Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Reviewing the Flash Crash of ZKJ and KOGE: A Deliberate Liquidity Harvesting "Scheme"

In the early hours of June 16th, Binance officially addressed the sharp volatility seen in $ZKJ and $KOGE. Preliminary investigations suggest that the price turbulence was primarily driven by the concentrated withdrawal of liquidity by large holders, triggering a cascade of liquidations. To prevent similar incidents from occurring again and to mitigate structural risks associated with Alpha incentives, Binance announced that starting June 17th, transactions between Alpha tokens will no longer count toward the calculation of Alpha Points.

The initial content of the article is as follows:

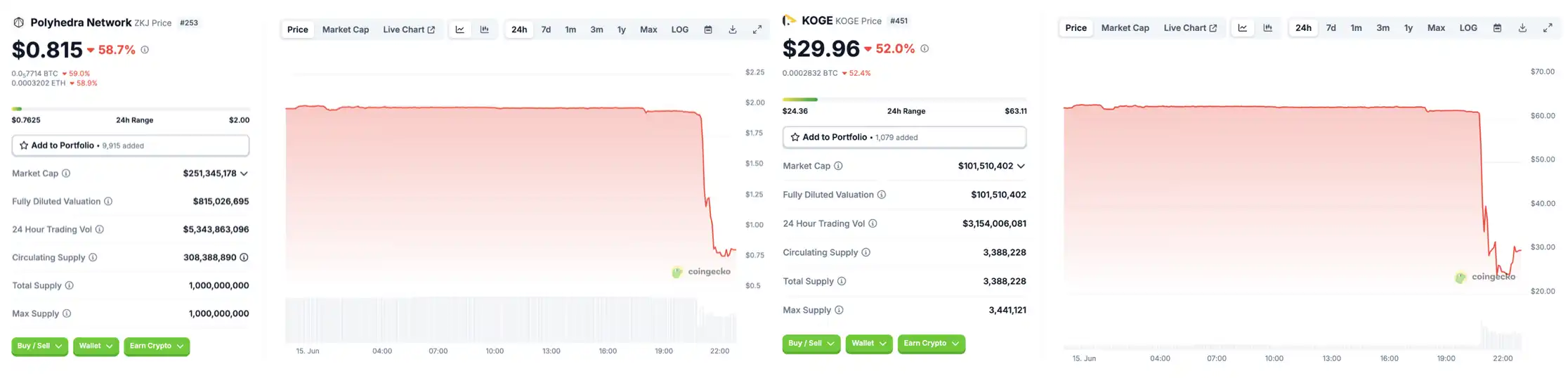

Previously recognized as the most cost-effective token pair for point farming within Binance Alpha—$ZKJ and $KOGE simultaneously experienced a flash crash.

Within the Binance Alpha platform, this token pair was once regarded as the most valuable tool for point farming, providing extremely high LP annualized returns and minimal slippage loss. It quickly became the go-to pool for Alpha users. The influx of significant capital and increased trading activity created an illusion of "stable growth," which ultimately laid the groundwork for subsequent systemic collapses.

To understand where it all began, we first need to revisit the incentive mechanism behind Binance Alpha itself.

It All Starts with Binance Alpha

Binance Alpha is an incentive mechanism launched by Binance in late 2024. Users can earn points through providing liquidity (LP), participating in trades, and holding tokens to engage in interactions. These points can then be used to participate in platform's regular airdrops and exclusive events.

Because of its transparent incentive ratios and clear distribution rhythm, Binance Alpha gradually became the focus of attention for "yield farmers" adapting to shifts in market dynamics. Farming volume and setting up LPs emerged as the most mainstream scoring strategies, indirectly spawning token pair combinations optimized specifically for Alpha structures.

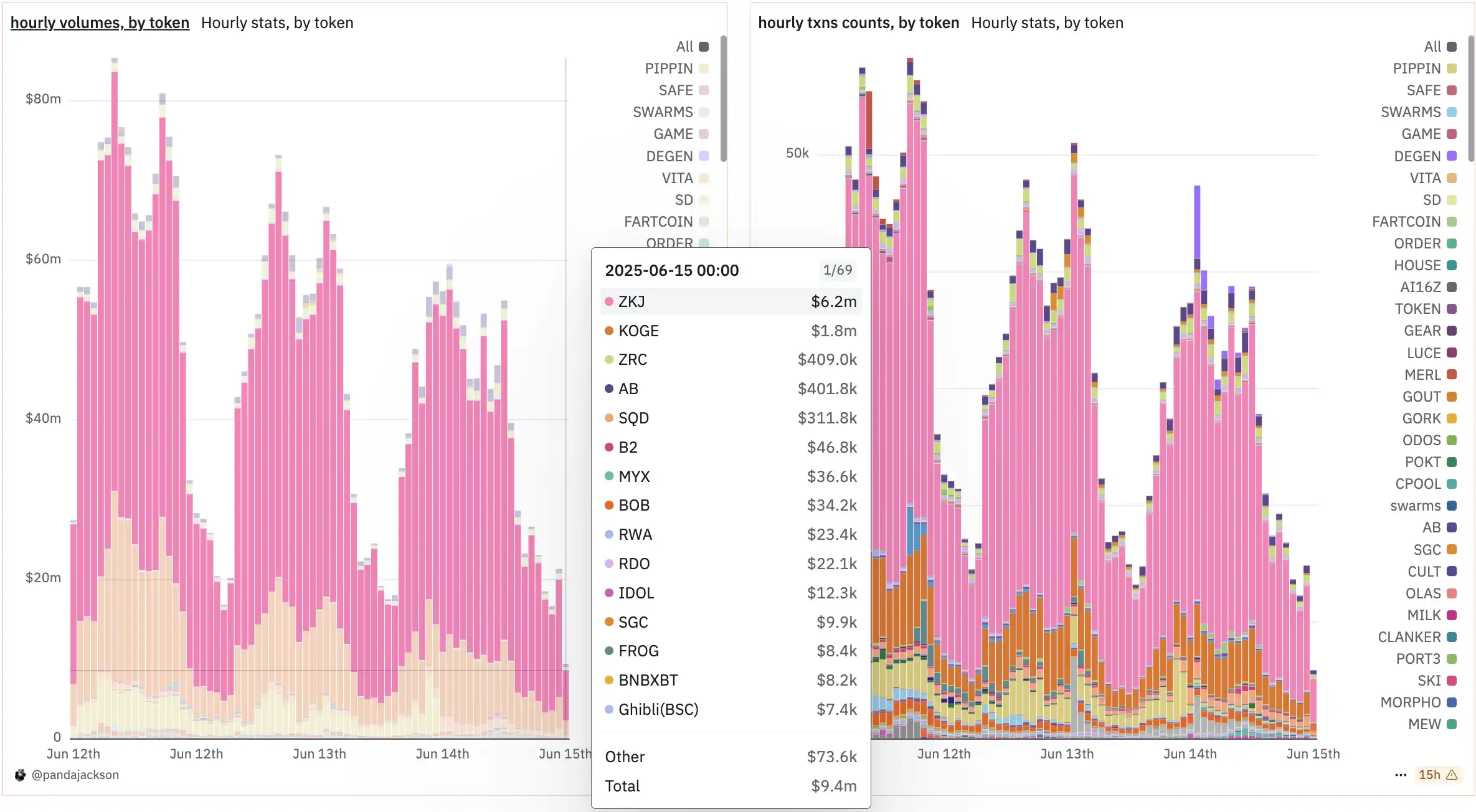

According to data from @pandajackson42, on June 14th alone, Binance Alpha recorded a total trading volume of $987 million, with $ZKJ and $KOGE trading volumes reaching $703 million and $159 million, respectively, securing the top two spots on the leaderboard.

However, after trading volume peaked at $2.04 billion on June 8th, the Alpha activity level has steadily declined. By June 14th, the trading volume had dropped by over 50% compared to its peak. On the same day, Binance announced upcoming adjustments to its airdrop distribution mechanism, which would be divided into "goal-based claims" and "first-come, first-served" stages. This change was interpreted by some members of the community as an indirect catalyst for large holders’ early exits and LP withdrawals.

In the Alpha points acquisition mechanism, the weighting for trading volume and liquidity provision is excessively high, leading to the widespread popularity of the "market making–wash trading–circular trading" trio, with the $ZKJ and $KOGE dual-token pool becoming a typical example.

The Overt Strategy of Whales?

Previously, the project team constructed a KOGE/ZKJ dual-token trading pair, opening permissions to external liquidity studios and heavily directing funds to participate in wash trading. Simultaneously, $KOGE's liquidity in the BNB and USDT pools remained relatively shallow, meaning that even large-scale capital wanting to exit would find it difficult to convert KOGE into mainstream assets directly.

Image Source: @Emilia88_eth

During periods of high APY, whales of KOGE and ZKJ continuously added LPs, boosting pool liquidity and encouraging more users to join. Their core logic was: KOGE itself lacked sufficient trading scenarios and external demand, which made direct liquidation difficult. On the other hand, ZKJ had massive open interest in the futures market, giving it stronger monetization capabilities. By utilizing the Router's automatic path selection mechanism, constructing a KOGE/ZKJ trading pair not only enhanced liquidity but also laid the groundwork for future liquidations.

According to community user Emilia's observations, the KOGE project team consistently added one-sided liquidity, controlling the token's price increase. This also resulted in KOGE/USDT's actual liquidity being much smaller than it appeared. If whales dumped KOGE on the market, the remaining LPs couldn't exit through the KOGE/USDT pool and would have to convert to ZKJ, further triggering a chain reaction of liquidations.

Meanwhile, some whales established short positions on ZKJ in centralized exchanges (CEX) to hedge for later stages. As market activity slowed, APY decreased, and wash trading funds diminished, whales began withdrawing LPs one after another, converting their KOGE holdings into ZKJ, and then dumping ZKJ en masse to complete their exit. Spot prices rapidly declined as a result, and ZKJ long positions in the futures market saw widespread liquidation, amplifying the downward movement.

Price volatility prompted greater liquidity withdrawal, forming a typical negative feedback loop. Due to the insufficient depth of the KOGE/USDT pool, subsequent users' exit paths largely had to rely on ZKJ, further depressing ZKJ's price. During this process, the KOGE project team continuously added unilateral liquidity to KOGE, creating the illusion of price support but effectively compressing the actual realizable liquidity, intensifying the capital strain. When market sell pressure concentrates, the remaining LPs cannot exit smoothly through the original path, forcing funds to flow into ZKJ, triggering a cascading liquidation scenario.

Ultimately, this structurally fragile design, compounded by LP arbitrage, highly leveraged contract positions, and high-yield inducements lacking real value inflows, evolved into a typical liquidity crisis in a short period, causing both KOGE and ZKJ to collapse.

