Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

error

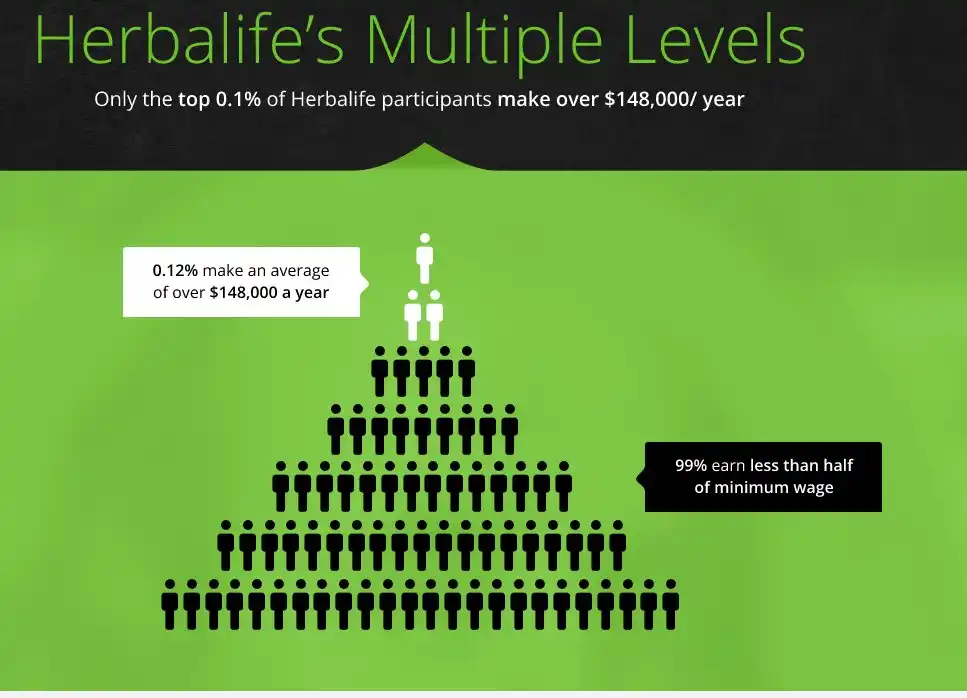

Original Title: Tokens are the new Herbalife. Parallelisms between crypto and Multi-Level Marketing schemes

Original Author: VannaCharmer

Translated by: johyyn, BlockBeats

Editor’s Note: The current cryptocurrency market is mired in a fourfold crisis — structural extraction mechanisms (exchange pricing dominance → VC valuation manipulation → market maker information arbitrage → KOL traffic traps). Retail liquidity awakening has disrupted this predatory chain, threatening its collapse. This article aims to deconstruct the logic of this four-tiered power breakdown and anchor the path toward restructuring token pricing systems as a linchpin for salvation—breaking through OTC opacity and redefining speculative PMF (Product-Market Fit) could transform the “illusory lottery” into a sustainable value vehicle.

Below is the original content (edited for clarity and readability):

Introduction

Cryptocurrency has perfectly replicated the worst traits of Multi-Level Marketing (MLM) schemes—not only embodying the viral marketing nature of the internet but also cloaking itself in even greater opacity. Tokens have essentially evolved into a finely-tuned pyramid: the top-tier players extract the lion’s share of profits, leaving retail investors holding worthless bags.

This is no accident. It is a carefully orchestrated crypto con.

In traditional MLM schemes like Herbalife or Mary Kay, their overpriced and underperforming products (compared to competitors with better cost-effectiveness) are merely surface-level issues. The core problem lies within their distribution model: distributors must first purchase inventory themselves and then hunt for actual consumers to offload the products. This shifts operational focus dramatically from product improvement to recruitment—participants buy only to resell at higher prices rather than actually use the products. The inevitable endgame is the depletion of new entrants to take over, leading to market collapse: the pyramid’s top-level orchestrators reap opaque, exorbitant rewards, while lower-level participants are left with unsold stock and mounting losses.

Operational focus quickly deforms into a “recruitment-over-product” game—participants buy with the sole intent of resale for profit, not for any real usage. Ultimately, the market collapses: every buyer hopes to buy low and sell high, yet no one truly consumes the product. Those at the pyramid’s summit pocket disproportionate gains, while the lower-tier participants are left holding unsellable inventory as sacrificial lambs.

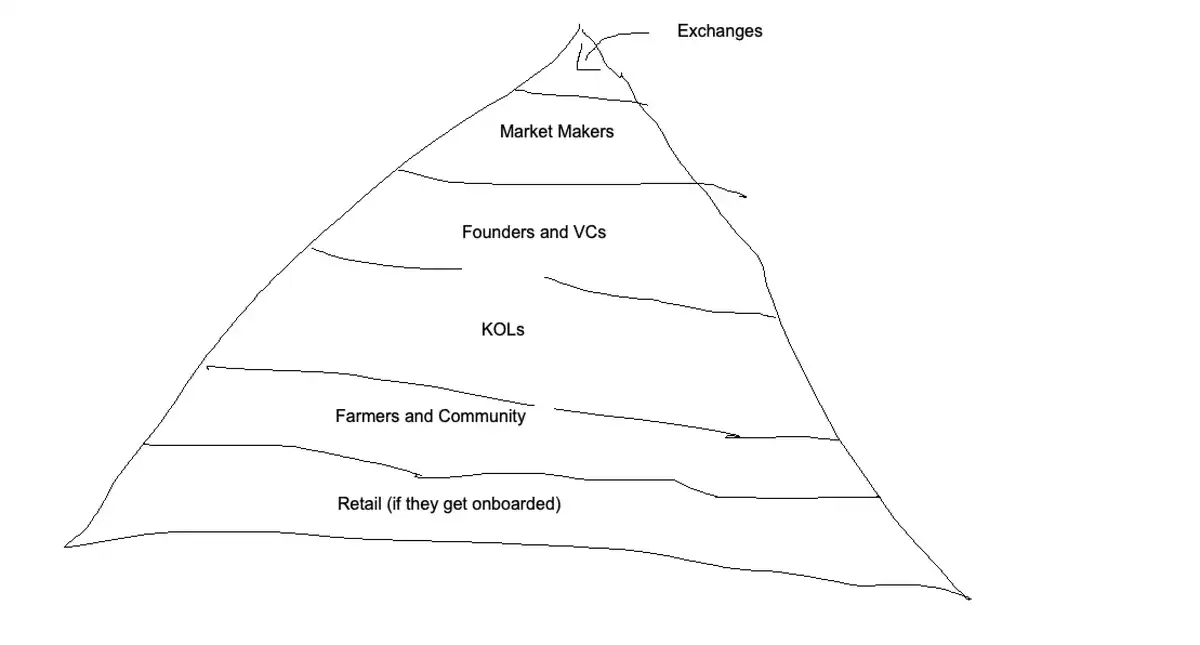

Pyramid Schemes: The Predatory Structure of Crypto Tokens

The operation of cryptocurrency tokens is structurally akin to the essence of pyramid schemes: tokens are the product—essentially premium-priced digital bubble assets meticulously packaged. Aside from their speculative value, their practicality remains highly questionable. Much like MLM distributors, token holders enter the game not for utility but to sell at a higher price to the next buyer, transforming into hunters preying on the next generation of bagholders in a game of musical chairs.

The pyramid structure of cryptocurrency tokens bears structural similarity to traditional multi-level marketing (MLM) models, but the inclusion of blockchain-specific stakeholders (project teams, market makers, exchanges, and KOLs) has constructed a more intricate hierarchy. Tokens, as the transmission medium, offer three distinct advantages compared to traditional MLM products:

1. **Exponential Channel Propagation** → The aggregation effect of the internet and social networks exponentially amplifies dissemination efficiency;

2. **Elimination of Transaction Friction** → 24/7 global liquidity markets enable frictionless trading;

3. **Liquidity Mechanism Innovation** → Automated market-making mechanisms obscure real supply-demand dynamics.

Its capital flow mechanism can be characterized as follows: In traditional MLM, recruiting others allows upstream participants to earn multi-level commissions from downstream transactions; token systems follow a similar logic—holders encourage the market to absorb their unsold positions ("bags") while attracting new entrants to bid up prices. This not only provides exit liquidity for top-tier participants and drives up market prices but also triggers a dual incentive loop, creating a bubble illusion:

1. New holders, pressured by their sunk costs, are compelled to promote the market (holding pressure-driven promotion);

2. Early participants cash out as their positions multiply in value (multiplier effect incentives).

While derived from the same origin as traditional MLM models, these mechanisms operate far more efficiently and powerfully due to their reliance on decentralized financial infrastructure. The higher participants ascend in the pyramid, the more entangled they become in perpetual token issuance and liquidity harvesting cycles. In other words, the marginal returns from continuous token issuance grow, reinforcing a self-perpetuating path dependency that ultimately causes systemic risks to expand geometrically.

The Power Apex: The Exchange Ecosystem

Exchanges occupy the commanding heights of power within the cryptocurrency ecosystem, effectively serving as the central control nodes of the industry. The valuation and liquidity of most so-called "successful" tokens are profoundly influenced by the ecosystem controlled by exchanges and their affiliated market makers. This ecosystem monopolizes token issuance channels and liquidity allocation rights, imposing mandatory financial obligations on project teams—typically through the provision of free tokens as listing fees—in order to secure market access and liquidity resources.

When failing to meet the compliance access requirements set by exchanges, tokens are systematically exposed to three major risk factors: delisting from trading platforms, liquidity crises, and project shutdowns. Exchanges, leveraging their monopolistic position over liquidity supply and token distribution channels, frequently exercise market dominance. Typical behaviors include unilaterally terminating market-making agreements, enforcing employee token lending clauses—essentially creating insider cash-out pathways by design—and imposing retroactive changes to terms during the service provision phase. Industry participants are compelled to endure this systemic rent-seeking framework because, under a market structure dominated by centralized exchanges, paying such compliance costs has become a necessary but insufficient condition for a project’s survival.

The core governance dilemma faced by founders lies in the fact that listing eligibility with top-tier exchanges heavily depends on opaque personal networks, which severely distorts resource allocation mechanisms in the market.

This distortion directly breeds two major gray-market industries:

1. Proliferation of "shadow co-founder" models—individuals securitize access to exchange-related connections in exchange for equity;

2. Industrialization of advisory services by former exchange employees, whose core value lies in navigating the closed decision-making processes.

Such low-transparency approval mechanisms essentially create structural barriers against new projects, making it nearly impossible for teams lacking specialized experience or critical connections to break through effectively.

Subordinate Power Players: The Market-Making System

The Systematic Arbitrage Mechanism of Market Makers

Theoretically, liquidity providers are supposed to facilitate healthier market dynamics. In reality, they act as collaborators in the project team’s off-exchange token sell-offs, executing counter-trades against users by exploiting their privileged access to order flow information. The operational logic can be outlined as follows:

1. Control over token holdings → Market makers hold a significant proportion of the circulated token supply (typically ≥5%), leveraging this scale to create arbitrage opportunities based on asymmetrical information;

2. Amplified exploitation in low-circulation tokens → Due to insufficient market depth in low-liquidity tokens, the profitability of counter-trades grows exponentially;

3. Profit structure revealed → Less than 10% of profits come from liquidity rebates, while over 90% are derived from counter-trading activities.

The core arbitrage capital of market makers lies in their mastery of precise circulating supply data and real-time token inventory levels, allowing them to achieve absolute informational dominance over retail trading flows.

The Founder’s Pricing Dilemma with Market Makers

Market-making services lack a standardized pricing model, and fee structures vary greatly depending on the project team’s negotiation power. This results in an exponential increase in token issuance complexity, effectively creating a barrier to entry for the industry.

Secondary Power Core: The VC-Founder Complex

Positioned beneath exchanges, founders and venture capitalists (VCs) form a secondary power hub. Their core mechanism for value capture occurs during the private token price discovery phase. These actors acquire token allocations at deeply discounted rates (usually 70–90% off) before the project enters the public domain, subsequently creating exit liquidity through narrative engineering.

Systemic Distortions in the Venture Capital Model The crypto venture capital model has shown clear signs of moral hazard:

1. Cost-Free Liquidity Events → Token listings are treated as exit opportunities (unlike traditional VC requiring IPO/M&A).

2. Lack of Long-Term Incentives → Capital naturally gravitates toward short-term liquidity events.

3. Predatory Token Economics → Strategic acquiescence toward exploitative designs (e.g., ultra-high inflation or cliff unlock schedules).

4. Ethical Erosion → Systemic support for pump-and-dump schemes over sustainable business development.

Dual Arbitrage Chains in Token Valuation Manipulation

The token economy has generated unique arbitrage dynamics: VCs mark up portfolio valuations to extract management fees, effectively exploiting limited partners. This strategy is particularly effective in low-float tokens—leveraging fully diluted valuations (FDVs) to inflate apparent market caps and assets under management. The fraudulent core of this model lies in what happens under full token circulation; the actual sell pressure would trigger an immediate collapse in valuation. This unsustainability is prompting industry corrections, with over 60% of crypto VC firms now facing fundraising freezes.

Limits to Improvements in Transparency

While transparency platforms like Echo have slightly improved the information landscape, the private fundraising market remains rife with opaque, unobservable practices, leaving retail participants systemically deprived of meaningful disclosure.

Discourse Leaders: KOL-Led Flow Aggregators

Key opinion leaders (KOLs) form the third-tier power nodes of the pyramid, operating primarily by exchanging token airdrops for promotional content, thereby institutionalizing a token distribution chain. The "KOL round"—where opinion leaders make a nominal investment only to be fully reimbursed post-TGE (Token Generation Event)—has become an industry norm. This system enforces a three-way exploitation dynamic through the control of token distribution rights:

1. KOL Empty-Handed Wolf → Zero-Cost Acquisition of Token Assets

2. Audience Cognition Harvesting → Implementing Brainwashing-Style Marketing Towards Follower Groups (Brainwashing Promotion)

3. Liquidity Sacrifice → Fans Becoming the Exclusive Exit Liquidity for KOLs (Dedicated Exit Liquidity)

Web3 Legion: Community Backbone and Liquidity Farmers

Community members and airdrop farmers form the gravedigger stratum of the pyramid, earning token allocations through intensive labor such as product testing, content creation, and on-chain interaction. However, this labor system has become entirely industrialized—while rewards continue to experience deflation, the complexity of labor rises exponentially.

The vast majority of community members operate under the Law of Realization Lag: only after the Token Generation Event (TGE) and the project's subsequent token sell-off do they realize they've essentially been zero-cost marketing laborers. When realization reaches a critical point, a wave of violent rights protests inevitably erupts. This process delivers three layers of destructive impacts on the actual product development:

Governance Resource Drain → Developers are forced to handle Vexatious Litigation

Brand Trust Collapse → Permanent erosion of Social Capital

Noise Management Costs → Over 30% of R&D resources consumed in PR firefighting

Retail Army: Crypto Commoners

In the pyramid structure of cryptocurrency, retail investors occupy the lowest tier. Their ideal role is to provide exit liquidity (i.e., act as bag holders) for all upper-level participants. These investors are equipped with carefully crafted "narrative" tools designed to enhance the Memetic Premium of assets and attract more buyers, enabling project foundations to profit through token sales.

However, unlike historical cycles where retail investors actively bought into the narrative, retail participants in the current cycle exhibit heightened skepticism. This shift has resulted in community members being forced to hold worthless airdrop tokens, while project insiders have already cashed out through OTC (Over-The-Counter) transactions. The massive backlash on social platforms, driven by token price crashes or zero-value airdrops, stems from one core issue: retail funds in this cycle have not truly entered the market to absorb the majority of tokens, yet project founders have still achieved significant wealth accumulation.

Conclusion

Core Issues in the Industry

The operational logic of the current cryptocurrency market has deviated from the essence of product development, shifting towards peddling narrative tools with high Hallucination Yield, aimed at enticing investors to purchase tokens. Strategies focused on product development are at a systemic disadvantage under the current incentive mechanisms (although this trend is slowly changing).

Structural Failure of Valuation Models

The token valuation system has lost its anchoring to fundamentals, relying entirely on Comps-Based Valuation rather than intrinsic value assessment. Market participants overwhelmingly replace rational analysis of "What real-world problems does this project solve?" with "How many multiples can X token gain?" leading to:

1. Collapse of project pricing mechanisms → Inability to establish credible valuation models

2. Dysfunctional risk assessment → Complete breakdown of underwriting systems

In essence, investors are buying probability lottery tickets rather than equity in businesses, and this characteristic must become a core consideration in investment decisions.

Narrative Manipulation Playbook (Empirical Examples)

The following demonstrates a typical narrative-pitching template for constructing pseudo-investment logic imbued with both digestibility and hallucinatory potential:

"Peter Thiel"-backed stablecoin project plans to issue tokens that will act as proxy assets for Tether equity.

Bullish logic is outlined as follows:

1. Benchmark: Circle's $27 billion market cap

2. Competitive advantage: Tether generates higher revenues and profits with lower operating costs

3. Scarcity premium: No direct channels for investing in Tether → This token fills the gap

4. Imaginative potential: Building a payment network rivaling Circle, enhanced with privacy features

5. Valuation expectation: Trillion-dollar financial future → Current market cap is undervalued

This narrative template exhibits dual manipulation characteristics:

1. Digestibility → Enables efficient propagation within social circles

2. Hallucination Pricing Power → Reserves irrational imaginative projections such as a "10 billion valuation"

```Looking Ahead: Improving the Token Market Structure

I remain firmly convinced that cryptocurrency is still one of the industries providing the highest asymmetric profit opportunities for retail investors, but this advantage is gradually diminishing. Speculation is inherently the core product-market fit in the crypto space, and it is this initial lure that draws market participants to engage with the products we're building. This is also the fundamental reason why we must address and improve the market structure.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia