Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

A 25 basis point interest rate cut has already been priced in. What will be the market's direction next?

On September 17, the Federal Reserve announced a 25-basis-point rate cut, signaling another directional shift in monetary policy. This was another easing measure following three rate cuts at the end of 2024, and prior to this move, the Federal Reserve had remained on hold for five consecutive meetings in 2025. The decision to cut rates this time was the result of multiple factors coming together: the U.S. labor market showed a significant slowdown, with stagnant job growth in August, substantial downward revisions to previous data, and an increase in the unemployment rate to 4.3%, leading the market to believe that the support for "full employment" was weakening. Meanwhile, although inflation remained above the 2% target, holding steady at around 2.9% year-on-year in August, the market generally viewed the price disturbances from tariffs as a temporary phenomenon. In this context, the Federal Reserve seems to be prioritizing employment stability over inflation control and to some extent responding to the continued pressure for rate cuts from President Trump.

It is worth noting that this policy maneuver is not just a shift in monetary policy but also reveals an unprecedented level of internal division within the Federal Reserve. Two members had already cast dissenting votes at the July rate-setting meeting, a rare occurrence dating back to 1993. At the same time, Trump's frequent pressure on Powell has added an extra layer of tension to this policy adjustment. The market widely believes that this rate cut will not only impact future financial market trends and policy expectations but also potentially reshape the global capital flow pattern, becoming a key turning point in this monetary cycle.

Interpreting This Rate Cut

The Federal Reserve's 25-basis-point rate cut this time is more of a "risk-management cut" rather than a signal of starting an aggressive easing cycle. The dot plot shows that the median interest rate expectation for 2025 has been revised down from 3.9% to 3.6%, indicating that with one rate cut already implemented, there is still a 50-basis-point space for cuts this year, most likely to occur in October and December by 25 basis points each time. As of now, the probability of another 25-basis-point rate cut by the Fed in October stands at 87.5%. By 2026 and 2027, the median expectation continues to decline to 3.4% and 3.1%, strengthening the market's view of a moderately accommodative stance in the medium to long term. However, the long-term rate anchor remains steady at 3.0%, indicating that the Federal Reserve's view of the "neutral rate" has not changed.

The signal behind this move is very delicate: on the one hand, the inflation risk remains relatively high, with overall August PCE year-on-year expected to rise to 2.7% and core PCE still at 2.9%, prompting officials not to overly relax policy; on the other hand, the downside risks in the labor market have led them to preemptively prepare. Therefore, Powell's team has chosen to proceed with caution, guiding the market through incremental meeting decisions and expectation management, rather than allowing the policy to swing dramatically.

From a political perspective, this interest rate decision can also be seen as Jerome Powell's conservative response to the Trump camp, defending the Fed's "independence." Apart from the new Fed Governor Milan still carrying out the "President's will," most officials chose to be rational and unified, only releasing a bit of space on the dot plot. In the short term, the market may be appeased by the possibility of a two-time cut, but in terms of results, Trump clearly came out on the losing end in this round of the Fed game.

Historical Rate Cuts: Market Performance During Rate-Cut Cycles

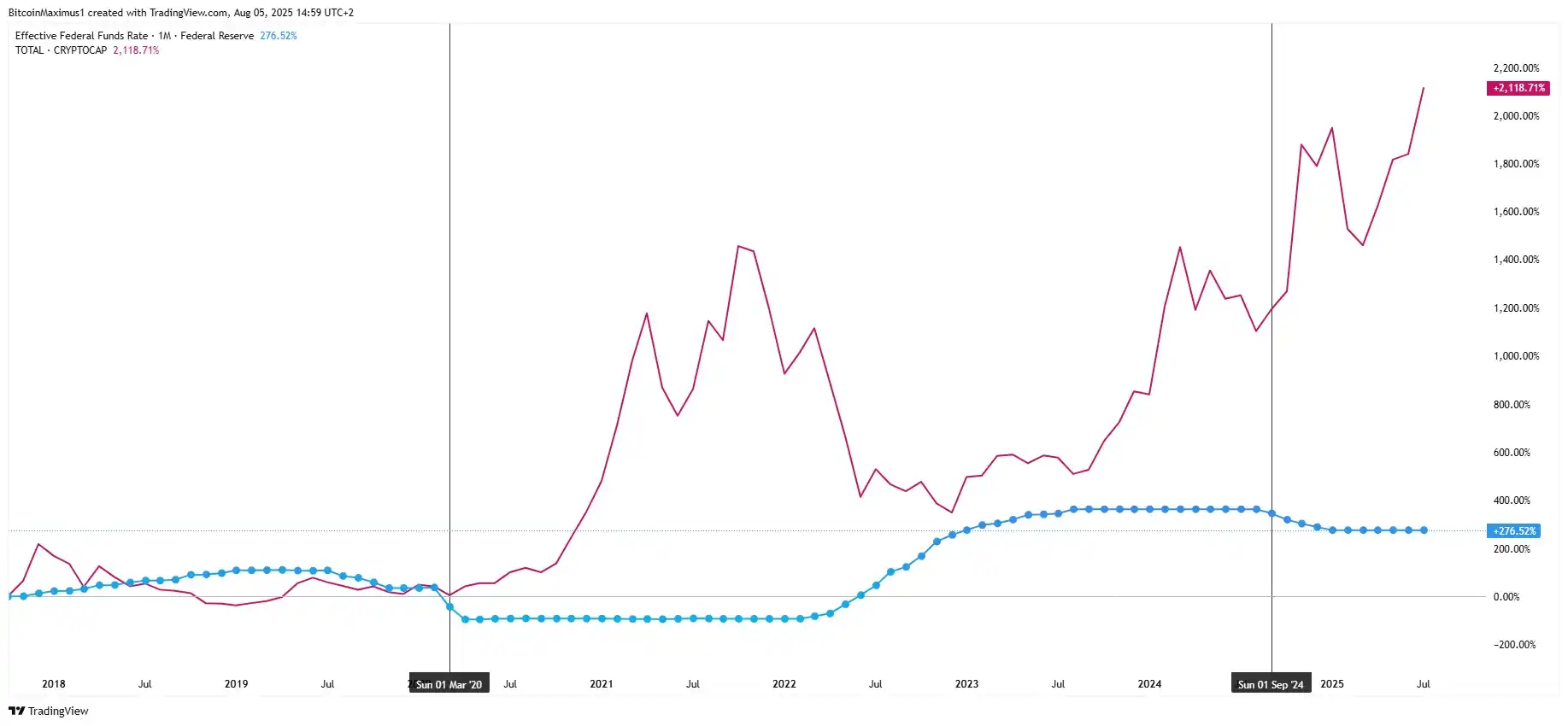

From a historical review, the Fed's rate cuts can generally be divided into two types: preemptive cuts and relief cuts. The rate cuts in 1990, 1995, and 2019 belong to the former, occurring before a full-fledged economic recession, more as a hedge against potential risks, often injecting new growth momentum into the market. On the other hand, the rate cuts in 2001 and 2008 were initiated under the heavy pressure of financial crises, ultimately accompanied by a steep market decline. Currently, the U.S. labor market is weak, tariffs and geopolitical issues continue to create uncertainty, but there are signs of easing inflation, making the overall environment closer to "preemptive rate cuts" rather than a crisis background. It is for this reason that risk assets have been able to maintain a strong uptrend this year, with both Bitcoin and U.S. stocks hitting historic highs.

Related Reading: "Another Rate Cut, Will the Market Launch into a Frenzied Bull Market Post-September?"

When aligning the rate cut path with cryptocurrency market capitalization, it is easy to see a high degree of correlation between the two: a downward interest rate often synchronizes with a bull market cycle in the crypto market. The rate cuts in 2020 and 2024 both marked the beginning of an exponential rise in cryptocurrency. This pattern once again confirms that a rate decrease has a significant positive impact on risk assets such as cryptocurrency.

How Institutions View the Post-Rate Cut Market

In a research report, Coinbase points out that the crypto bull market is expected to continue into the early fourth quarter of 2025, driven by ample liquidity, a favorable macro environment, and supportive regulatory dynamics. Bitcoin is considered the biggest beneficiary, with its performance expected to surpass market expectations. Unless energy prices fluctuate dramatically, leading to increased inflationary pressure, the immediate risks of disrupting the U.S. monetary policy path are quite limited. Additionally, the technical demand of Digital Asset Treasuries (DATs) will continue to inject incremental funds into the crypto market. Although the "September Curse" has long plagued the market — with Bitcoin falling against the dollar every September for six consecutive years from 2017 to 2022 — this seasonal pattern has been broken in 2023 and 2024.

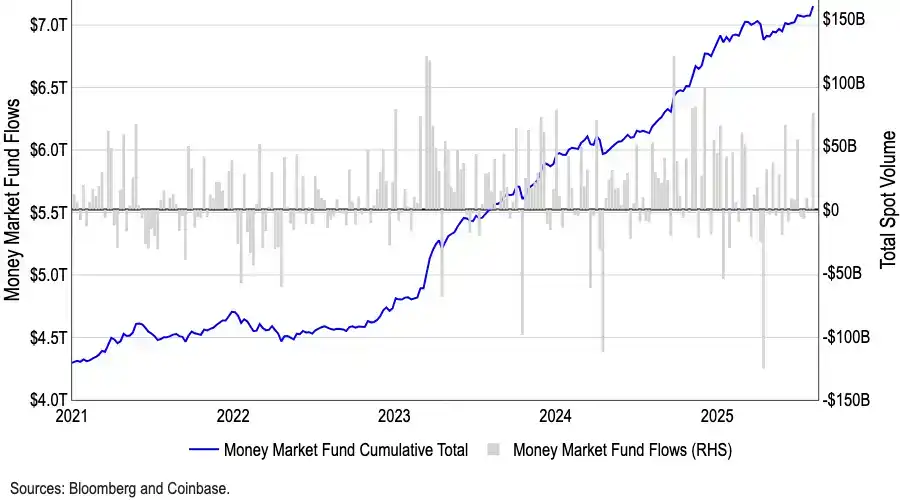

The scale of the U.S. money market fund has reached a record $7.2 trillion, with a large amount of funds trapped in low-risk instruments. Historically, outflows from money market funds have often been positively correlated with the rise of risk assets. As interest rate cuts take effect, their yield attractiveness is gradually weakening, and more funds are expected to be released into crypto and other high-risk assets. It can be said that this unprecedented cash reserve is the most potent potential powder keg of this bull market.

Furthermore, structurally, funds have begun to gradually leave BTC. BTC's market dominance has slipped from 65% in May to 59% in August, while the total market value of altcoins has grown by over 50% since early July, reaching $1.4 trillion. Although CoinMarketCap's "Altseason Index" remains around 40, far from the traditional definition of an altseason threshold of 75, the divergence of this "low-index, skyrocketing market cap" precisely reveals that funds are selectively entering specific sectors, particularly ETH. ETH not only benefits from institutional interest with ETF assets breaking through $220 billion but also embodies the core narrative of stablecoins and RWAs, possessing a funding attractiveness surpassing BTC.

Other institutions are equally optimistic about BTC's price outlook. Derive's Sean Dawson predicts that Bitcoin could reach $140,000 by the end of the year and could even rise to $250,000 if institutional funds continue to flow in. Bitmine CEO Tom Lee stated in a CNBC interview, "It's very easy for Bitcoin to reach $200,000 by the end of this year." BitMEX co-founder Arthur Hayes also predicted in an interview that by the end of 2025, Bitcoin could rise to $200,000, citing the potential U.S. government bond repurchase program that would release liquidity into the market, directing investor funds towards higher-risk assets.

However, some stock traders are hedging against short-term volatility risks as the 25-basis-point rate cut has been largely absorbed by the market. Options traders expect the S&P 500 index to experience approximately 1% two-way fluctuations on Wednesday, marking the largest single-day volatility in nearly three weeks. IUR Capital CEO Gareth Ryan suggests that the key is to see if the dot plot confirms an additional rate cut at the end of 2025 and in the first quarter of 2026. If confirmed, the stock market reaction may be more moderate; if the intention remains vague, the market may experience more significant swings. J.P. Morgan's trading desk has also issued a warning, suggesting that the meeting could evolve into an event where "good news is already priced in."

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia