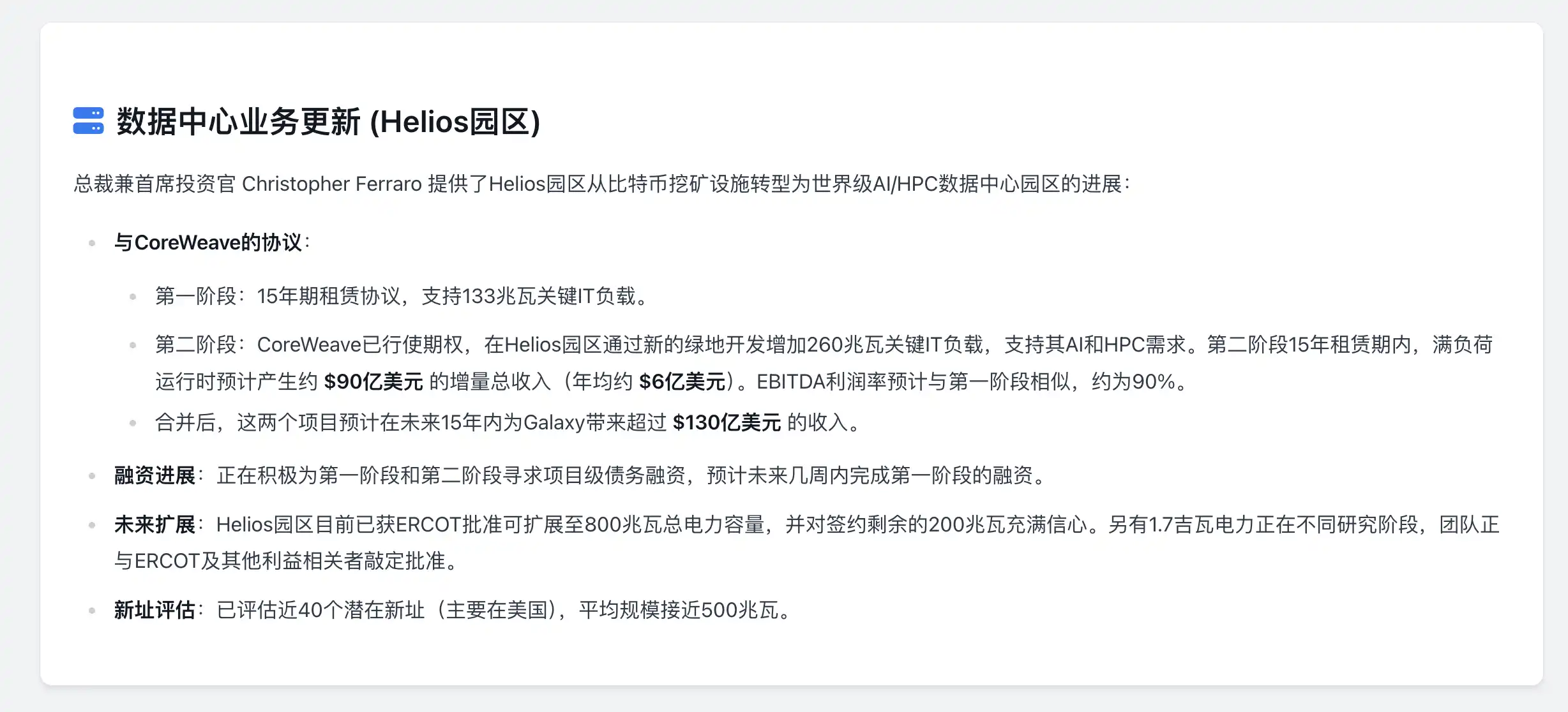

Of note is Galaxy's development of the AI Data Center business, namely the Helios project located in Texas. While this segment has not yet begun recognizing revenue this quarter, its transformation process has reached a critical stage. The project has deployed a total of 393 megawatts of computing power in the first two phases and has entered into a 15-year long-term lease agreement with the AI infrastructure leader, CoreWeave. Based on the agreement, this data center is projected to generate approximately $1.3 billion or even higher cumulative revenue for Galaxy over the next fifteen years. Currently, these expenses are considered capital investments, not affecting the current period's profits, but they are evidently a key part of Galaxy's growth trajectory in the next phase.