"Large-Scale Liquidity Withdrawal + Sustained Selling" Process

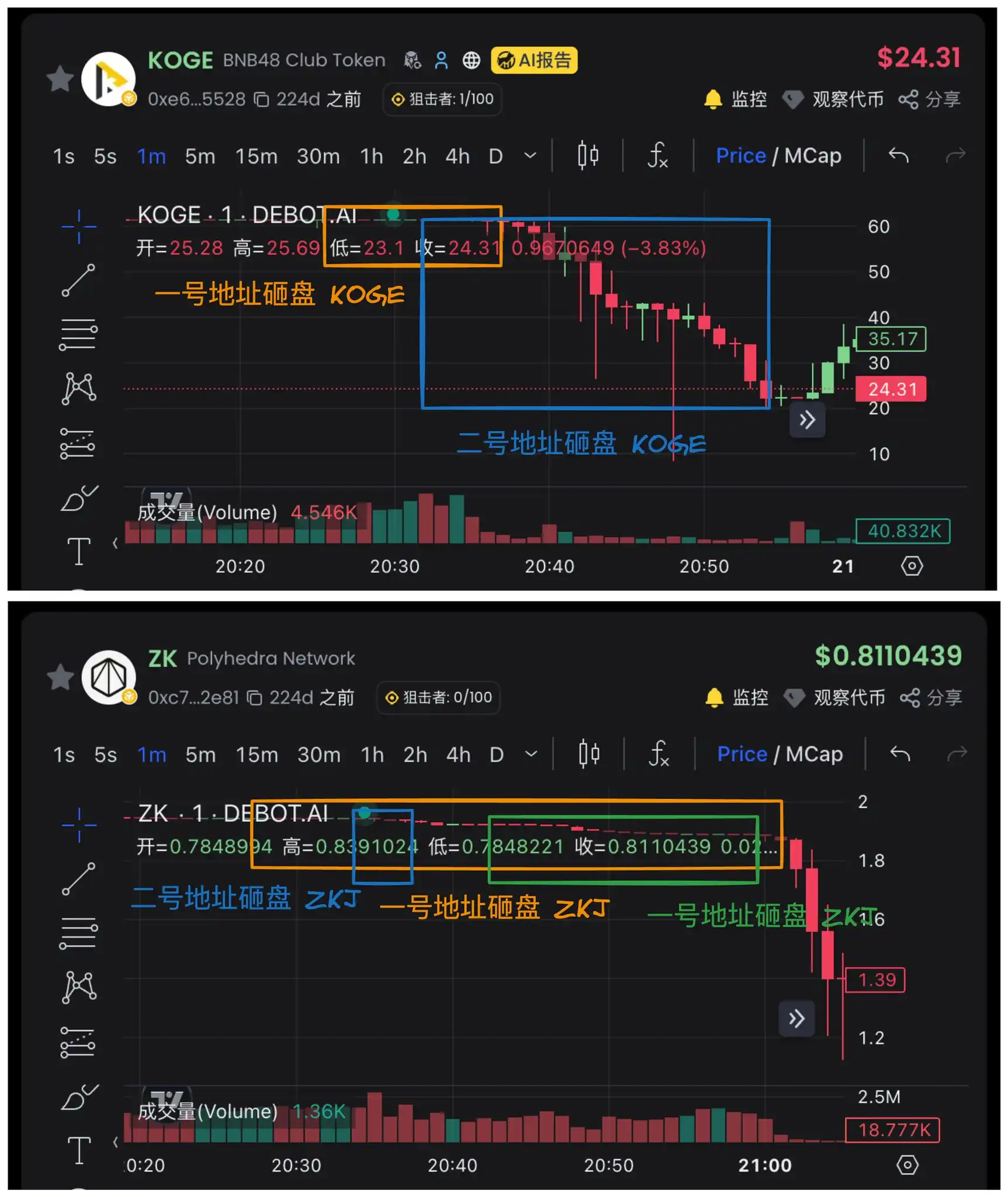

According to on-chain analyst @ai_9684xtpa, the simultaneous flash crash of $ZKJ and $KOGE was caused by three major addresses exerting dual pressure through "large-scale liquidity withdrawal + sustained selling." Below is an analysis of the on-chain traces:

20:28:21 and 20:33:15: Conducted two separate withdrawals of 61,130 KOGE (approximately $3.76 million) and 273,017 ZKJ (approximately $532,000) in dual-sided liquidity.

20:28:58 - 20:36:57: Swapped 45,470 KOGE for ZKJ during this timeframe, valued at $3.796 million. During this period, KOGE's on-chain trading volume visibly increased.

20:30:57 - 20:59:49: Sold 1.573 million ZKJ in batches, converting them into USDT and BNB, worth $3.052 million at an average selling price of $1.94 each. At this point, both KOGE and ZKJ experienced minor stair-step declines but did not yet plummet.

20:30:33: Withdrew 33,651 KOGE (approximately $2.07 million) and 709,203 ZKJ (approximately $1.38 million) in dual-sided liquidity.

20:31:10 - 20:58:18: Swapped 36,814 KOGE for ZKJ during this period, valued at $2.26 million.

20:35:15 - 20:37:34 Sold 1 million ZKJ tokens, valued at $1.948 million, with an average selling price of $1.948.

The "relay-style sell-off" by this address finally triggered a rapid decline in KOGE token price, which is represented by the consecutive large red candlesticks on the chart that everyone noticed.

Address 0x6aD...e2EBb

20:41:55 Received 772,759 ZKJ tokens worth $1.5 million from address 0x078...8bdE7 (the previous selling address).

20:42:28 - 20:50:16 Liquidated 772,759 ZKJ tokens during this period.

The third address primarily acted cooperatively, further catalyzing the decline in ZKJ after the KOGE token price crash, completing the harvest of liquidity pools (LP) and token holders of both tokens.

Has Binance Alpha's Bonus Faded?

This type of liquidity structure driven by short-term incentives can easily evolve into "targeted harvesting" under extreme market conditions. While the project's fundamentals remain unchanged, external factors such as the end of incentives, structural liquidations, or market maker exits intervene, leading to a precipitous price drop, with ordinary users lacking hedging mechanisms ultimately bearing the loss.

Particularly, KOGE lacks hedging tools, leaving most participants exposed with direct LP liquidity or market-making positions, resulting in even more substantial losses. By comparison, some experienced users primarily focused their operations on ZKJ and allocated derivative short positions, mitigating part of the risk.

In the aftermath, the community began reflecting on Binance Alpha's incentive mechanism. Many suggestions aim to reduce the overreliance on trade volume and LP weight alone, proposing to link incentives to interaction quality, holding duration, and implement penalization for behaviors like abnormal short-term self-trading or concentrated withdrawals.

For Binance, Alpha remains a crucial tool for enhancing on-chain activity and attracting quality projects. However, its sustainability will depend on more comprehensive risk control measures and incentive designs.

In hindsight, the $ZKJ crash was not a black swan event but rather an inevitable outcome of the "low transaction fees" illusion. Liquidity does not equate to legitimacy, narratives can amplify risks, and coordinated exits are never accidental. In the crypto market, structures that offer high returns but lack value loops are scripts pre-written for stampedes, and the ZKJ and KOGE episode reaffirms this fundamental principle.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia