Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

ArkStream Capital: The upward trend in Q3 comes to a close, entering a revaluation phase in Q4

Original Article Title: "ArkStream Capital: Q3 Rally Comes to an End, Q4 Enters Repricing Phase"

Original Article Author: ArkStream Capital

The third quarter of 2025 was of pivotal importance to the crypto market as it bridged the risk asset rebound since July and further confirmed a macro turning point post the interest rate cut landing in September. However, entering the fourth quarter, the market faced both macro uncertainty shocks and a structural risk outbreak within the crypto market itself, leading to a sharp reversal in market dynamics where previous bullish expectations were shattered.

As the pace of inflation moderation slowed down, coupled with the historically longest U.S. government shutdown erupting in October along with escalating fiscal disputes, the latest FOMC meeting minutes clearly signaled a "cautious about early rate cuts" message, causing severe swings in market assessments of the policy path. The initially clear narrative of "rate-cut cycle initiation" was rapidly undermined, leading investors to recalibrate potential risks such as "higher rates lasting longer" and "soaring fiscal uncertainty," significantly elevating risk asset volatility through the back-and-forth of rate cut expectations. In this context, the Fed also deliberately suppressed market over-expectations to avoid premature easing of financial conditions.

Simultaneously, the prolonged government shutdown further exacerbated macro pressures, exerting a dual squeeze on economic activity and financial liquidity:

• Significantly dragging GDP growth: The Congressional Budget Office estimated that the government shutdown would lower the actual annualized GDP growth rate in Q4 2025 by 1.0% - 2.0%, equivalent to billions of dollars in economic losses.

• Critical data absence and liquidity contraction: The shutdown caused key data such as non-farm payrolls, CPI, PPI, etc., to be delayed, throwing the market into a "data blind spot," increasing the difficulty of policy and economic judgments. At the same time, federal spending interruptions led to a passive liquidity squeeze, with risk assets broadly under pressure.

Entering November, internal debates within the U.S. stock market about whether the AI sector is experiencing a phase of overvaluation continued to heat up, with increased volatility in high-flying tech stocks affecting overall risk appetite, making it challenging for crypto assets to receive spillover support from the U.S. stock market Beta side. Although the early pricing-in of rate cuts in the financial markets during the third quarter had significantly boosted risk appetite, such "liquidity optimism" was notably weakened in the fourth quarter by the repeated impacts of the government shutdown and policy uncertainty, causing risk assets to broadly enter a new round of repricing.

As macroeconomic uncertainty rises, the cryptocurrency market is also facing its own structural shock. In July and August, Bitcoin and Ethereum each hit new all-time highs (Bitcoin surged above $120,000; Ethereum reached around $4,956 by the end of August), with market sentiment temporarily turning positive.

However, the massive liquidation event on October 11th by Binance became the most severe systemic shock to the crypto industry:

• As of November 20th, both Bitcoin and Ethereum experienced significant pullbacks from their highs, with market depth decreasing and long-short divergences widening.

• The liquidity gap caused by the liquidation weakened overall market confidence, leading to a notable drop in market depth in early Q4. Additionally, the liquidation spillover effect exacerbated price volatility and increased counterparty risk.

Meanwhile, the inflow of funds into spot ETFs and coin shares DAT slowed significantly in the fourth quarter, with insufficient institutional buying pressure to offset the selling pressure from liquidations. This lack of buying pressure led the crypto market to gradually transition from high turnover and oscillation since late August to a more pronounced correction phase.

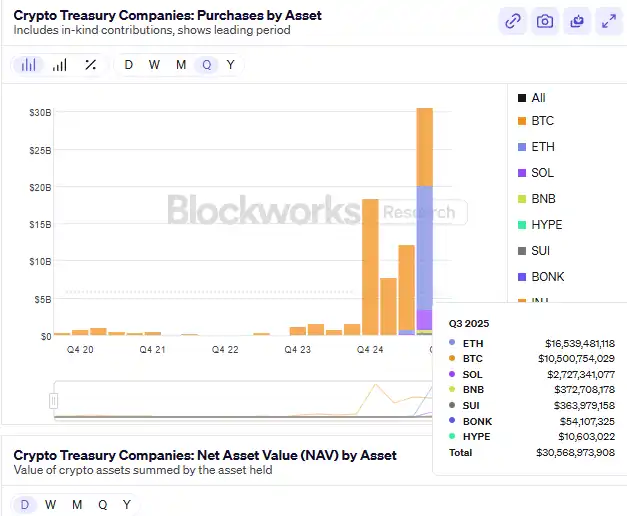

Reflecting on the third quarter, the crypto market's rise stemmed from a resurgence of overall risk appetite and was positively influenced by publicly listed companies driving DAT (Digital Asset Treasury) strategies. This type of strategy increased institutional acceptance of crypto asset allocation, improved the liquidity structure of some assets, and became one of the key narratives of the quarter. However, as liquidity tightened and prices plunged in the fourth quarter, the sustainability of DAT-related buying pressure began to wane.

The essence of DAT strategy lies in companies incorporating some token assets into their balance sheets to enhance capital efficiency through on-chain liquidity, yield aggregation, and staking tools. As more publicly listed companies and funds explore collaborations with stablecoin issuers, liquidity protocols, or tokenization platforms, this model is gradually transitioning from conceptual exploration to practical implementation. Throughout this process, assets like ETH, SOL, BNB, ENA, HYPE, etc., are demonstrating a trend of boundary fusion between "token–equity–asset" in various dimensions, showcasing the role of the Digital Asset Treasury as a bridge in the macro liquidity cycle.

However, in the current market environment, innovative assets related to DAT, with valuation frameworks such as mNAV, are commonly trading below 1, indicating the market's discounting of on-chain asset net worth. This phenomenon reflects investors' concerns about the liquidity, income stability, and valuation sustainability of the related assets, suggesting that the asset tokenization process is facing some short-term adjustment pressure.

At the sector level, multiple segments are showing continuous growth momentum:

• Stablecoin Sector has continued to expand, with a total market capitalization surpassing $2.97 trillion. Its role as a financial anchor in a macro uncertainty environment has been further strengthened.

• Perp Sector, represented by HYPE and ASTER, has achieved a significant increase in activity through transaction structure innovations such as on-chain matching, funding rate optimization, and layered liquidity mechanisms, becoming a major beneficiary of capital rotation within the quarter.

• Prediction Market Sector has reinvigorated under macro expectation volatility, with Polymarket and Kalshi seeing record trading volumes, becoming real-time indicators of market sentiment and risk appetite.

The rise of these sectors indicates that funds are shifting from a singular price game to structured allocations around the three core logics of "liquidity efficiency—yield generation—information pricing."

Overall, the third quarter of 2025 saw a divergence in pace between the crypto and US stock markets, transitioning in the fourth quarter to concentrated exposure to structural risks and widespread liquidity pressure. A government shutdown led to delayed release of key macro data, exacerbating fiscal uncertainty and weakening overall market confidence; the US stock market saw increased volatility surrounding AI valuation debates, while the crypto market faced more direct liquidity and depth impacts following the Binance liquidation event. Meanwhile, DAT strategy fund inflows slowed, with widespread mNAVs falling below 1, demonstrating the market's high sensitivity to liquidity environment amidst institutionalization, with clear vulnerabilities. The ability to stabilize thereafter will primarily depend on the pace of digesting the impact of the liquidation event, and whether the market can gradually restore liquidity and stabilize sentiment in an environment of increased long and short positions.

Rate Cut Expectations Met, Market Enters Repricing Stage

In the third quarter of 2025, the critical variable in the global macro environment was not the "rate cut" event itself, but the generation, trading, and consumption of rate cut expectations. Pricing of the liquidity inflection point had begun as early as July, with the actual policy action serving as a node to validate existing consensus.

After two quarters of speculation, the Federal Reserve cut the federal funds rate target range by 25 basis points to 4.00%–4.25% at the September FOMC meeting, followed by another slight cut in the October meeting. However, as the market consensus on a rate cut was already highly aligned prior, the marginal impact of the policy action on risk assets was limited, with the signaling effect of the rate cut largely priced in beforehand. At the same time, as inflation decelerated and economic resilience outperformed expectations, the Fed began expressing concerns about the "market pricing in consecutive rate cuts next year," leading to a significant decrease in the probability of further cuts in December after October. This communication stance became a new variable dragging down market risk appetite.

Macroeconomic data exhibited a "mild cooldown" feature in the third quarter:

• Core CPI Year-over-Year decreased from 3.3% in May to 2.8% in August, confirming the downward trend in inflation;

• Nonfarm Payrolls remained below 200,000 for three consecutive months;

• Job Opening Rate fell to 4.5%, reaching the lowest level since 2021.

This set of data indicates that the U.S. economy has not entered a recession but has entered a period of moderate slowdown, providing the Federal Reserve with the policy space for "controlled rate cuts." As a result, the market had already formed a consensus on "certainty of rate cuts" at the beginning of July.

According to the CME FedWatch Tool, investors' probability of a 25-basis-point rate cut in September exceeded 95% by the end of August, indicating that the market had almost completely priced in the expected outcome in advance. The bond market also reflected this signal:

• 10-Year Treasury Yield declined from 4.4% at the beginning of the quarter to 4.1% at the end of the quarter;

• 2-Year Yield experienced a larger decrease of approximately 50 bps, showing that market trades on the policy shift were more concentrated.

The macro inflection point in the third quarter was more of a "digested expectation" rather than a "policy change." The pricing of liquidity repair was largely completed between July and August, and the actual rate cut in September was just a formal confirmation of the existing consensus. For risk assets, the new marginal variable has shifted from "whether a rate cut will happen" to "the pace and sustainability of rate cuts."

However, when the rate cut is actually implemented, the anticipated marginal effects have already been fully absorbed, and the market quickly enters a vacuum stage of "no new catalysts."

Starting in mid-September, the changes in macro indicators and asset prices have shown a significant dulling:

• Flattening of the U.S. Treasury Yield Curve: As of the end of September, the 10-Year–3-Month Treasury yield spread was only about 14 basis points, indicating that term premiums still exist but the risk of inversion has been alleviated.

• U.S. Dollar Index declined to the 98–99 range, significantly weakening from its early-year high (107), but the cost of dollar funding remained relatively tight at the quarter-end settlement.

• U.S. Stock Market Liquidity Margin Contraction: The Nasdaq Index continues to rise, but ETF inflows are slowing down, and trading volume growth is lackluster, indicating that institutions have started adjusting their risk exposure at high levels.

This "post-expectation-realization vacuum period" has become the most representative macro phenomenon within the quarter. The market traded the "rate cut certainty" in the first half and began pricing in the "growth slowdown reality" in the second half.

The Federal Reserve's September meeting's Summary of Economic Projections (SEP) showed a significant divergence within the decision-making body regarding the future interest rate path:

• The median expected policy rate by the end of 2025 was lowered to 3.9%;

• Committee members' forecasts ranged from 3.4% to 4.4%, reflecting the decision-makers' differing opinions on inflation stickiness, economic resilience, and policy space.

Following the rate cut in September and another slight cut in October, the Fed's communication gradually shifted to a more cautious tone to avoid early loosening of financial conditions. As a result, the previously heavily bet on probability of another rate cut in December has significantly retreated, and the policy path has returned to a framework of "data dependence" rather than a "preset pace."

Unlike the previous rounds of "crisis-driven accommodation," this round of rate cuts is a policy adjustment with a controllable pace. While cutting rates, the Fed continues balance sheet reduction, sending a signal of "stabilizing capital costs and dampening inflation expectations," emphasizing a balance between growth and prices rather than actively expanding liquidity. In other words, the interest rate inflection point has been established, but the liquidity inflection point has not yet arrived.

Against this backdrop, the market exhibits distinct differentiation characteristics. The decline in funding costs provides valuation support for some high-quality assets, but broad liquidity has not significantly expanded, and fund allocation is becoming more cautious.

• Sectors with stable cash flow and profit support (AI, tech blue-chips, some data-centric U.S. stocks) continue the trend of valuation recovery;

• Assets with high leverage, high valuation, or lacking cash flow support (including some growth stocks and non-mainstream crypto tokens) see waning momentum post-expectation realization, with trading activity significantly decreasing.

Overall, the third quarter of 2025 is a "post-expectation realization period," not a "liquidity release period." The market priced in rate cut certainty in the first half, then shifted to a reevaluation of the growth slowdown in the second half. The early exhaustion of expectations keeps risk assets at high levels but lacking sustained upward momentum. This macro pattern lays the foundation for subsequent structural differentiation, also explaining the "breakthrough-drop-high volatility" trend in the crypto market in Q3: capital flows towards relatively stable, cash-flow-verifiable assets, rather than systemic risk assets.

The DAT Boom and Structural Inflection Point of Non-Bitcoin Assets

By the third quarter of 2025, Digital Asset Treasury (DAT) had risen from the fringe concept of the crypto industry to the fastest-spreading new theme in the global capital markets. For the first time in this quarter, public market funds entered the crypto asset space in scale and mechanism, with billions of dollars of fiat liquidity flowing directly into the crypto market through traditional financing tools such as PIPE, ATM, and convertible bonds, forming a structured trend of "coin-stock linkage."

The origin of the DAT model can be traced back to the trailblazer of the traditional market, MicroStrategy (NASDAQ: MSTR). Since 2020, the company has been the first to incorporate Bitcoin into its corporate balance sheet and has accumulated approximately 640,000 bitcoins through multiple rounds of convertible bond and ATM issuance between 2020 and 2025, with a total investment exceeding $47 billion. This strategic move not only reshaped the company's asset structure but also created a paradigm where traditional stocks became the "secondary carrier" of crypto assets.

Due to the systemic difference in valuation logic between the equity market and on-chain assets, MicroStrategy's stock price has long been higher than its Bitcoin net asset value, with the mNAV (Market Value / On-Chain Asset Net Value) staying in the range of 1.2–1.4 times on an annual basis. This "structural premium" reveals the core mechanism of DAT:

Enterprises hold crypto assets through public market financing, allowing fiat capital and crypto assets to form bidirectional connectivity and valuation feedback at the company level.

From a mechanistic perspective, MicroStrategy's experiment laid the three pillars of the DAT model:

• Financing Channel: Introducing fiat liquidity through PIPE, ATM, or convertible bonds to provide enterprises with capital for on-chain asset allocation;

• Asset Reserve Logic: Incorporating crypto assets into the financial reporting system to create an enterprise-level "On-Chain Treasury";

• Investor Entry: Allowing traditional capital market investors to gain indirect exposure to crypto assets through stocks, reducing compliance and custody barriers.

These three together constitute the "structural loop" of DAT: Financing—Holding—Valuation Feedback. Enterprises absorb liquidity through traditional financial tools, form crypto asset reserves, then capitalize through the equity market's premium to achieve capital thickening, realizing dynamic rebalancing between capital and tokens.

The significance of this structure is that it has first enabled digital assets to enter the traditional financial system's balance sheet in a compliant manner and has given the capital markets a new form of asset — “tradable on-chain asset mapping”. In other words, companies are no longer just on-chain participants but have become structural intermediaries between fiat capital and crypto assets.

As this model was validated by the market and quickly replicated, the third quarter of 2025 marked the second-stage diffusion of the DAT concept: from a “store-of-value treasury” centered around Bitcoin, expanding to Ethereum (ETH) and Solana (SOL) and other productive assets (PoS yields or DeFi yields). This new generation DAT model, with the mNAV (market cap / on-chain asset net value) pricing system at its core, integrates yield-bearing assets into the enterprise's cash flow and valuation logic, forming a “yield-driven treasury cycle.” Unlike the early Bitcoin treasuries, assets like ETH and SOL have sustainable Staking yields and on-chain economic activity, endowing their treasury assets with not only a store-of-value attribute but also cash flow characteristics. This shift marks DAT's evolution from mere asset holding to a capital structure innovation centered around productive yields, becoming a key bridge connecting the value of productive crypto assets with the traditional capital market valuation system.

Note: Entering November 2025, a new round of cryptocurrency market downturn triggered the most systematic revaluation of the DAT sector since its inception. With core assets like ETH, SOL, BTC experiencing rapid 25–35% retracements in October and November, along with some DAT companies accelerating their balance sheet expansion through ATM, leading mainstream DAT companies saw their mNAV fall below 1. BMNR, SBET, FORD, among others, experienced varying degrees of “discounted trading” (mNAV ≈ 0.82–0.98), and even MicroStrategy (MSTR), which had maintained a long-term structural premium, briefly saw its mNAV fall below 1 in November, the first time since the launch of its Bitcoin treasury strategy in 2020. This phenomenon marks the market's transition from a period of structural premium to a “asset-led, valuation discount” defensive stage. Institutional investors widely view this as the first comprehensive “stress test” for the DAT industry, reflecting the capital market's reassessment of the sustainability of on-chain asset yields, the pace of treasury expansion, and the long-term impact of the financing structure on equity value.

SBET and BMNR Lead the Ethereum Treasury Wave

In the third quarter of 2025, the market landscape of Ethereum Treasuryization (ETH DAT) was preliminarily established. In this regard, SharpLink Gaming (NASDAQ: SBET) and BitMine Immersion Technologies (NASDAQ: BMNR) emerged as two flagship companies defining the industry paradigm. Not only did they replicate MicroStrategy's balance sheet strategy, but they also achieved a "concept to institution" leap in funding structure, institutional participation, and disclosure standards, building the dual pillars of the ETH Treasury Cycle.

BMNR: The Capital Engineering of Ethereum Treasuryization

As of the end of September 2025, BitMine Immersion Technologies (BMNR) has established its position as the world's largest Ethereum Treasury. According to the company's latest disclosure, it holds approximately 3,030,000 ETH, which, based on the October 1st closing price of $4,150/ETH, corresponds to an on-chain net asset of about $12.58 billion. When accounting for the company's book cash and other liquid assets, BMNR's total crypto and cash holdings amount to around $12.9 billion.

By this estimate, BMNR's holdings represent approximately 2.4–2.6% of Ethereum's circulation, making it the first publicly listed institution holding over 3 million ETH. With a corresponding market value of about $11.2–11.8 billion, implying an mNAV ≈ 1.27x, it is the highest valued among all publicly listed Digital Asset Treasury (DAT) companies.

BMNR's strategic ascent is closely tied to its organizational restructuring. Following Chairman Tom Lee's (former Fundstrat co-founder) full takeover of capital operations in 2025, a pivotal assertion was made: "ETH is the asset of future institutional sovereignty." Under his leadership, the company completed a structural transformation from a traditional mining enterprise to one where "ETH is the sole reserve asset, and PoS yield is the core of cash flow," becoming the first U.S. publicly listed company to make Ethereum staking yield its primary operating cash flow.

In terms of funding, BMNR demonstrated rare funding intensity and execution efficiency. The company simultaneously expanded its funding sources in the public market and private placement channels, providing long-term ammunition for its Ethereum Treasury strategy. This quarter, BMNR not only refreshed the financing pace of traditional capital markets but also laid the institutional groundwork for "on-chain asset securitization."

On July 9th, BMNR, through a Form S-3 registration statement, signed an "At-the-Market (ATM)" offering agreement with Cantor Fitzgerald and ThinkEquity, with an initial authorized amount of $20 billion. Just two weeks later, on July 24th, the company disclosed in an SEC 8-K filing that the amount had been increased to $45 billion to address the market's positive response to its ETH treasury model. On August 12th, the company once again submitted a supplemental filing to the SEC, raising the total ATM amount to $245 billion (an additional $200 billion), with the explicit purpose of purchasing ETH and expanding the PoS staking asset portfolio.

These amounts represent BMNR's SEC-approved limit for sustainable market price issuance of stock and do not equate to actual cash raised.

On the ground funding-wise, the company has completed several specific transactions:

• In early July 2025, a $250 million PIPE private placement was completed to provide funding for the initial ETH position;

• ARK Invest (Cathie Wood) disclosed on July 22nd the purchase of approximately $182 million of BMNR common stock, with a net raise of $177 million directly used by the company to increase its ETH holdings;

• Founders Fund (Peter Thiel) declared a 9.1% ownership on July 16th to the SEC. While not additional financing, this move strengthened institutional consensus in the market.

In addition, under its early ATM authorization, BMNR has sold approximately $45 billion equivalent in stock, significantly exceeding the initial PIPE amount. As of September 2025, the company has cumulatively deployed funds through PIPE + ATM and other channels totaling billions of dollars, and continues to advance its long-term expansion plans within the $245 billion total authorization framework.

BMNR's financing structure exhibits a clear three-tier architecture:

• Definitive Funding Layer—Completed PIPE and institutional directed subscription, totaling around $4.5–5 billion;

• Market-based Expansion Layer—Selling shares in stages through the ATM mechanism, with actual fundraising reaching the multi-billion-dollar level;

• Potential Ammunition Layer — The SEC-approved $24.5 billion ATM total volume, providing upper limit elasticity for future ETH treasury expansion.

With this layered capital structure, BMNR quickly built a reserve of approximately 3.03 million ETH (worth around $12.58 billion), achieving the treasury's strategic transition from a "single-position experiment" to "institutional asset allocation."

BMNR's valuation premium mainly comes from two logic layers:

• Asset Layer Premium: The PoS staking yield remains at 3.4–3.8% APY, forming a stable cash flow anchor;

• Capital Layer Premium: As a "compliant ETH leverage channel," its stock price usually leads ETH spot by 3–5 trading days, becoming an institutional leading indicator tracking the ETH market.

In terms of market behavior, BMNR's stock price reached new all-time highs in sync with ETH in the third quarter and drove sector rotation several times. Its high turnover rate and circulating stock turnover speed indicate that the DAT model is gradually evolving into a tradable "on-chain asset mapping mechanism" in the capital market.

SBET: A Transparent Sample of Institutionalized Treasury

Compared to BitMine Immersion Technologies' (BMNR) aggressive balance sheet expansion strategy, SharpLink Gaming (NASDAQ: SBET) chose a more stable, institutionalized treasury path in the third quarter of 2025. Its core competency lies not in fund size but in the transparent development of governance structure, disclosure standards, and audit system, establishing a replicable "institutional-level template" for the DAT industry.

As of September 2025, SBET holds approximately 840,000 ETH, estimated at the quarter-end average price, with on-chain assets of around $3.27 billion, corresponding to a market cap of about $2.8 billion, mNAV ≈ 0.95×. Although the valuation is slightly lower than net assets, the company's quarterly EPS growth reached a high of 98%, demonstrating its strong operational leverage and execution efficiency in ETH monetization and cost control.

SBET's core value lies not in aggressive position expansion but in establishing the DAT industry's first compliant, auditable governance framework:

• Strategic advisor Joseph Lubin (Ethereum co-founder, ConsenSys founder) joined the company's Strategic Advisory Board in Q2, driving the incorporation of staking rewards, DeFi derivatives, and liquidity mining strategies into the corporate treasury portfolio;

• Pantera Capital and Galaxy Digital participated in PIPE financing and secondary market holdings, providing institutional liquidity and on-chain asset allocation advisory to the company;

• Ledger Prime provided on-chain risk hedging and volatility management models;

• Grant Thornton, as an independent audit firm, was responsible for verifying the authenticity of on-chain assets, earnings, and staking accounts.

This governance structure constitutes the DAT industry's first "on-chain verifiable + traditional audit parallel" disclosure mechanism.

In the 10-Q report for Q3 2025, SBET fully disclosed for the first time:

• The company's main wallet addresses and on-chain asset structure;

• Staking reward curve and node distribution;

• Risk limits for collateralization and restaking positions.

This report made SBET the first publicly listed company to synchronously disclose on-chain data in SEC filings, significantly increasing institutional investor trust and financial comparability. The market widely regards SBET as a "compliant ETH index component stock": its mNAV is close to 1×, its price is highly correlated with the ETH market, yet it exhibits relatively low volatility due to transparent information and a robust risk structure.

ETH Treasury Dual Narrative: Asset-Driven and Governance-Driven

The differentiation paths of BMNR and SBET constitute the two core narratives of the ETH DAT ecosystem development in Q3 2025:

• BMNR: Asset-Driven—with financing for balance sheet expansion, institutional holdings, and capital premiums as the core logic. BMNR rapidly accumulated ETH positions through PIPE and ATM financing tools, and through mNAV pricing, established a market-driven leverage channel to drive the direct coupling of fiat capital and on-chain assets.

• SBET: Governance-Driven — Emphasizing transparent compliance, treasury yield structuring, and risk control as the main focus. SBET incorporates on-chain assets into an audit and disclosure system, establishes the institutional boundaries of DAT through an on-chain validation and traditional accounting parallel governance structure.

These represent the two poles of ETH treasuryization's shift from "reserve logic" to "institutionalized asset form": the former expands capital scale and market depth, while the latter establishes governance trust and institutional compliance foundations. In this process, ETH DAT's functional attributes have surpassed "on-chain reserve assets," evolving into a compound structure that combines cash flow generation, liquidity pricing, and balance sheet management.

Institutional Logic of PoS Yield, Governance Rights, and Valuation Premium

The core competitiveness of ETH and other PoS native assets' treasuries comes from the triple combination of interest-bearing asset structure, network layer discourse power, and market valuation mechanism.

High Staking Yield: Establishment of Cash Flow Anchor

Distinct from Bitcoin's "non-productive holding," as a PoS network asset, ETH can earn a 3–4% annualized yield through staking, forming a compound yield structure in the DeFi market (Staking + LST + Restaking). This allows DAT companies to capture on-chain real cash flow in a corporate form, transforming digital assets from "static reserves" to "income-generating assets," with stable endogenous cash flow characteristics.

Discourse Power and Resource Scarcity in PoS Mechanism

Following the expansion of staking scales, ETH treasury companies gain governance rights and ranking rights at the network level. BMNR and SBET currently control approximately 3.5–4% of the total ETH staking, entering the marginal impact range of protocol governance. This kind of control possesses a premium logic similar to "systemic importance," as the market is willing to provide a valuation multiplier higher than the asset's net worth.

Formation Mechanism of mNAV Premium

The valuation of DAT companies not only reflects the net asset value (NAV) of the on-chain assets they hold but also includes two types of expectations:

• Cash Flow Premium: Expectation of staking yield and distributable profit from on-chain strategies;

• Structural Premium: Corporate equity provides a compliant ETH exposure channel for traditional institutions, creating institutional scarcity.

At the market peak in July and August, the ETH DAT average mNAV was maintained in the range of 1.2–1.3x, with some individual companies (BMNR) reaching as high as 1.5x. This valuation logic is similar to the premium of a Gold ETF or the NAV discount/premium structure of a closed-end fund, serving as a crucial "pricing intermediary" for institutional funds entering on-chain assets.

In other words, the premium of DAT is not driven by sentiment but rather formed based on real yield, network power, and capital channels' composite structure. This also explains why the ETH treasury achieved higher funding density and transaction activity in just one quarter compared to the Bitcoin treasury (MSTR model).

The Structural Evolution from ETH to Multi-Alt Treasury

Entering August and September, the expansion rate of non-Ethereum-based DATs significantly accelerated. A new wave of institutional allocation led by Solana treasuryization signifies a shift in market theme from "single-asset reserve" to "multi-chain asset layering." This trend indicates that the DAT model is evolving from the core of ETH to multi-ecosystem replication, forming a more systemic cross-chain capital structure.

FORD: An Institutionalized Example of the Solana Treasury

Forward Industries (NASDAQ: FORD) became the most representative case of this stage. The company completed a $1.65 billion PIPE financing in the third quarter, with all funds allocated to Solana spot position building and ecosystem collaboration investments. As of September 2025, FORD holds approximately 6.82 million SOL, valued at an average quarterly closing price of $248–$252, with an on-chain treasury net worth of around $1.69 billion, corresponding to a stock market value of approximately $2.09 billion, mNAV ≈ 1.24×, ranking first among non-ETH treasury companies.

Unlike the early ETH DAT, FORD's rise is not driven by a single asset but rather a product of multi-party capital and ecosystem resonance:

• Investors include Multicoin Capital, Galaxy Digital, and Jump Crypto, all long-term core investors in the Solana ecosystem;

• The governance structure introduces members of the Solana Foundation Advisory Committee, establishing a strategic framework of "on-chain assets as enterprise production inputs";

• The held SOL assets are kept fully liquid, without being staked or used in DeFi protocols, in order to maintain strategic flexibility for future Restaking and Real World Asset (RWA) asset integration.

This "High Liquidity + Configurable Treasury" model positions FORD as the capital hub of the Solana ecosystem, reflecting the market's structural premium expectation for high-performance blockchain assets.

Structural Changes in the Global DAT Landscape

As of the end of the third quarter of 2025, the total disclosed non-Bitcoin DAT treasury size globally has surpassed $24 billion, representing a quarter-over-quarter growth of approximately 65% from Q2. The distribution is as follows:

• Ethereum (ETH) continues to dominate, accounting for around 52% of the total size;

• Solana (SOL) represents about 25%, becoming the second largest direction for institutional fund allocations;

• Other funds are mainly distributed among emerging assets such as BNB, SUI, HYPE, forming a horizontal expansion layer of the DAT model.

The valuation anchor of ETH DAT lies in the PoS yield and governance value, representing a combination logic of long-term cash flow and network control power; while SOL DAT's core premium source lies in ecosystem growth potential and staking efficiency, emphasizing capital efficiency and scalability. BMNR and SBET established the institutional and asset foundation in the ETH phase, and the emergence of FORD is driving the DAT model into the second stage of multi-chain and ecosystem development.

Meanwhile, some newcomers have begun exploring the functional extension of DAT:

• StablecoinX model introduced by Ethena (ENA) combines national bond yields with on-chain hedging structures, attempting to create a "yield-bearing stablecoin treasury" to generate stable yet cash-flowing reserve assets;

• The BNB DAT is led by the exchange system, leveraging asset collateralization from ecosystem enterprises and reserve tokenization to expand liquidity pools, forming a "closed treasury system."

Phase Stagnation and Risk Repricing After Valuation Overshoot

After experiencing a concentrated uptrend in July and August, the DAT sector entered a rebalancing phase in September after overvaluation. Secondary treasury stocks briefly pushed up the sector's overall premium, with the mNAV median exceeding 1.2×. However, as regulatory tightening and funding slowdown took place, valuation support quickly receded by the end of the quarter, and the sector's hype noticeably cooled off.

Structurally, the DAT industry is transitioning from "asset innovation" to "institutional integration." The ETH and SOL treasuries have established a "dual-core valuation system," but the liquidity, compliance, and real yield of expansionary assets are still in the validation stage. In other words, market momentum has shifted from "premium expectation" to "profit realization," marking the industry's entry into a repricing cycle.

As September began, core metrics simultaneously weakened:

• ETH staking yield fell from 3.8% at the beginning of the quarter to 3.1%, and SOL staking yield saw a month-on-month decline of over 25%;

• Several secondary DAT companies have seen mNAV drop below 1, with marginal capital efficiency diminishing;

• PIPE and ATM financing amounts decreased by approximately 40% compared to the previous month, with institutions like ARK, VanEck, Pantera pausing new DAT allocations;

• On the ETF front, net fund inflows turned negative, and some funds replaced their ETH treasury positions with short-duration government bond ETFs to reduce valuation volatility.

This pullback reveals a core issue: the capital efficiency of the DAT model has been overextended in the short term. The early valuation premium stemmed from structural innovation and institutional scarcity. However, as on-chain returns decline and financing costs rise, companies are expanding their balance sheets faster than revenue growth, falling into a "negative dilution loop" — where market cap growth relies on financing rather than cash flow.

From a macro perspective, the DAT sector is now entering the "internalized valuation phase":

• Core companies (BMNR, SBET, FORD) are maintaining structural stability through robust treasuries and information transparency;

• Peripheral projects face deleveraging and liquidity shrinkage due to single capital structures and inadequate disclosure;

• On the regulatory front, the SEC is requiring companies to publicly disclose major wallet addresses and staking yield standards, further compressing the space for "high-frequency balance sheet expansion."

The main short-term risk comes from valuation compression due to liquidity reflexivity. When the mNAV continues to decline and the PoS yield struggles to cover the financing cost, market confidence in the "on-chain reserve + equity pricing" model will be undermined, leading to a systemic valuation pullback similar to the post-2021 DeFi summer. Nevertheless, the DAT industry has not entered a recession but has transitioned from an "asset expansion-driven" phase to a "yield-driven" phase. Over the next few quarters, ETH and SOL treasuries are expected to maintain their institutional advantage, with their valuation core relying more on:

Staking and restaking yield efficiency;

On-chain transparency and compliance disclosure standards.

In other words, the first phase of the DAT frenzy has ended, and the industry has entered a "consolidation and validation period." The key variables for future valuation regression are the stability of PoS yield, the efficiency of restaking integration, and the clarity of regulatory policies.

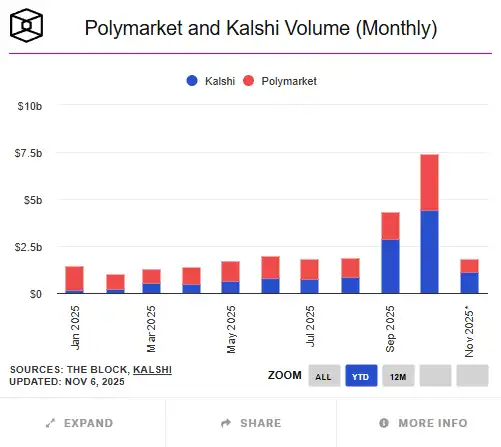

Prediction Markets: The "Barometer" of Macro Narratives and the Rise of Attention Economy

By the third quarter of 2025, prediction markets will transition from "crypto-native edge play" to "new market infrastructure at the intersection of on-chain and compliant finance". In an environment of frequent macro policy changes, drastic fluctuations in inflation and rate expectations, prediction markets are gradually becoming a vital place to capture market sentiment, hedge policy risks, and discover narrative prices. The integration of macro and on-chain narratives has transformed it from a speculative tool to a market layer that combines information aggregation and price signaling functions.

Historically, crypto-native prediction markets have shown significant foresight in several macro and political events. During the 2024 US presidential election, Polymarket's total trading volume exceeded $500 million, with a single contract "who will win the presidential election" reaching $250 million, and a daily trading peak exceeding $20 million, setting a record in on-chain prediction markets. In events like "Will the Fed cut rates in September 2024," the price changes in contracts were significantly ahead of the CME FedWatch rate futures' expected adjustments, demonstrating that prediction markets have shown leading indicator value at certain time periods.

However, the overall volume of on-chain prediction markets is still much smaller than traditional counterparts. Since 2025, the global cryptocurrency prediction market (represented by platforms like Polymarket, Kalshi) has accumulated a total trading volume of approximately $24.1 billion, while traditional compliant platforms like Betfair and Flutter Entertainment have annual trading volumes in the hundreds of billions of dollars. The on-chain market size is still less than 5% of the traditional market, but in terms of user growth, thematic coverage, and trading activity, it has shown higher growth potential than traditional financial products.

In the third quarter, Polymarket became a phenomenon-level growth case. Unlike the mid-year rumors of a "billion-dollar valuation funding," the latest news in early October indicates that the New York Stock Exchange parent company ICE plans to invest up to $2 billion, acquiring a stake of about 20%, corresponding to a Polymarket valuation of approximately $80–90 billion. This means that its data and business model have received recognition at the Wall Street level. As of the end of October, Polymarket's annual cumulative trading volume is around $13.2 billion, with a monthly trading volume in September reaching $14–15 billion, a significant increase from the second quarter. Furthermore, the October monthly trading volume hit a historic high of $30 billion. Trading themes were concentrated on macro and regulatory events such as "Will the Fed cut rates at the September FOMC meeting," "Will the SEC approve an Ethereum ETF before the end of the year," "Key state win rates in the U.S. presidential election," and "Price performance of Circle (CIR) post-listing." Some researchers have pointed out that the price fluctuations of these contracts often lead the U.S. bond yields and FedWatch probability curve by about 12–24 hours, becoming a forward-looking market sentiment indicator.

At the same time, Kalshi achieved an institutional breakthrough on the compliance path. As a prediction market exchange registered with the U.S. Commodity Futures Trading Commission (CFTC), Kalshi completed a $185 million Series C financing round in June 2025 (led by Paradigm), valuing the company at around $2 billion. The latest disclosure in October has increased the valuation to $5 billion, with an annualized trading volume growth rate exceeding 200%. The platform introduced contracts related to cryptocurrency assets in the third quarter, such as "Will Bitcoin close above $80,000 by the end of this month" and "Will an Ethereum ETF be approved before the end of the year," marking the formal entry of traditional institutions into the speculative and hedging market of the "crypto narrative event." According to Investopedia, the trading volume of its crypto-related contracts exceeded $500 million within two months of launch, providing institutional investors with a new channel to express macro expectations within a compliant framework. As a result, the prediction market has formed a dual-track structure of "on-chain freedom + rigorous compliance."

Unlike early prediction platforms that leaned toward entertainment and political themes, the mainstream market focus in the third quarter of 2025 has significantly shifted toward macro policies, financial regulations, and events linking currencies and stocks. The cumulative trading volume of macro and regulatory contracts on the Polymarket platform has exceeded $500 million, accounting for over 40% of the quarterly total trading volume. Investors remain highly engaged in themes such as "Will an ETH spot ETF be approved before Q4" and "Will the Circle stock price break through a key level post-listing." The price trends of such contracts sometimes even lead traditional media sentiment and derivatives market expectations in certain periods, gradually evolving into a "market consensus pricing mechanism."

The core innovation of on-chain prediction markets lies in their liquidity pricing of events through a tokenization mechanism. Each prediction event is binaryized or turned into a continuous form in tokenized format (e.g., YES/NO Token), and relies on automated market makers (AMMs) to maintain liquidity, enabling efficient price discovery without the need for order matching. Settlement depends on decentralized oracles (e.g., UMA, Chainlink) for on-chain execution, ensuring transparency and auditability. This structure allows nearly all social and financial events — from election results to interest rate decisions — to be quantified and traded as on-chain assets, forming a new paradigm of "information securitization."

However, alongside rapid development, risks are also a significant consideration. Firstly, oracle risk remains a key technical bottleneck for on-chain prediction markets, where any external data delay or manipulation could lead to contract settlement disputes. Secondly, unclear compliance boundaries still limit market expansion, as the regulatory approaches of the United States and the European Union towards event-based derivatives have not been fully harmonized. Thirdly, some platforms still lack KYC/AML processes, posing potential risks related to compliance with fund sourcing. Finally, liquidity is excessively concentrated on major platforms (with Polymarket holding over 90% of the market share), which could lead to price deviations and amplified market fluctuations in extreme market conditions.

Overall, the third quarter's performance in the prediction market shows that it is no longer a marginalized "crypto play," but is becoming an important layer of the macro narrative. It is both an immediate reflection of market sentiment and an intermediary tool for information aggregation and risk pricing. Looking ahead to the fourth quarter, the prediction market is expected to continue evolving along a "on-chain × compliant" dual-loop structure: the on-chain segment represented by Polymarket will expand through DeFi liquidity and macro narrative trading; while the compliance-oriented platform Kalshi will accelerate institutional capital attraction through regulatory approval and a USD pricing mechanism. With the prevalence of data-driven financial narratives, the prediction market is transitioning from an attention economy to decision-making infrastructure, becoming one of the few asset layers in the financial system that can both reflect collective sentiment and provide forward-looking pricing functionality.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia

0

0