Meanwhile, this quarter, Galaxy reported a net loss of $295 million, mainly stemming not from its core business, but from mark-to-market losses due to the digital asset market price pullback and asset impairment from the retirement of old mining machines in the Helios project. These non-operating items amounted to $392 million in total, although they suppressed GAAP net profit, they did not actually impact its operating revenue and cash flow performance. From a non-GAAP perspective, Galaxy's core operating profit remains stable, with segments such as asset management, trading, lending, fund issuance, etc., continuing to generate structural income.

One could say that this quarter's financial report is a transformation window for Galaxy to fully "sync with Wall Street" from operations to accounting standards. Looking at it from the GAAP financial statement, it is a company under pressure in market volatility; however, from a non-GAAP standpoint, Galaxy is steadily building a global multi-asset platform with stable cash flow, a wide range of financial product lines, and an AI data center as a medium- to long-term pivot.

eToro

eToro completed its IPO pricing on May 14, 2025, and officially listed on Nasdaq on May 15 (stock symbol ETOR), selling 6 million shares at a price of $52 per share, raising approximately $312 million from investors. The valuation of the company from this listing was $4.2 billion. The platform, founded in Israel in 2007, focuses on providing social trading services for various assets such as cryptocurrencies, stocks, ETFs, positioning itself as a competitor to Robinhood.

Previously, eToro attempted to go public through a SPAC merger (valued at $10.4 billion in 2021), but due to changes in the market environment, the plan was terminated in 2022. It is worth noting that a BlackRock-affiliated fund had already committed to subscribing to $100 million worth of shares at the IPO price, demonstrating institutional investors' high interest in the Web3 space.

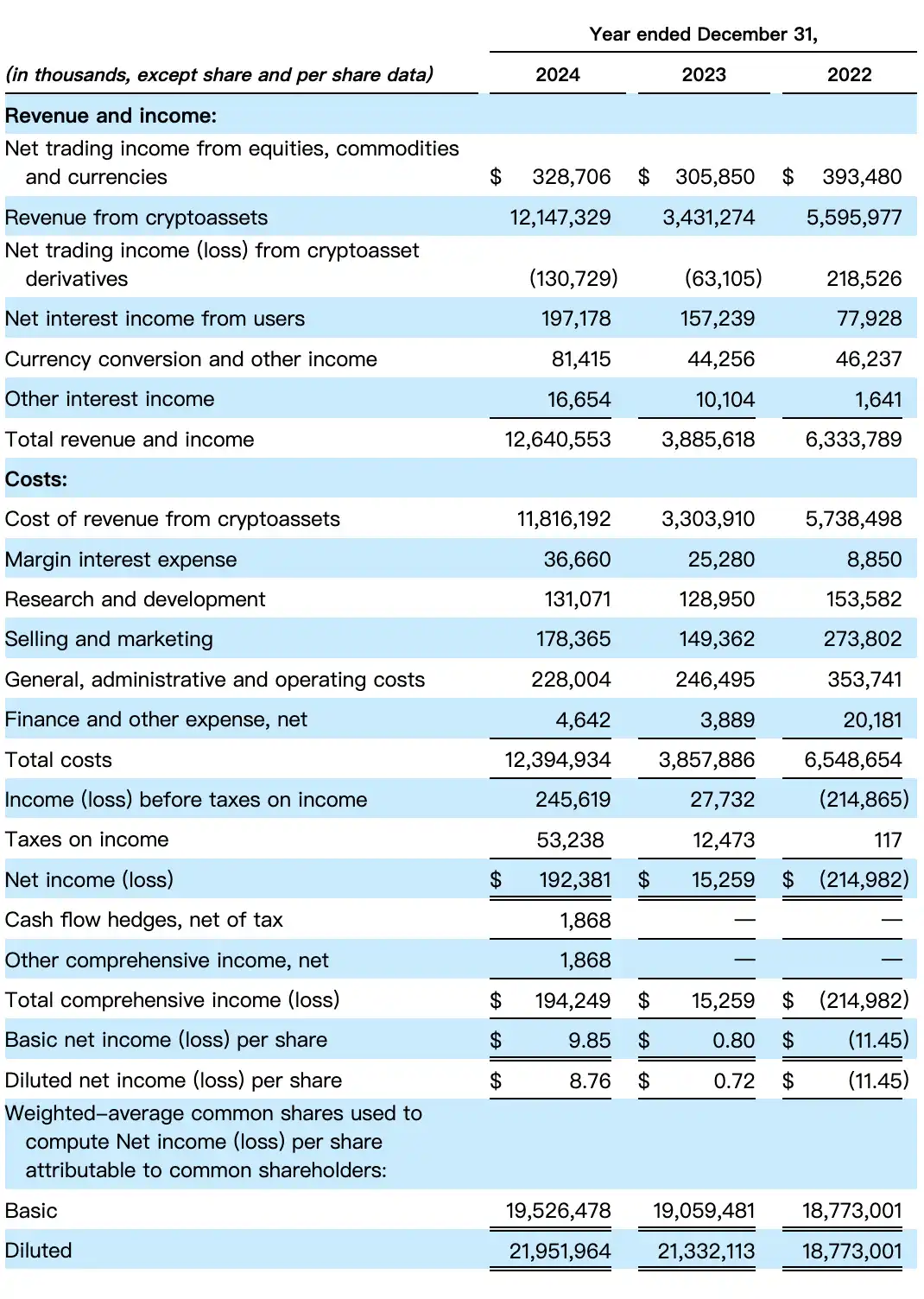

eToro's total revenue and other income in 2024 amounted to $12.64 billion, more than triple that of 2023 ($3.89 billion) and far exceeding 2022's $6.33 billion. Among these, revenue from cryptocurrency trading was the primary contributor, reaching $12.147 billion, accounting for over 96%, whereas this revenue in 2023 was only $3.431 billion, indicating a significant increase in the platform's market share in this round of the crypto market.

In the non-crypto asset business, eToro also maintained robust growth: Net revenue from stocks, commodities, and forex trading reached $3.29 billion; Net interest income from users $1.97 billion, a year-on-year increase of about 25%; Currency conversion and other revenue $81.41 million; Other interest income $16.65 million.

At the same time, it is worth noting that the cryptocurrency derivatives trading division recorded a net loss of $131 million in 2024, which is related to its risk exposure management and partly to its volatility trading strategy, also reflecting the double-edged sword nature of the cryptocurrency leveraged market.

While eToro saw significant revenue growth, its expenses also expanded noticeably. Total costs for the full year 2024 reached $12.39 billion, including: Crypto asset cost of revenue (i.e., counterparties and market execution fees) $11.816 billion, nearly tripled year-on-year; Sales and marketing expenses reached $178 million, a 20% year-on-year increase, mainly used for user acquisition, brand expansion, and pre-IPO market investment; General and administrative expenses were about $228 million, slightly lower than the $246 million in 2023; Research and development expenses were $131 million, maintaining a relatively stable level; Margin interest expenses, financial charges, etc., were minor cost items, totaling about $49 million.

Despite the substantial increase in total costs, due to revenue growth far exceeding the increase in costs, eToro's profitability made a significant leap this year.

Driven by strong revenue, eToro achieved a pre-tax profit of $2.45 billion, nearly 9 times that of 2023 ($277.3 million). After deducting $53.24 million in income tax, net profit was $1.92 billion, compared to a net profit of only $152.5 million in the previous year, and a loss of $215 million in 2022.

CoreWeave

CoreWeave, formerly known as Atlantic Crypto (founded in 2017), initially focused on providing GPU mining infrastructure for cryptocurrencies like Ethereum. With Ethereum's shift to a PoS consensus mechanism in 2022, it rapidly recalibrated its strategy, redirecting its GPU cluster, originally used for mining, towards graphics rendering and AI training, seizing the opportunity of the Generative AI boom, and becoming a company specializing in AI cloud computing services, with hosting partnerships with various crypto mining enterprises.

CoreWeave went public on Nasdaq on March 28, 2025, under the ticker symbol "CRWV," raising $15 billion with a market valuation of approximately $230 billion. Despite a lackluster performance on the first day of trading, the company's strategic positioning in the AI infrastructure sector has garnered significant attention. NVIDIA, as a strategic investor, subscribed to $2.5 billion worth of shares, earning CoreWeave the nickname "NVIDIA's prodigal son" in the US stock market.

On May 14, CoreWeave released its first post-IPO financial report, revealing revenue growth far exceeding analysts' expectations.

Revenue: For the quarter ending on March 31, revenue reached $9.816 billion, a staggering 420% year-over-year increase (compared to $1.887 billion in the same period last year), well above the market's expected $8.53 billion;

Earnings Per Share: A net loss of $1.49 per share, with the net loss amount expanding from $1.292 billion in the same period last year to $3.146 billion, partly due to $177 million in equity compensation expenses related to the IPO;

Business Growth: While the full-year revenue growth in 2024 was 737%, this quarter saw a slight slowdown but still maintained triple-digit high growth.

In terms of business model, CoreWeave provides GPU rental services to enterprises, competing with tech giants like Amazon Web Services. However, industry leaders such as Google and Microsoft have become key customers for CoreWeave, with Microsoft contributing 62% of the company's revenue in 2024 ($19.2 billion).

Of note, this quarter, OpenAI signed a five-year cooperation agreement with CoreWeave worth up to $11.9 billion, on top of its reliance on Microsoft (which contributed 62% of CoreWeave's revenue in 2024), highlighting its critical position in the AI computing power sector.

Strive Asset Management

Strive Asset Management completed its Nasdaq listing on May 7 through a reverse merger with Asset Entities Inc. (NASDAQ: ASST), with the final merger agreement rebranding the merged entity as "Strive" for continued trading on Nasdaq. Post-transaction, Strive holds 94.2% of the new company's shares, and former CEO Matt Cole assumes the role of Chairman and CEO.

Strive was founded by Vivek Ramaswamy, co-leader of the US government efficiency department DOGE, with investors including vice presidential candidate JD Vance, who has close ties to the Trump camp. The company is seen as a key player driving the "Bitcoin Strategic Reserve".

Strive Asset Management has applied to US regulatory agencies for approval to list an exchange-traded fund (ETF) investing in a convertible bond issued by MicroStrategy and other companies. The ETF aims to provide exposure to "Bitcoin Bonds," described as "convertible bonds issued by MicroStrategy or other companies," with these companies planning to "use all or most of the proceeds to purchase Bitcoin."

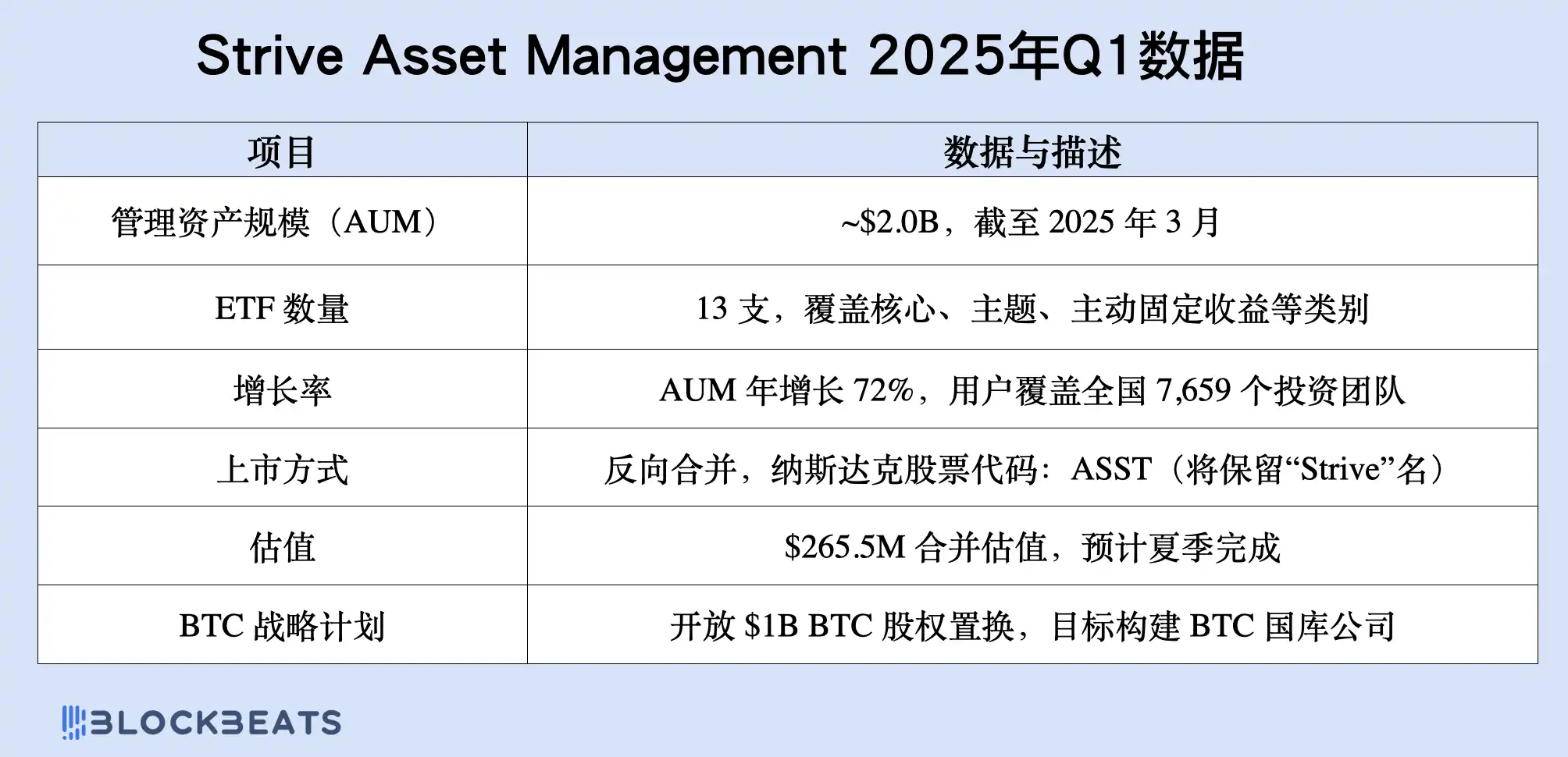

As of the first quarter of 2025, Strive's assets under management (AUM) have reached approximately $2 billion, a year-over-year growth of over 70%. Strive's core business is built around ETF products, and in less than three years, the company has launched 13 ETFs covering core index strategies, thematic investments, and actively managed fixed income funds.

These ETF products have become its primary recurring revenue source, rapidly expanding to over 7,000 registered investment advisor (RIA) teams and entering multiple corporate 401(k) retirement platforms, especially after gaining retail market recognition. At the same time, the company has made breakthroughs in technology platform services, starting to provide "technology platform fees" revenue to high-net-worth clients and institutions through direct investment portfolios, customized index services, and tax optimization tools, which has become its new revenue growth curve.

Although the company has not yet released full GAAP financial statements, its revenue structure is becoming increasingly clear based on its investor documents released in May 2025. The focus on the expenditure side is primarily on organizational expansion and marketing, highly relying on social media and content operations for market penetration. The TikTok and Discord community users have exceeded 200,000 and have annual interactions in the tens of millions. Additionally, as Strive prepares to go public, expenses in compliance, personnel, and listing architecture have also significantly increased, constituting its main operating cost items.

Upon completion of the merger, Strive launched a groundbreaking financial engineering plan: opening a $1 billion Bitcoin equity buyback window. Through IRS Section 351, the company allows Bitcoin holders to exchange BTC for Strive equity without triggering capital gains tax. This mechanism is called "Bitcoin Balance Sheet Engineering," with the aim not only to hodl Bitcoin but to convert BTC into a foundational anchor for company valuation, creating a capital allocation platform supported by BTC as a reserve asset and stable income stream.

Furthermore, Strive has formally established Bitcoin as the internal "Capital Deployment Hurdle Rate" within the company, meaning that any investment decision, M&A transaction, or financing activity must be evaluated based on the criteria of "whether it can outperform BTC's long-term annualized return." At the core of this concept is the company's unwavering belief in the Bitcoin standard economy: if a capital appreciation return higher than BTC's cannot be achieved, then the activity is not worth pursuing.

Transitioning from a cutting-edge ETF issuer to a compliance-focused platform building a "Bitcoin Asset Treasury" model, Strive's transformation can be described as nothing short of "radical." However, looking at its capital structure, business performance, and user community engagement, it is reshaping the boundaries of an asset management firm in a way that diverges from traditional Wall Street.

Amber Premium

Founded in 2017 and headquartered in Hong Kong, Amber Group is a global crypto finance service provider. On March 12, 2025, Amber International (branded as Amber Premium), the crypto financial institution services and solutions provider under the Amber Group, completed a merger transaction with iClick Interactive Asia Group Limited and began trading on the Nasdaq Global Market under the stock symbol "AMBR."

As the core subsidiary of Amber Group, Amber Premium will leverage its proprietary blockchain and financial technology, AI-driven risk management, as well as the market experience and influence gained over the years by Amber Group. Amber Premium will continue to strengthen its execution services, expand compliance products, and promote the institutional-level development of digital asset finance through enhanced institutional partnerships and strengthened regulatory security.

In 2024, Amber International is still undergoing a crucial transitional period of large-scale strategic transformation. From a financial performance perspective, while the overall company is still operating at a loss, signs of improvement in several key metrics are beginning to emerge, especially as the growth potential of new business segments is starting to unfold.

Starting with the revenue side, Amber achieved a continuous operating income of $32.806 million in the year, a decrease of approximately 9% from $36.051 million in 2023. This decline was mainly influenced by the macroeconomic environment, particularly the tightening of marketing budgets by advertisers, causing a 13% year-on-year decrease in revenue from the marketing solutions segment, one of the company's main revenue sources. However, the enterprise solutions segment still saw slight growth in revenue, indicating that the digital service demand has partially offset the downward risk of the traditional advertising business. At the same time, the company maintained good cost control capabilities, with an annual gross profit of $16.747 million and a gross profit margin of about 51.0%, almost on par with the previous year's 52.9%, demonstrating that despite revenue fluctuations, the overall profitability quality of the company remains stable.

However, on the expense side, Amber's operating costs saw a significant increase, with total operating expenses rising from $30.725 million in 2023 to $34.107 million, representing a year-over-year increase of about 11%. The cost structure underwent a more dramatic change: Sales and marketing expenses plummeted from $17.28 million to $7.118 million, a compression rate of over 59%, indicating a conscious effort by the company to shrink traditional promotional expenses and transition to more efficient marketing methods. However, the saved marketing expenses did not fully translate into profit margins. The largest expense growth occurred in general and administrative expenses, which soared from $10.838 million to $26.058 million, a staggering year-over-year increase of about 140%. This was mainly due to one-time costs related to the Amber DWM acquisition, such as legal, audit, compliance, and personnel expenses. Research and development expenses remained relatively stable at $8.78 million for the year, slightly down from the previous year, indicating that the company maintained rational control over its technology investments.

In the non-operating segment, the company also faced a $72.1 million net loss, much higher than the $22.99 million in 2023. This loss may involve impairment of long-term investments, losses due to exchange rate fluctuations, and additional costs incurred during the Amber DWM acquisition process. After considering interest income and expenses, Amber's pre-tax operating loss for the year expanded to $24.07 million ($13.03 million in 2023). Ultimately, the net loss attributable to common shareholders was $23.935 million, equivalent to a loss of $2.61 per ADS, with an expanding year-over-year loss margin, reflecting the concentrated financial pressure arising from the merger transformation.

Furthermore, the company has gradually exited the mainland China market since 2023, and the related discontinued operations continued to drag down performance in 2024, resulting in a net loss of $5.104 million, a significant contraction from the $25.187 million in the previous year. Although a one-time disposal gain of $2.585 million was recorded during the year to partially offset this, under comprehensive effects, the net loss attributable to shareholders for the full year amounted to $29.007 million, equivalent to a loss of $3.17 per ADS. This represents an improvement compared to the loss of $3.78 per ADS in 2023, but the overall situation still reflects the "growing pains" of the deep transformation phase.

It is worth noting that in 2024, Amber recorded a foreign exchange gain of $37.49 million, mainly from the appreciation of Asian currencies against the US dollar. This exchange gain effectively offset some of the book losses, keeping the company's comprehensive loss at $22.593 million, a significant improvement over the $38.673 million in the previous year. This indicates that, after excluding the impact of exchange rates and one-time accounting items, Amber's operational quality is steadily on the path to recovery.

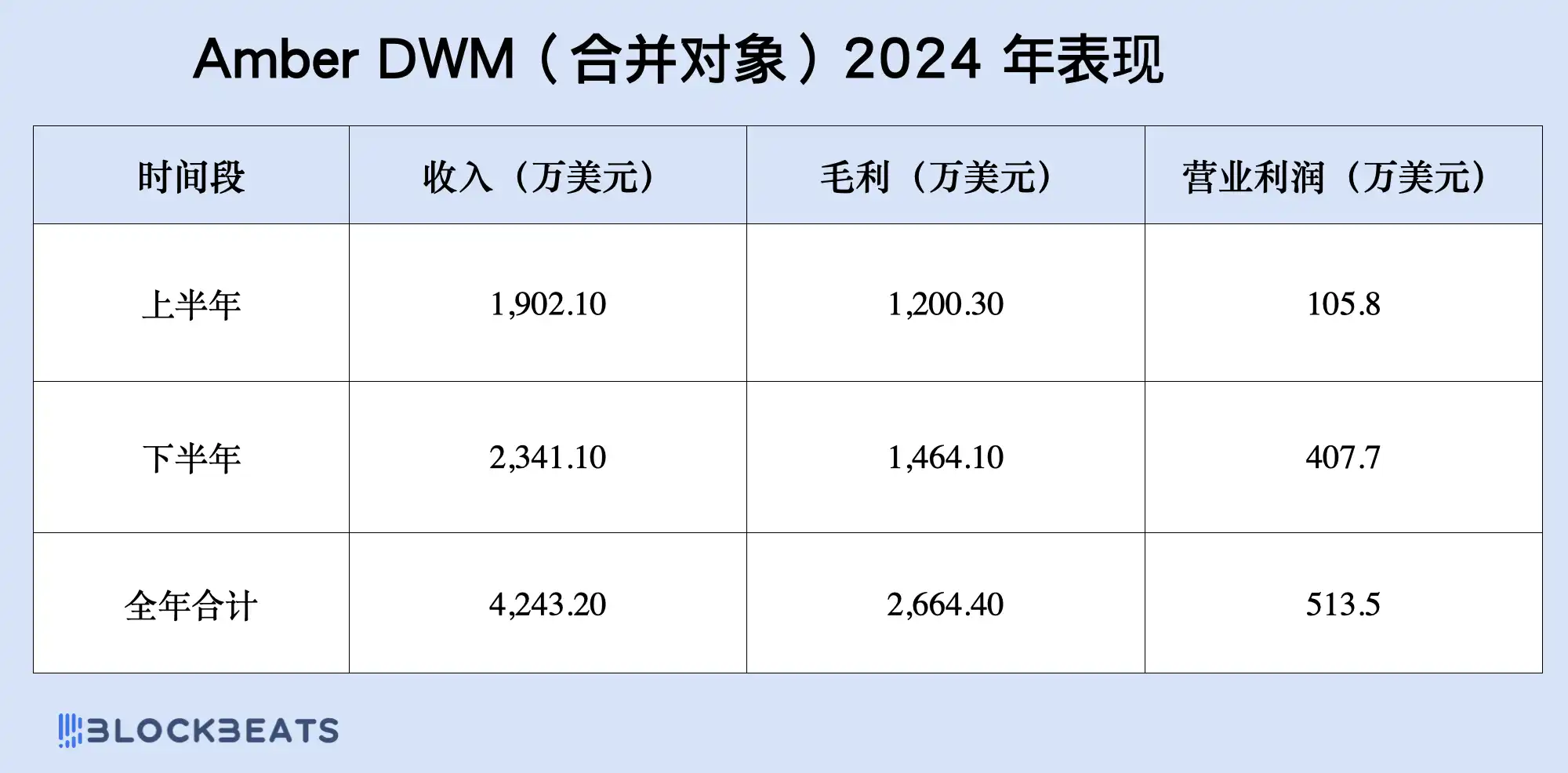

Of particular note is Amber DWM, the business entity that officially completed the merger in 2025 and had a very impressive standalone financial performance in 2024. Although not yet consolidated, Amber disclosed in its annual report that the full-year revenue of this segment has exceeded $42 million, with a substantial profit increase in the second half of the year. This business entity operates under the Amber Premium brand and is a core segment of the company's comprehensive transformation towards compliant crypto financial services, covering institutional crypto asset custody, OTC liquidity matching, portfolio management, and payment solutions for high-net-worth clients, all of which have high added value and significant growth potential.

In outlook for 2025, Amber Premium is highly anticipated. The company expects its revenue for the first quarter of 2025 to reach $12.5 million to $13.5 million, achieving last year's DWM annual revenue in just one quarter, demonstrating rapid expansion. At the same time, Amber has announced the establishment of a $10 million crypto asset reserve fund, formally incorporating crypto assets into the company's balance sheet for the first time. This not only signifies the beginning of its financial system's evolution towards a Web3 financial model but also marks Amber's transition away from the old model towards a comprehensive crypto-native financial platform.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia